CRED iQ is hiring a senior software engineer. We’re looking for collaborative, forward-thinking software engineers to join the team and help build our next-generation financial analysis platform. You’ll be working on end-user products, data-ingestion pipelines, and all the pieces in-between that make for a seamless experience.

For the full job post and application details, please click here.

About CRED iQ

CRED iQ is a commercial real estate data, analytics, and valuation platform designed to unlock investment, financing, and leasing opportunities. CRED iQ provides real-time property, loan, tenant, ownership, and valuation data for all major commercial property types across the nation.

This week, CRED iQ calculated real-time valuations for 5 office properties that have major tenants with lease expirations in the next 6 months. Featured leases include a large block of space in the Midtown West submarket of Manhattan and spaces in suburban office complexes located across the Washington, DC, Memphis, and Dallas MSAs. Lease expirations are opportunities for tenant reps to source options and find solutions for clients. Additionally, lease expirations can serve as a preemptive signal of distress for CRE loans if prospects for leasing the newly vacant space are low.

The CRED iQ valuations factor in a base-case (Most Likely), a downside (significant loss of tenants), and dark scenarios (100% vacant). Base-Case valuations are provided for the properties below. For full access to the valuation reports including the Downside and Dark scenarios as well as full CMBS loan reporting, with detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

1740 Broadway

603,928 sf, Office, New York, NY 10019

L Brands is vacating approximately 418,000 sf of space upon lease expiration on March 31, 2022 at 1740 Broadway. The property, a 26-story office tower located in the Midtown West submarket of Manhattan, NY, secures a $308.0 million mortgage loan that has been on the servicer’s watchlist since April 2021. News of L Brands’ departure pre-dated the loan’s addition to the servicer’s watchlist, however, when a CBRE Research note first pointed out the fashion retailer’s impending move to 55 Water Street in March 2020. The property’s second largest tenant at origination, law firm Davis & Gilbert, also vacated its 95,000-sf space, equal to 16% of the GLA, at lease expiration in December 2020.

The timing of L Brands’ departure announcement is two-fold. First, there is a benefit of additional time to prepare to backfill the vacant space, and Blackstone, the loan sponsor, has taken advantage of the early notice to redevelop the building’s lobby and add new tenant amenities including a tenant-only gym, café, and lounge. Second, there was a disadvantage due to the announcement’s coincidence with the onset of the pandemic, which left many office tenants in the market uncertain about future needs of space. CRED iQ’s estimated occupancy for the property is 13%. The loan remains current in payment and has a maturity date of January 6, 2025. For the full valuation report and loan-level details, click here.

AARP is vacating approximately 76,000 sf of space at lease expiration on November 30, 2021 at the Rockville Corporate Center. The property, a two-building suburban office complex located in Rockville, MD, secures a $32.6 million mortgage loan that is scheduled to mature on May 6, 2022. AARP accounts for approximately 34% of the property’s GLA and was the primary tenant at 15 West Gude Drive. A large vacancy just 5 months prior to maturity could adversely impact the loan’s refinancing prospects. The property’s second building, located at 45 West Gude Drive, is fully leased to Montgomery County Public Schools through December 2031. CRED iQ estimates occupancy of 66% for the office complex following the departure of AARP. For the full valuation report and loan-level details, click here.

Regions Bank has a 108,731-sf lease expiration on December 31, 2021 at a suburban office complex located about 15 miles outside of Memphis, TN. Regions Bank is the largest tenant at the property and accounts for 30% of the GLA. The property, which consists of three buildings, secures a $25.2 million mortgage loan that has been on the servicer’s watchlist since December 2020. Regions Bank appears to be vacating the property at lease expiration. The space is being marketed as available and Colliers has the listing. Occupancy at the property declined to 72% during 2020 and the loss of Regions Bank would reduce occupancy even further to 42%. With loan maturity less than 4 months away, lease rollover issues at this property will likely need to be resolved before the borrower can secure refinancing. For the full valuation report and loan-level details, click here.

