April 03, 2025 – At CRED iQ, we’re committed to delivering timely, data-driven insights into the commercial real estate (CRE) market. Our latest analysis reveals a notable shift: the overall distress rate across commercial mortgage-backed securities (CMBS) has dropped for the second consecutive month, declining by 20 basis points to 10.6%. This encouraging trend is accompanied by modest improvements in our core distress metrics, signaling potential stabilization in certain segments of the market. However, a closer look at property types reveals a tale of divergence—particularly between retail and hotel—offering critical takeaways for investors and stakeholders.

Distress Metrics Show Incremental Progress

Our research team tracks two key indicators of distress: delinquency rates and special servicing rates. In our latest report, the delinquency rate edged down from 8.0% in March to 7.9%, while the special servicing rate saw a more significant 40-basis-point reduction, landing at 9.7%. A year ago, these figures stood at 5.4% and 7.4%, respectively, underscoring how much the CRE landscape has evolved. These month-over-month improvements suggest that while challenges persist, the market may be finding its footing in select areas.

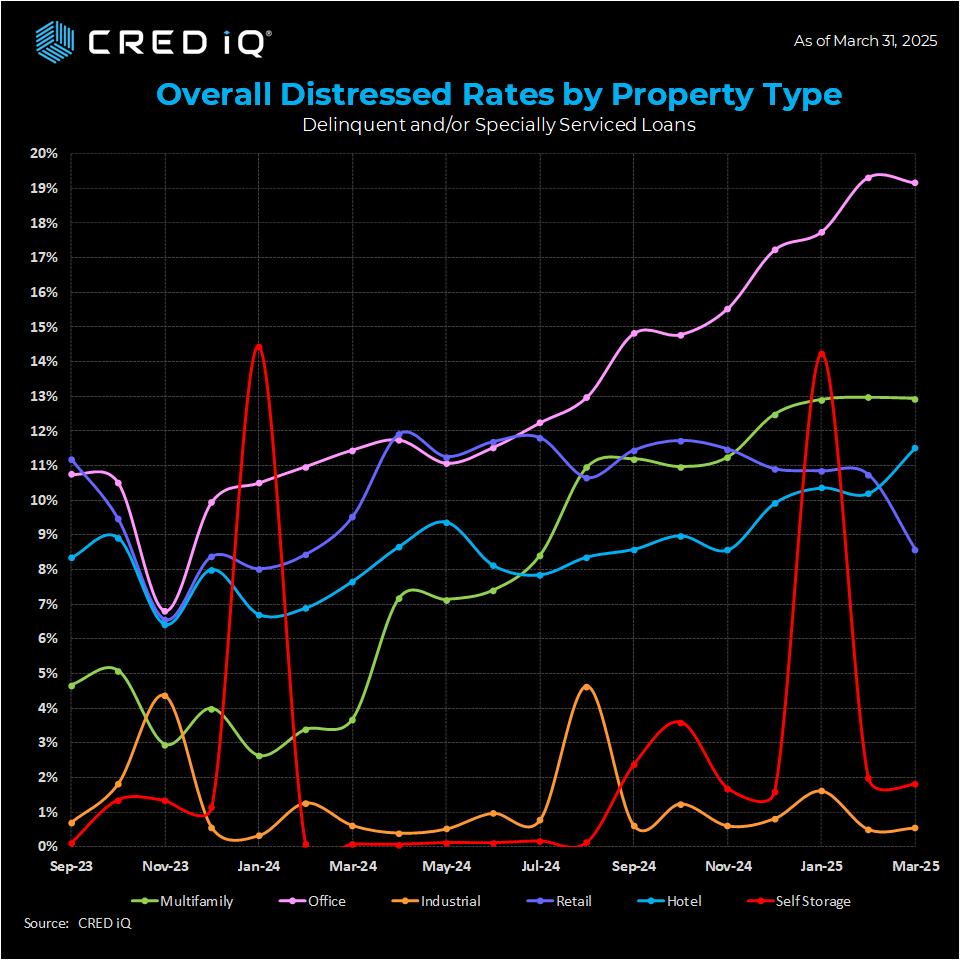

Segment Spotlight: Retail Shines, Hotel Struggles

Among property types, the office and multifamily segments remain the most distressed, though both posted relatively flat results. Office continues to lead the pack at 19.2% (down 10 basis points from March), while multifamily eased slightly to 12.9% (also down 10 basis points). These incremental declines hint at resilience, but the broader distress levels in these sectors still warrant close attention.

