A CRED iQ Preliminary Analysis

DATA HEREIN PROVIDED TO CRED IQ IS FROM A PRELIMINARY PROSPECTUS AND MAY BE AMENDED OR SUPPLEMENTED PRIOR TO TIME OF SALE

Deal Overview

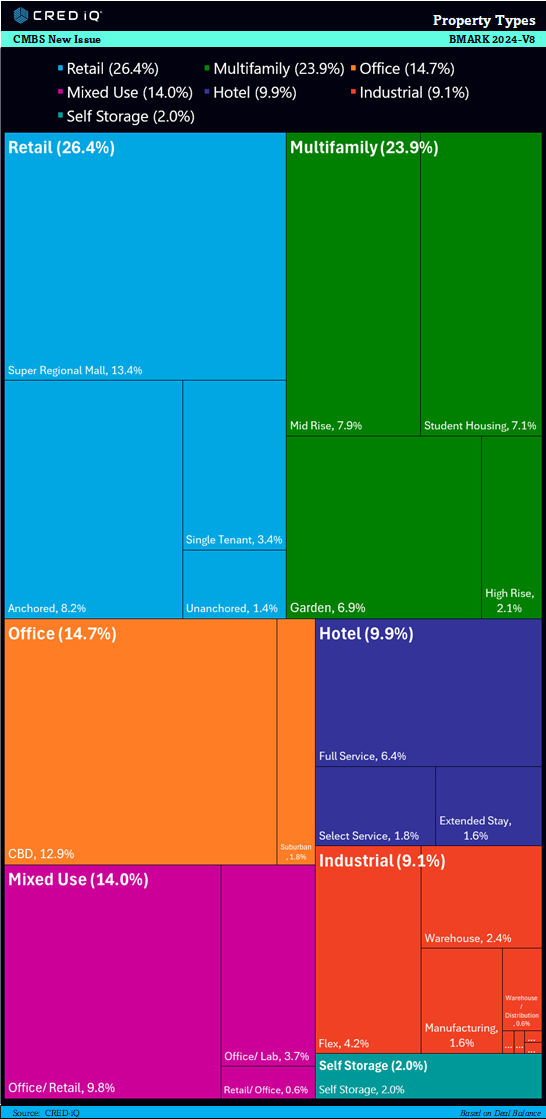

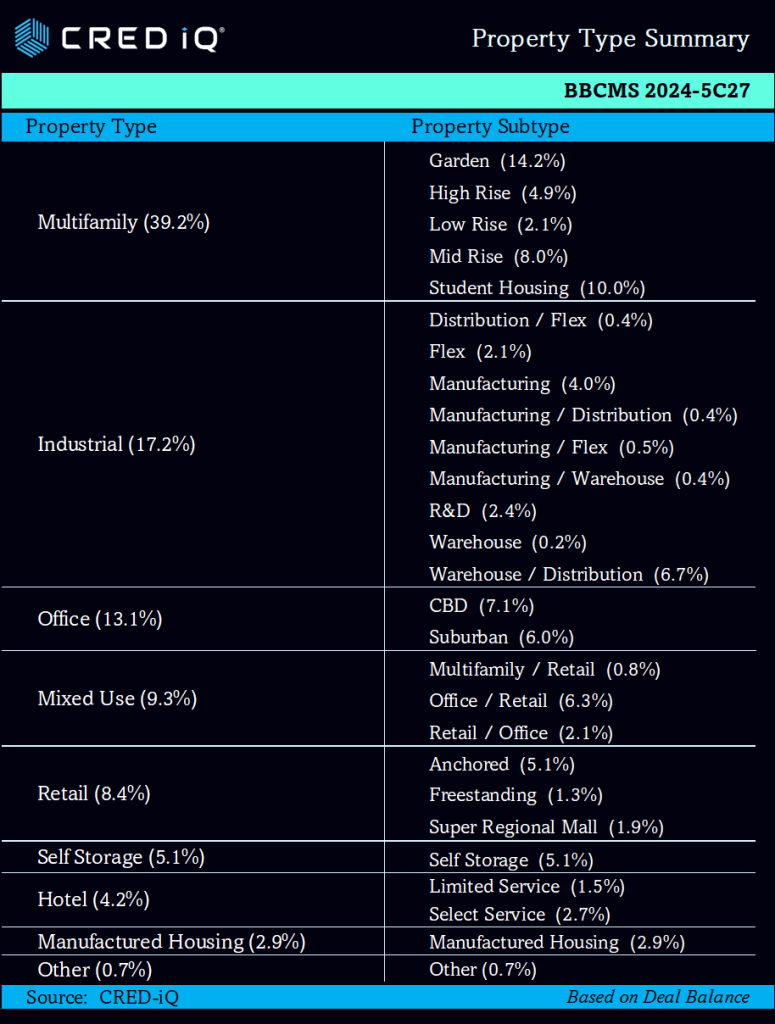

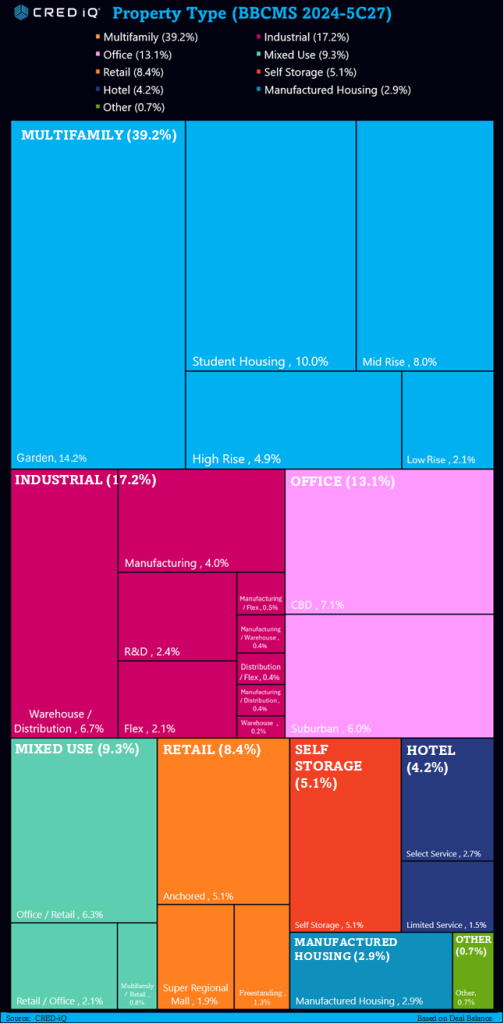

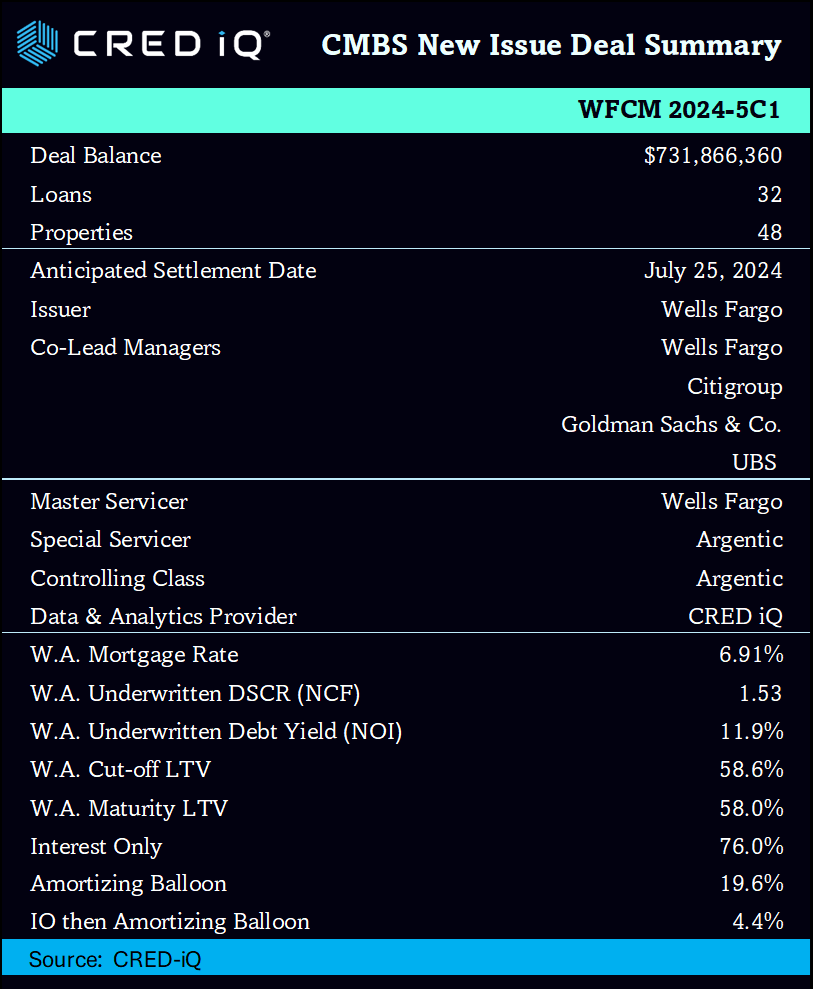

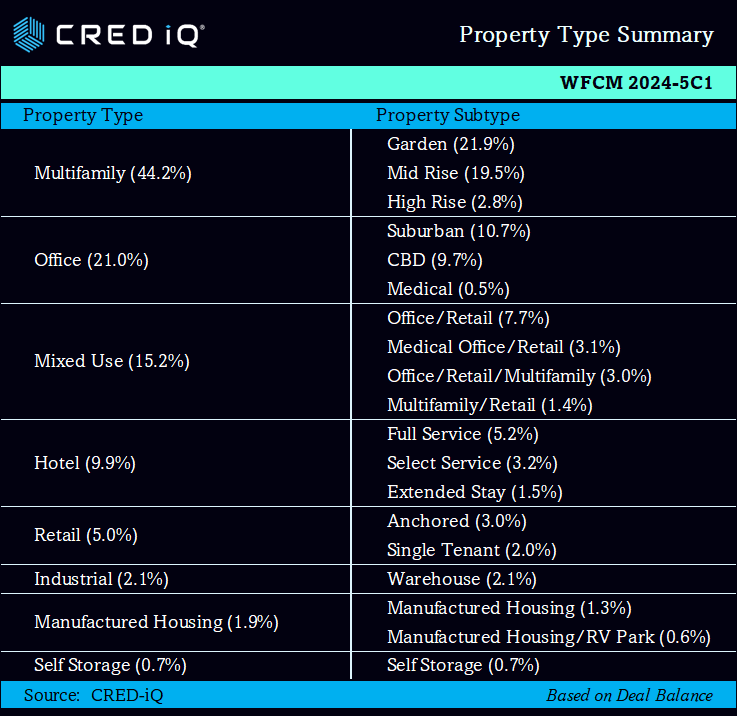

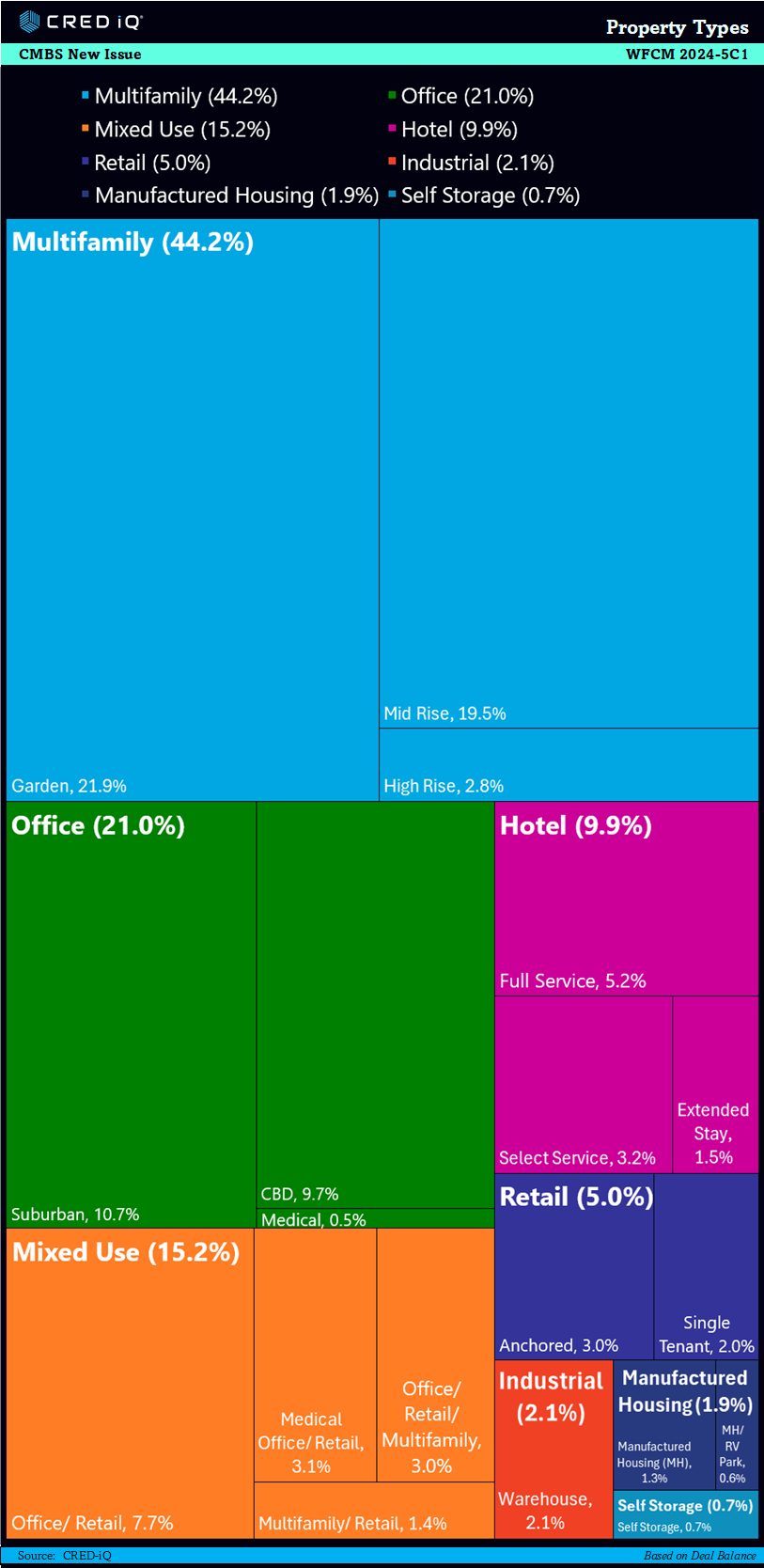

The Wells Fargo Commercial Mortgage Trust 2024-5C1 is a significant new issue CMBS deal with an approximate aggregate certificate balance of $646.8 million, backed by a mortgage pool totaling around $731.9 million. This transaction is managed by Wells Fargo Securities, Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, and UBS Securities LLC, with additional support from co-managers Academy Securities, Drexel Hamilton, and Siebert Williams Shank. The offering consists of 32 loans secured by 48 properties, presenting a diversified portfolio that spans various property types such as multifamily, office, mixed-use, and hospitality. The properties are geographically dispersed, ensuring a robust risk mitigation strategy for investors.

Key Metrics

Key metrics for this CMBS deal include a weighted average loan-to-value (LTV) ratio of 58.6% and a weighted average mortgage interest rate of 6.91%. The loan pool is structured to include a mix of amortizing and interest-only loans, with 24% of the mortgage pool having scheduled amortization and the remaining 76% providing for interest-only payments throughout the loan term. This mix is designed to offer flexibility and stability in cash flow, appealing to a broad range of investors seeking both short-term and long-term returns. Additionally, the pool features a weighted average debt service coverage ratio (DSCR) of 1.53x and a weighted average net operating income (NOI) debt yield of 11.9%, indicating strong underwriting standards and financial performance.