A 117,452-sf office building located in Hall Office Park in Frisco, TX is working through lease rollover issues. The property secures an $18.1 million mortgage loan that has been on the servicer’s watchlist since November 2020. The property’s largest tenant, Randstad Professional US, had a lease that expired in August 2021. The staffing agency occupied 40,991 sf of the building, equal to 35% of the GLA. Randstad’s original lease expired in April 2021, but the tenant negotiated a 4-month extension. The extension may have been used to buy time to facilitate a move to another building because Randstad signed a 31,884-sf lease at an office building in Plano, TX located 3 miles away in June 2021.

Schlumberger is the property’s second-largest tenant with a 39,190-sf lease, accounting for 33% of the GLA. Schlumberger’s lease expires on February 28, 2022. Commentary from the servicer’s watchlist indicates the tenant may reduce its footprint at lease expiration. A downsizing for full departure would create added distress to a building that was 80% occupied as of April 2021. Approximately 49% of the GLA is being marketed as available for lease. CRED iQ estimates that occupancy could decline to about 12%, accounting for departures of Randstad and Schlumberger. For the full valuation report and loan-level details, click here.

Kaplan University is vacating this 124,500-sf office building in Orlando, FL, which secures a $16.5 million mortgage loan. Kaplan, formerly a for-profit college, was the property’s sole tenant. The loan was added to the servicer’s watchlist in August 2021 and updated commentary indicates a 78,500-sf portion of the property may already be backfilled pending negotiations. The remaining vacant space is being marketed as available and CBRE has the listing. Assuming the 78,500-sf leasing deal comes to fruition, then occupancy at the property would be approximately 63%. The loan is scheduled to mature in December 2024 and has been current throughout its term. For the full valuation report and loan-level details, click here.

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. For full access to our loan database and valuation platform, sign up for a free trial below:

This week, CRED iQ calculated real-time valuations for 5 properties that are either vacant or dark, including two hotels that have been closed due to the pandemic and two vacant office buildings in the San Jose, CA MSA. Vacant or non-operational properties are opportunities for off-market transactions. In cases of distress, new ownership has the ability to infuse capital into a project and vacant suites are always on the radar of leasing brokers. For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

Empire Hotel & Retail

423 keys, Hotel, New York, NY 10023

The Empire Hotel, located in the Lincoln Square submarket of Manhattan, closed in March 2020 due to the pandemic and has been out of operation throughout 2021. The hotel, as well as 61,223 sf in retail space, secures a $169.3 million loan that transferred to special servicing in May 2021. The loan was modified shortly after the onset of the pandemic in May 2020 to allow the borrower to fund debt service payments with reserves. The modification proved to be insufficient in keeping the loan current and the borrower appears to be requesting for additional relief.

Multiple sources point to January 2022 as possible timeframe for reopening for the hotel, which operates independently. Despite zero incoming revenue from the hotel portion of property, the retail spaces have been operational on a limited basis throughout the pandemic, apart from the 16,000-sf rooftop lounge. Retail occupancy includes ground-floor retail tenants Duane Reade (12,557 sf) and Starbucks (2,676 sf). Still, the pandemic wasn’t the initial cause of distress for loan, which had a below breakeven DSCR of 0.78 during 2019 due to increases in operational leverage. For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

34,498 sf, Mixed-Use (Office/Retail), New York, NY10013

Last week’s WAR Report took us to the corner of Broadway and Howard Street in the SoHo submarket of Manhattan to evaluate the vacant 428 Broadway. We don’t have to look any further than across the street for another vacant property with 427 Broadway. The property is part of a 2-building portfolio that secures a $76.5 million mortgage loan. The debt stack also includes an $11.5 million mezzanine loan that was held by Jefferies LoanCore at origination. The second property that is part of the portfolio is 459 Broadway. The loan shares the same sponsor, Jacob Chetrit, as 428 Broadway. The loan transferred to special servicing in June 2021 and Rialto, as special servicer, is discussing potential workouts with the borrower.

