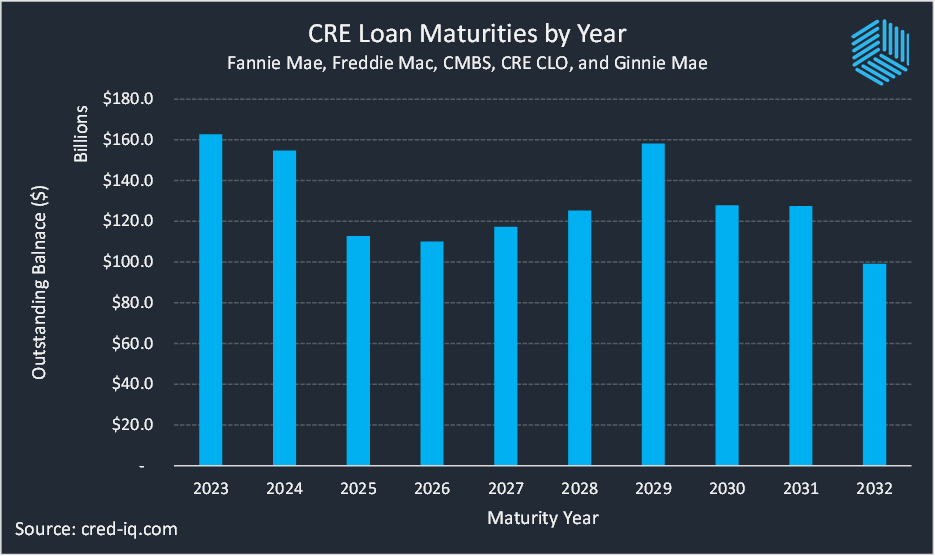

CRED iQ prepared for the year ahead in commercial real estate by examining securitized commercial mortgages with maturity dates scheduled in 2023. CRED iQ’s database has approximately $162 billion in commercial mortgages that are scheduled to mature in 2023, including loans securitized in CMBS conduit trusts, single-borrower large-loan securitizations (SBLL) and CRE CLOs, as well as multifamily mortgages securitized through government-sponsored entities. The next 12 months have the highest volume of scheduled maturities for securitized CRE loans over a period of 10 years ending 2032.

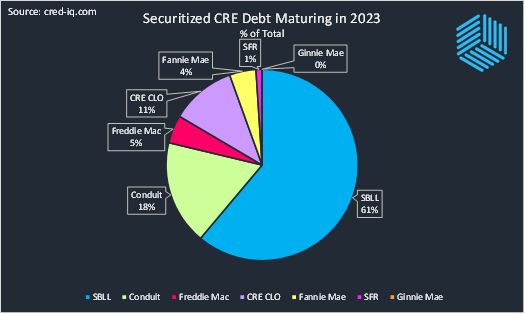

By securitization type, the SBLL securitization subset of nearly $100 billion comprises the majority (61%) of scheduled maturities in 2023; however, approximately 94% of that balance is tied to floating-rate loans that have extension options available, providing no assurances of refinancing or new origination opportunities.

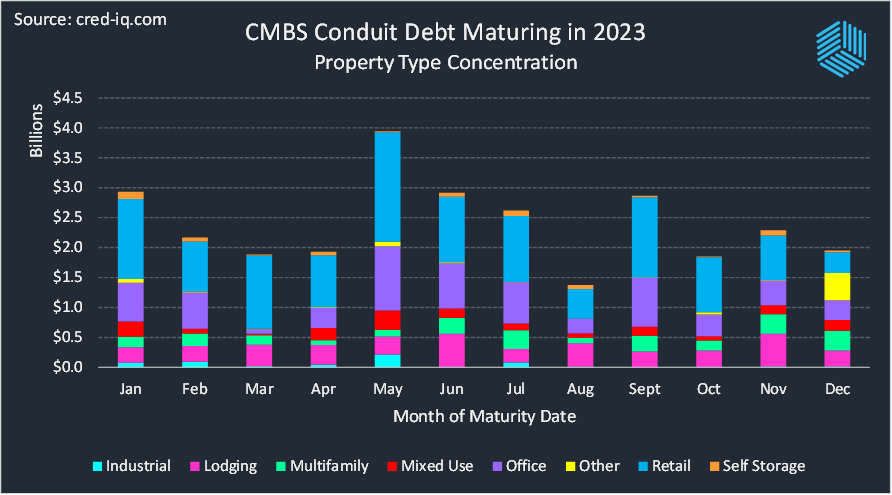

CMBS conduit loans account for the second-highest total of loans with 2023 maturity dates with approximately $29 billion in 2023 scheduled maturities, accounting for 18% of total scheduled maturities. This group of loans provides for diverse observation across property type, building class, and geographic location. Breaking down 2023 conduit maturities by property type, retail has the highest concentration with 42% of outstanding debt and is followed by office with 22%. Lodging has the third-highest concentration with 14% of the outstanding balance of scheduled maturities in 2023.