The real story this month lies in the contrasting fortunes of retail and hotel. Retail, which had been neck-and-neck with hotel in March, delivered a standout performance—its distress rate plummeted 210 basis points to 8.6%. This marks the fifth consecutive month of improvement for the sector and the largest drop in that streak. Factors such as adaptive reuse, strong consumer spending, or successful lease negotiations may be driving this positive momentum—a trend we’ll continue to monitor.

Meanwhile, the hotel segment moved in the opposite direction, with its distress rate climbing 130 basis points to 11.5%. This uptick brings hotel closer to overtaking multifamily as the second-most distressed property type. Rising operational costs, shifting travel patterns, or maturing loans could be contributing to this increase, making hotels a focal point for our next analysis.

Industrial and self-storage, as expected, remain bright spots. Industrial held steady at an impressively low 0.5% distress rate, while self-storage shaved 20 basis points to 1.8%. These segments continue to demonstrate stability amid broader market fluctuations.

Payment Status: A Mixed Picture

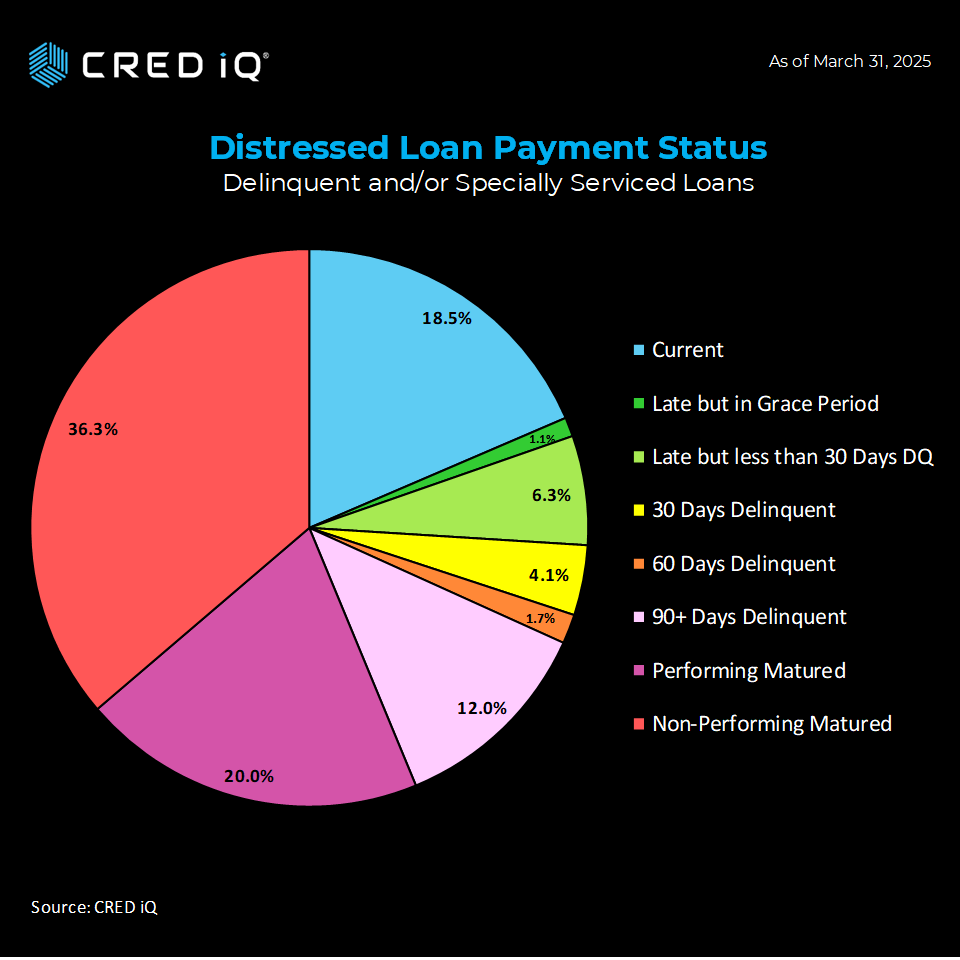

Digging deeper into payment statuses across approximately $55.6 billion in CMBS loans, we found:

- $10.3 billion (18.5%) are current,

- $14.0 billion (25.2%) are delinquent (including those within grace periods),

- $31.3 billion (56.2%) have passed their maturity date, with 20.0% performing and 36.3% non-performing.

These figures are largely unchanged from March, suggesting a steady—if uneven—state of payment performance across the portfolio.

Our Methodology

CRED iQ’s distress rate is a comprehensive measure that combines delinquency (30+ days past due) and special servicing activity, encompassing both performing and non-performing loans that fail to pay off at maturity. Our analysis focuses on CMBS properties securitized in conduits and single-borrower large loan structures, while we track Freddie Mac, Fannie Mae, Ginnie Mae, and CRE CLO metrics separately for a holistic view of the market.

What’s Next?

The second consecutive decline in our overall distress rate is a cautiously optimistic signal for the CRE sector. Retail’s impressive turnaround offers a glimmer of hope, though hotel’s rising distress reminds us that recovery is far from uniform. As we move forward, CRED iQ remains dedicated to providing actionable insights to help our clients navigate this dynamic landscape.

Stay tuned for our next update, and feel free to reach out to our team for a deeper dive into the data shaping today’s CRE market.

About CRED iQ

CRED iQ is a market data provider that offers a robust suite of data and software solutions tailored for commercial real estate and finance professionals.

With over $2.3 trillion of CRE loans, CRED iQ delivers instant access to a comprehensive range of financial data and analytics for millions of properties in every market. CRED iQ’s data and analytical capabilities are instrumental in helping investors, lenders and brokers make informed and strategic decisions critical to their business.

THE DATA, INFORMATION AND/OR RELATED MATERAL (“DELIVERABLES”) IS BEING OFFERED AS-IS/WHERE-AS CONDITION. CRED-IQ MAKES NO REPRESENTATION OR WARRANTY AS TO QUALITY OR ACCURACY OF SUCH DELIVERABLES BEING PURCHASED, WHETHER EXPRESS OR IMPLIED, EITHER IN FACT OR BY OPERATION OF LAW, STATUTE, OR OTHERWISE, AND CRED-IQ SPECIFICALLY DISCLAIMS ANY AND ALL IMPLIED OR STATUTORY WARRANTIES INCLUDING WARRANTIES OF MERCHANTABILITY AND OF FITNESS FOR A PARTICULAR PURPOSE, TECHNICAL PERFORMANCE, AND NON-INFRINGEMENT. WITHOUT LIMITING THE FOREGOING, YOU AS CUSTOMER ACKNOWLEDGE THAT YOU HAVE NOT AND ARE NOT RELYING UPON ANY IMPLIED WARRANTY OF MERCHANTABILITY OR OF FITNESS FOR A PARTICULAR PURPOSE OR OTHERWISE, OR UPON ANY REPRESENTATION OR WARRANTY WHATSOEVER AS TO THE DELIVERABLES IN ANY REGARDS WHATSOEVER, AND ACKNOWLEDGE THAT CRED-IQ MAKES NO, AND HEREBY DISCLAIMS ANY, REPRESENTATION, WARRANTY OR GUARANTEE THAT THE PURCHASE, USE OR COMMERCIALIZATION OF ANY DELIVERABLES WILL BE USEFUL TO YOU OR FREE FROM INTERFERENCE. BY ACCEPTANCE OF THE DELIVERABLES, YOU HEREBY RELEASE CRED-IQ AND ITS AFFILIATES AND AGENTS FROM ALL CLAIMS, DAMAGES AND LIABILITY ARISING HEREUNDER.