")

CRED iQ Research | Q1 2026 | Multifamily Bank Loan Performance

The overall multifamily delinquency rate at FDIC-insured banks climbed to 1.47% in Q1 2026, up 5 basis points from 1.42% at year-end 2025, according to CRED iQ analysis of the latest Banking data. Delinquent multifamily balances reached $9.78 billion, the largest dollar amount since Q1 2011, even as bank multifamily portfolios continued to expand to a record $665.3 billion.

What Do Banks’ Q1 2026 Numbers Show for Multifamily?

CRED iQ tracks bank multifamily performance across three measures. Loans 30-89 days past due rose to 0.40% of balances, or $2.66 billion, up from 0.38% in Q4 2025. Loans 90+ days past due or in nonaccrual status, the seriously delinquent bucket, rose 3 basis points to 1.07%, with dollar volume increasing to $7.12 billion from $6.86 billion. Combined, the overall delinquency rate of 1.47% matches the Q1 2025 reading and marks the joint-highest level of this cycle. The Banking Report itself flagged multifamily past-due and nonaccrual rates as remaining elevated in its Q1 2026 release.

How Does 1.47% Compare Historically?

Outside of the matching Q1 2025 print, banks have not reported multifamily delinquency this high since Q2 2013, when the industry was still working down Global Financial Crisis credit. Today’s rate remains far below the GFC peak of 5.90% set in Q1 2010, when $12.68 billion was delinquent against a much smaller loan base. The more telling comparison is the cycle low: multifamily delinquency bottomed at just 0.21% in Q3 2019, meaning the current rate is seven times its pre-pandemic trough.

Are Banks Still Growing Their Multifamily Books?

Yes. Multifamily loans outstanding at FDIC-insured institutions rose 0.9% quarter over quarter and 4.1% year over year to $665.3 billion, roughly 3.5 times the $192 billion held in early 2007. Growing denominators have masked some of the dollar deterioration: delinquent balances are up $415 million in a single quarter and now sit at 15-year highs even while the rate itself appears moderate.

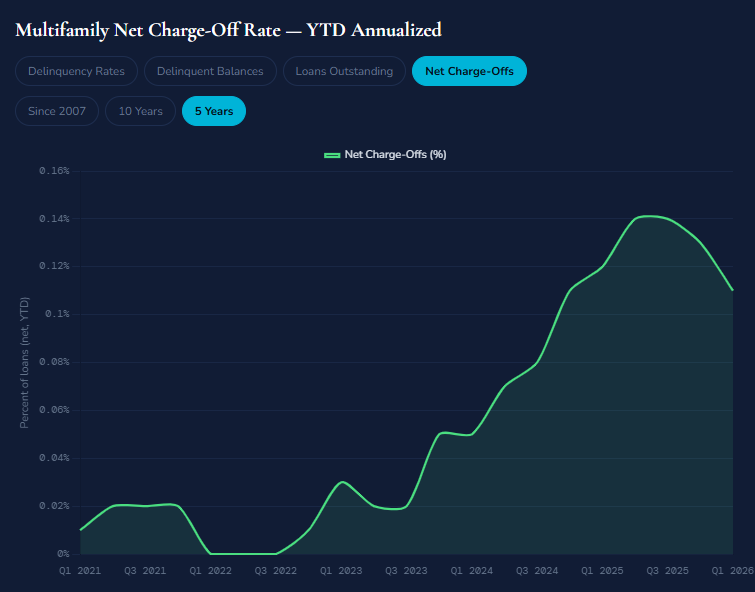

What Are Losses Telling Us?

Realized pain remains limited. The multifamily net charge-off rate ran at just 0.11% annualized in Q1 2026, down from 0.13% for full-year 2025. The gap between rising delinquency and muted charge-offs suggests banks are still resolving troubled multifamily credit through extensions and workouts rather than write-downs, a dynamic CRED iQ also observes across CMBS loan modifications.

The Bottom Line

Bank multifamily credit is deteriorating gradually, not collapsing. With $9.78 billion delinquent and balance growth still outpacing resolutions, Q2 2026 data will show whether the seasonal Q1 bump fades or compounds. Explore the full interactive tracker and request the underlying data at cred-iq.com.

Source: CRED iQ analysis of all FDIC-insured institutions, multifamily residential real estate loans, Q1 2007 through Q1 2026.

About CRED iQ

CRED iQ is the enterprise data and intelligence platform powering the securitized commercial real estate market — spanning CMBS, SASB, CRE CLO, and GSE/Agency Multifamily. Delivered via web platform, API, bulk feeds, and MCP server, CRED iQ is the data provider of choice for institutional market participants and the canonical data layer for AI-driven CRE workflows. Learn more at www.cred-iq.com.