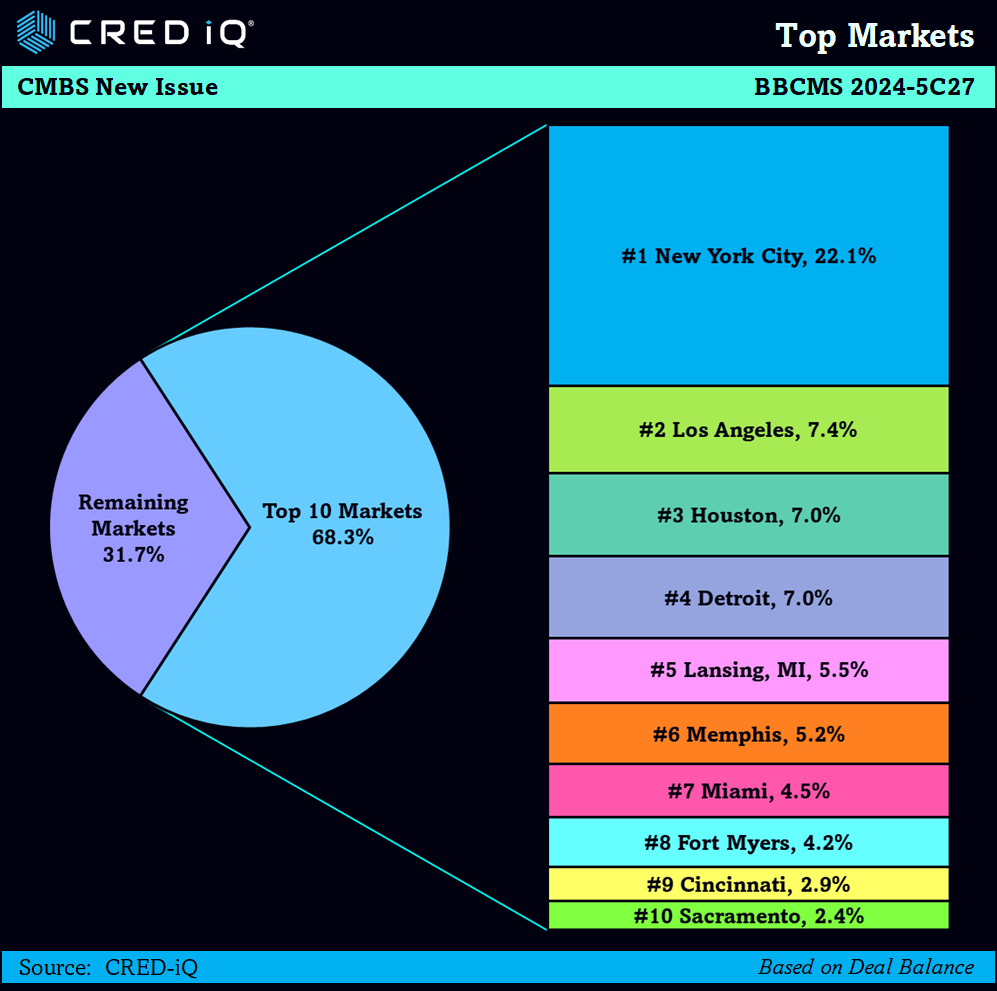

Geography & Top Assets

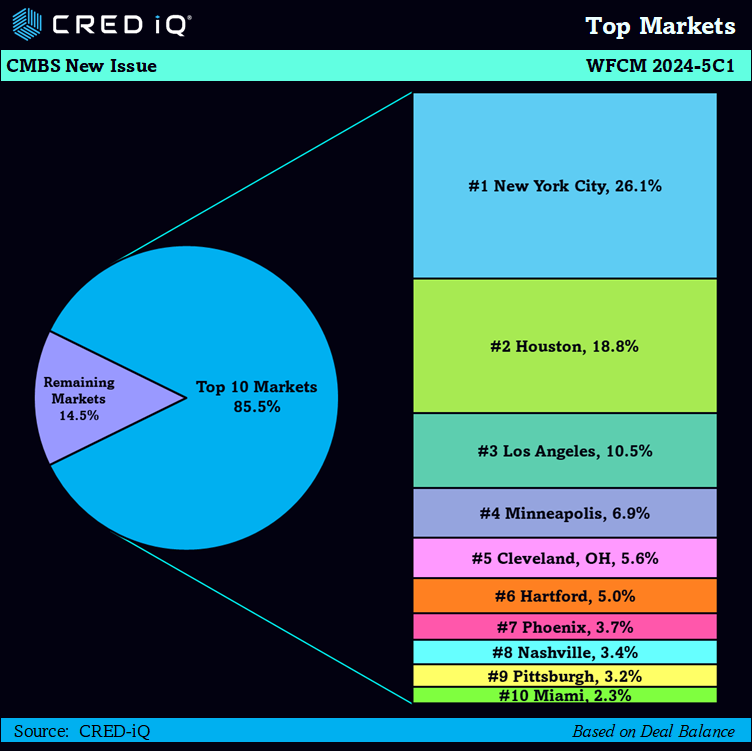

The transaction highlights include properties concentrated in major markets like New York City, Houston, and Los Angeles with significant assets such as the 9950 Woodloch suburban office property in Houston and the 640 5th Avenue mixed-use (office/retail) property in New York. The deal is set to close on July 25, 2024, with the master servicer being Wells Fargo Bank and the special servicer being Argentic Services Company LP. The certificates are expected to be rated by Fitch Ratings, Kroll Bond Rating Agency, and Moody’s Investors Service, providing additional assurance of the deal’s quality and reliability. This CMBS offering presents a well-structured investment opportunity with diverse property types and geographic distribution, designed to deliver stable returns and mitigate risks effectively.

For subscribers to CRED iQ

About CRED iQ

CRED iQ is a market data provider that offers a robust suite of data and software solutions tailored for commercial real estate and finance professionals. With over $2.3 trillion of CRE loans, CRED iQ delivers instant access to a comprehensive range of financial data and analytics for millions of properties in every market. CRED iQ’s data and analytical capabilities are instrumental in helping investors, lenders and brokers make informed and strategic decisions critical to their business.