427 Broadway is a five-story building that contains ground-floor and below-grade retail space in addition to four floors of office space. The vacant retail space was formerly occupied by American Apparel (8,498 sf), which vacated in July 2017. The vacant office space was formerly occupied by Night Agency (6,500 sf) and Psyop Media Company (19,500 sf). Psyop Media Company vacated ahead of its April 2025 lease expiration and is obligated to pay a termination fee of approximately $4.0 million. As mentioned last week, the high-street retail leasing environment in Manhattan remains extremely challenging, especially with a concentration of vacancies in the SoHo submarket. For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

Hotel on Rivington was vacant until about two weeks ago when the boutique Lower East Side hotel re-opened. The property had previously been closed since March 2020. Hotel on Rivington secures a $36.3 million loan that matures in March 2026. Despite the property having 0% occupancy for nearly 18 months, the loan has been current in payment. Servicer commentary also indicates a new owner may have assumed the mortgage loan with plans to invest additional capital into the hotel. The property was nearly sold for $65.0 million in November 2018 to the Kushner Companies but the deal ultimately fell through. The 20-story hotel contains 107 keys and is located in the Lower East Side on Manhattan, NY. For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

This 200,000-sf vacant office building is located in San Jose, CA and secures a $34.8 million mortgage loan. The property was formerly occupied by Broadcom as a single tenant; however, Broadcom vacated in May 2018, ahead of its May 2020 lease expiration. Broadcom paid a $2.5 million termination fee. In total, borrower has reserved about $4.5 million for leasing costs for the property, which is actively being marketed. Colliers has the listing and is marketing the property as a headquarters with flexibility as R&D or lab space and campus-like amenities such as an outdoor amphitheater and tennis courts. The loan has been current in payment; however, it has been over 2 years without positive cash flow at the property. For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

This 67,000-sf vacant office building is located in Mountain View, CA and secures a $21.6 million mortgage loan. The property was formerly occupied by tech firm Tintri as a single tenant through October 2018 when the company vacated. The vacant building was acquired by a joint venture between BioScience Properties Inc. and Harrison Street Real Estate Capital LCC for $40.75 million in February 2021 with a plan to reposition the building for life science use. CBRE has the listing and is marketing the space for flex, R&D, and life science use. The mortgage loan been current in payment despite 0% occupancy and negative net cash flow over the past few years. For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. For full access to our loan database and valuation platform, sign up for a free trial below:

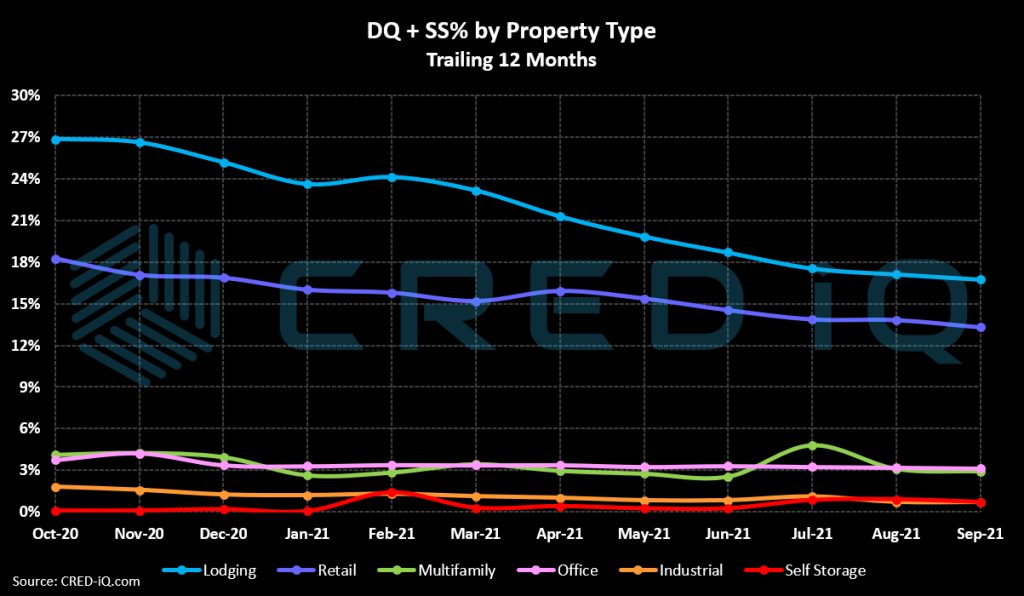

The overall delinquency rate declined for the 15th consecutive month since its peak in June 2020, continuing a trend of recovery from the spike in distressed assets caused by the pandemic. The delinquency rate, equal to the percentage of all delinquent specially serviced loans and delinquent non-specially serviced loans, for CRED iQ’s sample universe of $500+ billion in CMBS conduit and single-asset single-borrower (SASB) loans was 5.30%. CRED iQ’s special servicing rate, equal to the percentage of CMBS loans that have transferred to special servicing, was equal to 7.57%. Aggregating these two indicators of distress – delinquency rate and special servicing rate – into an overall distressed rate (DQ + SS%) equals 7.81% of CMBS loans that are specially serviced, delinquent, or a combination of both.

DQ = All delinquent loans in the conduit, SASB and CRE CLO universe, including specially serviced and non-specially serviced loans SS = All specially serviced loans in the conduit, SASB and CRE CLO universe, including current, delinquent and REO DQ + SS = All distressed loans in the conduit, SASB and CRE CLO universe that are delinquent, specially serviced, or a combination of both

By property type, lodging and retail had the highest individual delinquency rates. Delinquency for each property type declined compared to the prior month and each has exhibited an overall downward trend over the trailing twelve months. The lodging delinquency rate has made the most dramatic recovery over the past year, declining from just under 20% in October 2020 to approximately 11% in September 2021.

DQ = All delinquent loans in the conduit, SASB and CRE CLO universe, including specially serviced and non-specially serviced loans SS = All specially serviced loans in the conduit, SASB and CRE CLO universe, including current, delinquent and REO DQ + SS = All distressed loans in the conduit, SASB and CRE CLO universe that are delinquent, specially serviced, or a combination of both

Despite a clear signal of improvement in the lodging sector, this property type showed the most volatility when evaluating performance across markets. Lodging accounted for 75% of the biggest month-over-month changes when broken out by market, as exhibited in the table above.

CRED iQ monitors market performance for nearly 400 MSAs across the United States covering over $900 billion in outstanding CRE debt. Minneapolis, Louisville, New Orleans, Cleveland, and Milwaukee continue to be the MSAs with the highest rate of distressed properties, which is consistent with the prior month. This month, Sacramento overtook Allentown as the MSA with the lowest distressed rate among the Top 50. The majority of MSAs saw improvements with overall declines in the percentage of distressed properties. Only 8 of the Top 50 MSAs exhibited additional distress compared to the prior month. The Salt Lake City market had the greatest improvement with nearly a 30% decrease in the percentage of distressed properties. The improvement was largely driven by South Towne Center, a 1.1 million-sf regional mall that returned from special servicing to the master servicer after a loan modification.

This week, CRED iQ calculated real-time valuations for 5 distressed properties that have transferred to special servicing within the past 3 months, including a regional mall located in Lancaster, PA and 2 mixed-used properties located in Lower Manhattan. One of the highlighted properties, a medical condo located in the Upper East Side of Manhattan, transferred to special servicing only 8 months after origination and may have raised some eyebrows in the process.

The CRED iQ valuations factor in a base-case (Most Likely), a downside (significant loss of tenants), and dark scenarios (100% vacant). For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

Park City Center

1.4 million sf, Regional Mall, Lancaster, PA 17601

This $115.5 million loan failed to pay off at maturity on September 9, 2021 and transferred to special servicing. The borrower, Brookfield Property Partners, requested an extension, and KeyBank, as special servicer, is reviewing the request. The loan maturity was previously extended through a November 2020 modification agreement that required Brookfield to curtail $13.5 million in principal. Despite the maturity default, an additional $6.0 million in principal was curtailed in September, which could be related to a second extension. Overall, the loan has de-levered by approximately 14% from its original balance of $135.0 million. Unfortunately, the decline in value of the collateral property since origination may have been steeper than the principal paydowns to date.

