The apartment loans with CMBS financing reached an 185% increase in distress since the start of the year. The CRED iQ distress rate added 13 basis points in June to 8.62%, a nearly identical gain as posted last month. The print marks a fourth straight record high. The CRED iQ team evaluated payment statuses reported for each loan, along with special servicing status as part of our monthly distress update. CRED iQ’s special servicing rate remained mostly flat at 8.08% while the CRED iQ delinquency rate gained 48 basis points to 6.28% in this print.

Segment Review

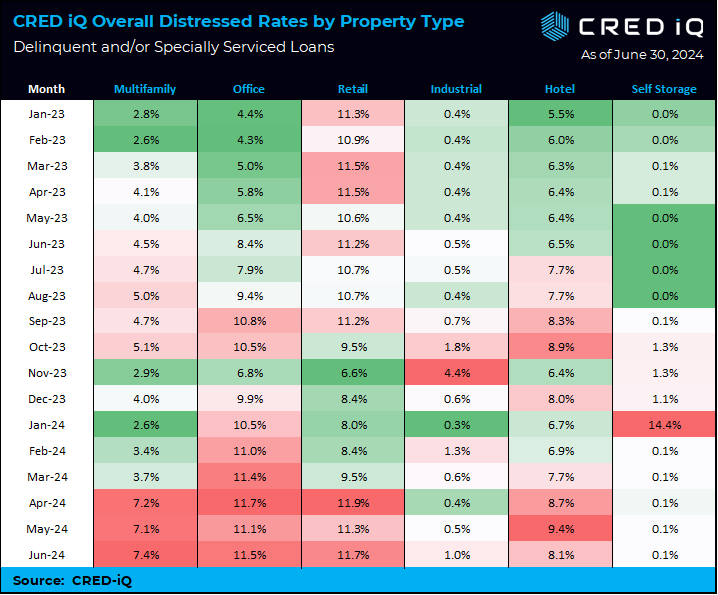

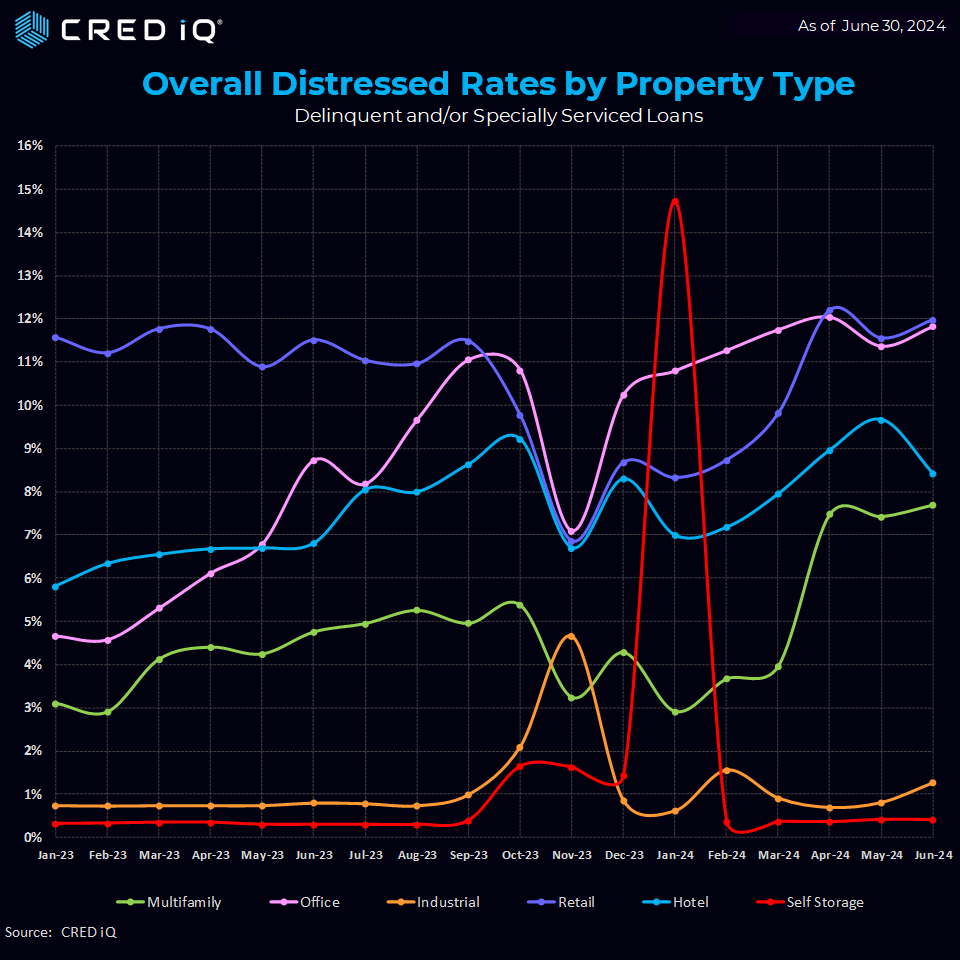

The retail and office sectors continue to battle for the highest distress rates, notching 11.7% and 11.5%, respectively. Both sectors saw modest increases of 4 basis points compared to the previous month.

The hotel sector held on to third place with an 8.1% distress rate, after logging the best month-over-month improvement of the group – shaving 130 basis points from our June print.

Multifamily monthly distress rate increased – adding a modest three basis point increase to 7.4% and earning multifamily a fourth-place finish. Six months ago, this number was 2.6%. Multifamily now challenges hotels for third place.

Industrial and self-storage continued operating at sub 1% for all but one of the last 7 months.

Payment Status

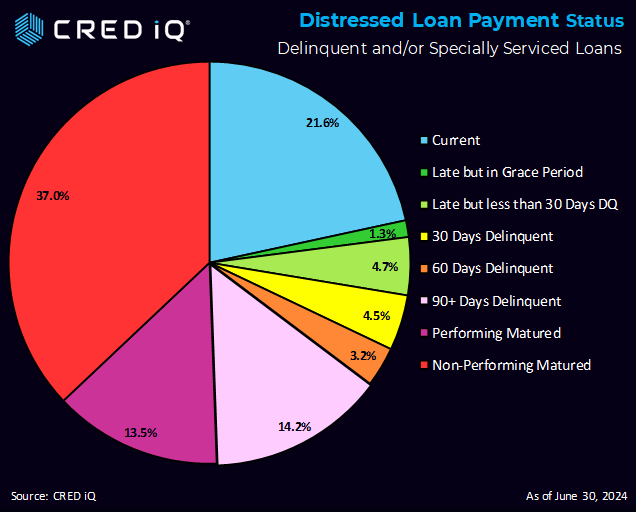

Looking at distressed loan payment status, 21.6% of the loans are current – a reduction of 2.8% when compared to the June report. Factoring in 1.3% and 4.7% attributable to Late (but in the grace period) and Late (but less than 30 days) respectively, the combined metric saw a 4.3% decrease in current and near-current status.

Once again, the largest category was Non-Performing Matured at 37%–notching a two percent month-over-month increase, followed by 90+ Days Delinquent at 14.2% (shaving 1.4%) and Performing Matured at 13.5% (adding 1.7% this month).

Analysis Methodology