If you would like to learn more about CRED iQ’s products and services, please contact team@cred-iq.com or (215) 220-6776.

THE DATA, INFORMATION AND/OR RELATED MATERAL (“DELIVERABLES”) IS BEING SOLD IN AS-IS/WHERE-AS CONDITION. CRED-IQ MAKES NO REPRESENTATION OR WARRANTY AS TO QUALITY OR ACCURACY OF SUCH DELIVERABLES BEING PURCHASED, WHETHER EXPRESS OR IMPLIED, EITHER IN FACT OR BY OPERATION OF LAW, STATUTE, OR OTHERWISE, AND CRED-IQ SPECIFICALLY DISCLAIMS ANY AND ALL IMPLIED OR STATUTORY WARRANTIES INCLUDING WARRANTIES OF MERCHANTABILITY AND OF FITNESS FOR A PARTICULAR PURPOSE, TECHNICAL PERFORMANCE, AND NON-INFRINGEMENT. WITHOUT LIMITING THE FOREGOING, YOU AS CUSTOMER ACKNOWLEDGE THAT YOU HAVE NOT AND ARE NOT RELYING UPON ANY IMPLIED WARRANTY OF MERCHANTABILITY OR OF FITNESS FOR A PARTICULAR PURPOSE OR OTHERWISE, OR UPON ANY REPRESENTATION OR WARRANTY WHATSOEVER AS TO THE DELIVERABLES IN ANY REGARD WHATSOEVER, AND ACKNOWLEDGE THAT CRED-IQ MAKES NO, AND HEREBY DISCLAIMS ANY, REPRESENTATION, WARRANTY OR GUARANTEE THAT THE PURCHASE, USE OR COMMERCIALIZATION OF ANY DELIVERABLES WILL BE USEFUL TO YOU OR FREE FROM INTERFERENCE. BY ACCEPTANCE OF THE DELIVERABLES, YOU HEREBY RELEASE CRED-IQ AND ITS AFFILIATES AND AGENTS FROM ALL CLAIMS, DAMAGES AND LIABILITY ARISING HEREUNDER.