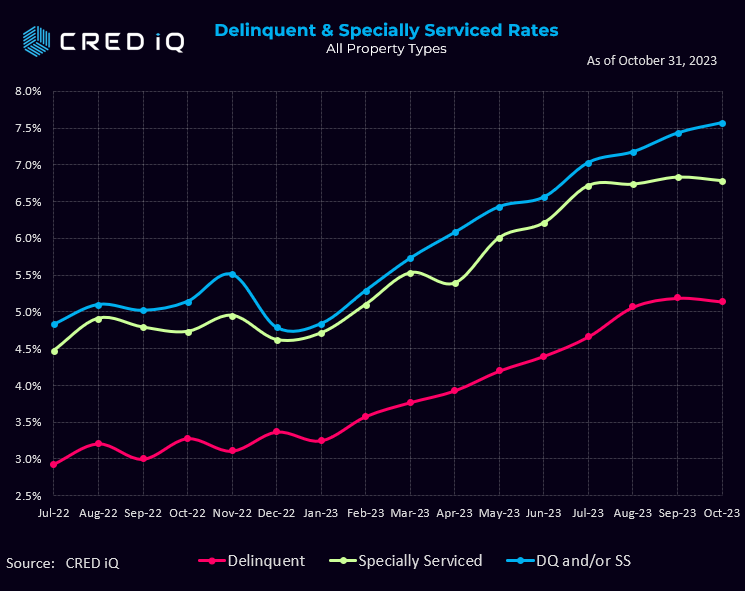

The CRED iQ overall distress rate for CMBS increased by 14 basis points to 7.57%, the 10th consecutive monthly increase this year. The core delinquency rate decreased by 5 basis points – snapping 9 months of increases in 2023. Similarly, our special servicing rate, which represents the percentage of CMBS loans that are with the special servicer (includes both delinquent and non-delinquent), trimmed 5 basis points from the September print.

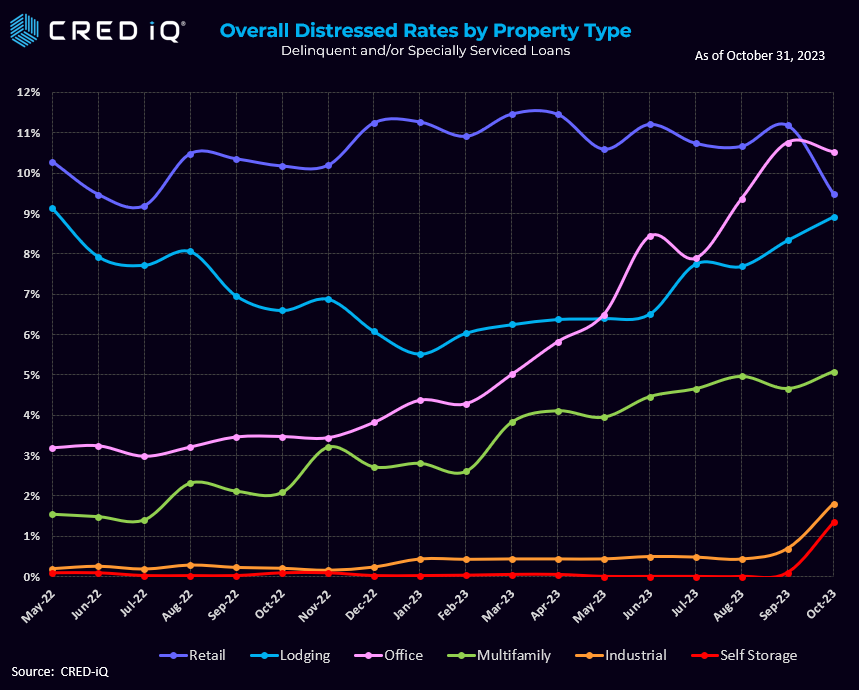

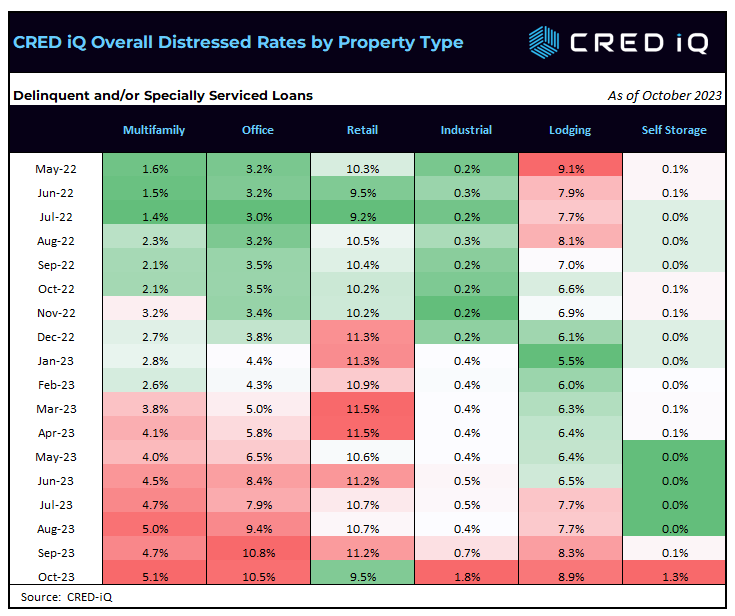

Looking across the CRED iQ Distressed Rate Heat Map, all property types are in the red — with the exception of retail which achieved the most significant reduction in overall distress rate in October. Meanwhile, self-storage landed in the red for the first time in two years.

The retail segment saw a significant reduction in its overall distress rate, logging 9.47% in October, a reduction of 1.71% from September’s rate of 11.18%.

Industrial’s overall distressed rate was 1.81% in October compared to 0.70% in September – an uncharacteristic spike. In fact, October marks the first month that the Industrial segment posted a rate above 1.0% this year. It should be noted that a significant portion of the spike is attributable to a single property. The $1.43 billion floating-rate industrial loan, which was securitized in a Single-Borrower, Large Loan deal in 2021 was originally collateralized by 109 properties totaling over 14M square feet. The loan has since been paid down to $952 million as of October 2023 due to the release of 32 properties. The loan failed to pay off at its maturity date in October 2023. CRED iQ’s data indicates that the loan’s interest rate cap agreement expired on October 9, 2023. Due to the floating-rate, interest-only structure of this industrial loan, annual debt service payments have almost tripled since January 2022. January 2022’s monthly debt service totaled $2.1 million ($25 million annualized) compared to this month’s debt service of $5.6 million ($67 million annualized).

Lodging continued to see its overall distress rates rise – adding 58 basis points to 8.92%. Similarly, Multifamilylogged a 42-basis point increase to 5.08%. Officeremains the segment leader in overall distress at 10.51% – although trimming 24 basis points of Overall Distress vs. September.

Finally, the most resilient self-storage segment posted its biggest jump of the year to 1.35% — compared to 0.10% in September Like industrial, this marks the first posting above 1.0% in 2023.

CRED iQ’soverall distress rate aggregates the two indicators of distress – delinquency rate and special servicing rate – into an overall distressed rate. This includes any loan with a payment status of 30+ days or worse, any loan actively with the special servicer, and includes non-performing and performing loans that have failed to pay off at maturity.

A severely limited refinancing and a ‘higher for longer’ interest rate environment continues to contribute to sustained increases in commercial real estate distress. With the Federal Reserve holding rates unchanged at the November meeting, perhaps the market is approaching the peak of interest rate increases, but that remains to be seen.