From a monthly perspective, CMBS conduit loan maturities are dispersed fairly evenly throughout the year. May 2023 has the highest total of scheduled maturities out of any month with $3.9 billion. September 2023 has the second-highest total with $2.9 billion in scheduled maturities and is followed by January 2023, also with $2.9 billion. The January 2023 subtotal of maturities has potential to drop significantly over the next few weeks as refinances close ahead of yearend. Loans generally have three to four-month open periods so lenders often have the opportunity to provide refinancing earlier than stated maturity dates.

Approximately 12% of the 2023 scheduled maturity debt for CMBS conduits is already delinquent or in special servicing, foreshadowing potential maturity defaults, delayed payoffs, or extended workouts.

Multifamily

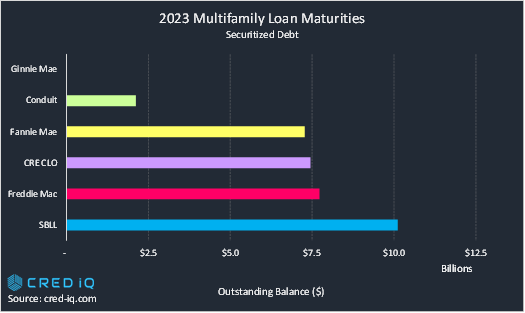

The multifamily sector is the only property type represented across all various securitization structures in the 2023 maturity analysis, which includes Fannie Mae and Ginnie Mae mortgage debt. Aside from single-borrower large-loan multifamily loans with relatively higher probabilities of being extended, Freddie Mac securitizations accounted for the second-highest outstanding balance of scheduled maturities in 2023 with approximately $7.7 billion. Following close behind, there is about $7.5 billion in multifamily loans securitized in CRE CLOs that are scheduled to mature in 2023. Many multifamily loans securitized in CRE CLO vehicles are secured by transitional apartment properties moving up in building class through value-add initiatives. Although many of these loans have floating rates, the idea of locking in fixed-rate financing after completion of value adds may be an optimal completion of properties’ business plans. Fannie Mae multifamily loans also account for a considerable portion of 2023 maturities with $7.3 billion in outstanding debt coming due over the next year.

Retail

Among CMBS conduit debt, retail is the property type with the highest volume of schedule maturities in 2023. There is over $12 billion in retail loans coming due in 2023, accounting for 42% of total scheduled 2023 maturities. Loans secured by retail properties have had the highest delinquency rates among all properties times for most of 2022. CRED iQ’s delinquency rate for retail was 7.06% as of October 2022 and has potential to rise throughout 2023 as maturity defaults occur in the process of sorting out payoff resolutions.

Office

Perhaps one of the highest concerns from lenders is refinancing office loans. In the CMBS conduit environment, there is approximately $6.3 billion in loans secured by office properties scheduled to mature in 2023. This accounts for 22% of the total 2023 CMBS conduit maturities. CRED iQ’s special servicer rate for office loans has increased for three consecutive months from July 2022 through October 2022. Recessionary pressures, downsizing from tech firms and others, and the evolution of workplace dynamics from the fallout of the pandemic have all been encompassing forces have had an adverse impact on office loan originations.

Looking Back and Looking Forward

Aside from a focus on 2023 maturities, the year ahead brings plenty of opportunities within the CRE industry. Looking back — there is over $35 billion in outstanding debt with a past due scheduled maturity date that still needs to be worked out as well as several billion dollars in REO assets that are on track to be liquidated. Looking ahead to 2024 — CRED iQ’s early estimates indicated nearly $155 billion in scheduled maturities; however, the aggregate total is fluid when considering loan extensions and potential prepayments throughout 2023.

About CRED iQ

CRED iQ is a commercial real estate data, analytics, and valuation platform designed to unlock investment, financing, and leasing opportunities. CRED iQ provides real-time property, loan, tenant, ownership, and valuation data for over $2.0 trillion of commercial real estate.