The loan is secured by Park City Center, a regional mall located in Lancaster, PA that is anchored by JCPenney, Boscov’s, Kohl’s, and Round1 Entertainment – although Boscov’s owns its land and improvements. These tenants may serve as traditional anchors but much of the foot traffic is derived from the Apple Store, which had plans at loan origination to expand its space into an updated store concept. The presence of the Apple Store is one of the few positives for the asset, which was hit hard by the pandemic and co-tenancy clauses from previous closures of Sears and The Bon-Ton. Since loan origination, the following tenants have vacated or no longer have a presence at Park City Center: Williams-Sonoma, TGI Friday’s, Justice, GNC, Christopher & Banks, Finish Line, The Walking Company, Motherhood Maternity, and Clarks. Net cash flow at the property declined approximately 37% from TTM June 2019 through year-end 2020, which corresponded to a significant decline in value for the property. A June 2019 appraisal for the property indicated an LTV of 53%; however, CRED iQ’s Base-Case valuation implies a more conservative LTV closer to 70% even after reductions in principal over the past 2 years. With Brookfield actively looking for refinancing, leverage levels and the potential contribution of additional equity could be key factors for getting a deal done for mortgage originators and other lenders. For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

53,418 sf, Mixed-Used (Office/Retail), New York, NY 10013

This $60.0 million loan transferred to special servicing on September 2, 2021 due to delinquency. This distressed loan is yet another product of the fallout from the struggles of WeWork, which served as a primary tenant. WeWork had leased 77% of the collateral property’s GLA at origination, but a lease termination was approved by the lender. The lease termination fee may have been in excess of $3.0 million, according to servicer data. Multiple workouts are being evaluated including foreclosure or a note sale.

The floating-rate loan was originated in March 2020 by LoanCore Capital as bridge financing to allow the borrower to recapitalize the collateral property, which is a mixed-use office building with ground floor retail located in the SoHo submarket of Manhattan. The loan sponsor, Jacob Chetrit, had planned to lease the ground-floor and below-grade retail space, which totaled 12,203 sf and was vacant at origination. However, the retail space remains vacant with a tough leasing environment for high-street retail in Manhattan. The departure of WeWork now leaves the entire building vacant. For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

This $19.6 million loan transferred to special servicing on July 23, 2021 and is a potential refinance opportunity. The loan failed to pay off at maturity in April 2021 and the borrower, Arciterra, requested an extension that was approved. However, the loan originator, Money360, Inc., was concurrently working on a refinance solution. Both extension and refinancing alternatives are being evaluated.

The loan is secured by a leasehold interest in a retail property located in Waimea, HI on the Big Island. The property serves as a captive retail destination for travelers staying at the Mauna Lani resort and features primarily restaurant and apparel tenants. Although Hawaii tourism levels continue to improve from pandemic lockdown lows in 2020, the property has hasn’t improved occupancy greater than 83%. Occupancy was approximately 91% at loan origination. Further complicating matters, annual ground rent for the property is in excess of $800,000.

Using CRED iQ’s newly launched COMPS software, our team identified King’s Shops as a highly relevant comparable property. Similar to the Shops At Mauna Lani, King’s Shops is a captive retail development that serves guests of the Waikoloa Beach Marriott Resort & Spa. The King’s Shops recently went into receivership following its own struggles with the disruption of Hawaiian tourism caused by the pandemic. For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

32,285 sf, Mixed-Use (Retail/Office), New York, NY 10013

This $18.65 million loan transferred to special servicing on July 9, 2021 for the purpose of inking a loan modification. The collateral property had been adversely impacted by the pandemic and occupancy has declined since loan origination in March 2019. The loan modification was negotiated with LNR Securities Holdings as special servicer and will likely be designed to provide relief and give the borrower an opportunity to address the property’s vacancy.