CRED iQ’s distress rate aggregates the two indicators of distress – delinquency rate and specially serviced rate – yielding the distress rate. The index includes any loan with a payment status of 30+ days delinquent or worse, any loan actively with the special servicer, and includes non-performing and performing loans that have failed to pay off at maturity.

It’s important to note that CRED iQ’s distress rate factors in all CMBS properties that are securitized in conduits and single-borrower large loan deal types. CRED iQ tracks Freddie Mac, Fannie Mae, Ginnie Mae, and CRE CLO loan metrics in separate analyses.

As mentioned in our June report, our analysis exposes a meaningful gap between the distress and watchlist rates which could imply that the special serving & delinquency percentages may be likely to grow.

Loan Highlight

The 688,292 SF Equitable Plaza office property in the Mid-Wilshire submarket of Los Angeles is backed by an $87.1 million loan. The loan began amortizing in June 2019 after the initial five-year interest only period. Failing to pay off at its June 2024 maturity date resulted in the loan’s payment status degrading to non-performing matured. No maturity extension options were available at underwriting. Due to imminent default, the loan transferred to the special servicer in April 2024.

The CBD office property was constructed in 1969 and renovated in 1993. The asset most recently performed with a DSCR of 1.12 and 56.6% occupancy. At underwriting in March 2014, the asset was valued at $150.5 million ($219/SF).

About CRED iQ

CRED iQ is a market data provider that offers a robust suite of data and software solutions tailored for commercial real estate and finance professionals.

With over $2.3 trillion of CRE loans, CRED iQ delivers instant access to a comprehensive range of financial data and analytics for millions of properties in every market. CRED iQ’s data and analytical capabilities are instrumental in helping investors, lenders and brokers make informed and strategic decisions critical to their business.