The collateral property is a 32,285-sf mixed-used building located in the Tribeca submarket of Manhattan. With a high volume of vacancies up and down Broadway, the ground-floor retail portion of the building may take relatively longer to lease compared to any vacant office space. The property was 67% occupied at the time of its transfer to special servicing. For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

This $4.5 million loan transferred to specially servicing on August 24, 2021, just 9 months after origination. Special servicer commentary indicated a receiver was appointed for the collateral property. It is worth noting that the borrower sponsor, Jean-Francois Simon, was subject to ongoing litigation at the time of loan origination in December 2020. The loan is secured by a 7,751-sf medical office condominium unit located in the Upper East Side of Manhattan. The office condominium is on the ground floor and is part of a larger residential building with 67 units and 2 other office units. The property is leased to Fifth Avenue Surgery Center, Inc. through December 2025. For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. For full access to our loan database and valuation platform, sign up for a free trial below:

This week, CRED iQ reviewed the commercial real estate lending landscape and highlighted 5 properties that have secured financing within the past month. Using the CRED iQ platform’s Comps functionality, which features propriety Comps scoring for the CRE loan universe, we compared lending terms and loan structures to get a sense of the trends in the CRE lending environment. Additionally, we provided valuations for each asset to evaluate leverage levels in relation to the originators’ LTVs, similar to last month’s WAR Report on the lending landscape. The CRED iQ valuations factor in a base-case (Most Likely), a downside (significant loss of tenants), and dark scenarios (100% vacant). For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

Parkway Irvine

209,831 sf, Flex Industrial, Irvine, CA 92618

A $37.0 million loan was originated by Société Générale Financial Corporation (SocGen) on August 30, 2021 to refinance existing debt of $16.7 million and return approximately $19.6 million in equity to the loan sponsor, Paul Queyrel – president of TriQuest Development Company. The loan was structured with a 10-year term and requires interest-only payments at a rate of 3.13%. The loan will be locked out from prepayment for 2 years, and after lockout will require a yield maintenance charge for prepayment prior to its open period. CRED iQ’s most relevant comp is the $15.0 million Newport Court loan, which was originated in January 2021 and has an interest rate of 2.97%. Newport Court is secured by a 212,283-sf industrial property that is also located in Irvine, CA.

The Parkway Irvine loan is secured by fee interest in a 209,831-sf industrial property that was developed in 1989 and features 12 buildings set across 14 acres located in Irvine, CA. Most of the buildings operate as single-story flex buildings and approximately 34% of the GLA is primarily used as office space. The property was 88% occupied as of August 16, 2021 and no individual tenants account for greater than 4% of the GLA. With such a granular rent roll, lease rollover management will be relevant in 2023 and 2024 when leases accounting for a combined 52% of the GLA are scheduled to expire. A July 23, 2021 appraisal valued the property at $62.4 million, equal to $279/sf, which implied an LTV of 59.30% and a capitalization rate of 5.47% based on the originator’s underwritten NCF. For the full valuation report and loan-level details, click here.

Subject Property

Name

Parkway Irvine

Address

15375 Barranca Parkway Irvine, CA 92618

Type

Industrial

Subtype

Flex

Building Size

209,831 sf

Year Built

1989

Submarket

Irvine Spectrum

County

Orange

MSA

Los Angeles-Long Beach-Santa Ana, CA

Origination Date

08/30/2021

Loan Amount

$37,000,000

Interest Rate

3.13%

Valuation

Appraisal Value

$62,400,000

Appraisal Date

07/23/2021

Appraisal LTV

59.30%

MyQ Concluded Value

$60,440,000

15-17 Park Avenue

97 units, Multifamily, New York, NY 10016

A $31.0 million loan was originated by SocGen on August 16, 2021 to refinance existing debt on a 97-unit high-rise multifamily building located on the edge of the Murray Hill submarket of Manhattan, NY. The 10-year interest-only loan has an interest rate of 3.34%. The loan will be locked out from prepayment for 2 years, and defeasance will be permitted after lockout through the remainder of the loan term. The borrower sponsor for the loan is Scott Goldstein. CRED iQ’s highest scoring comp is the $14.8 million 234-236 East 24th Street loan, which was originated in March 2020 and has an interest rate of 3.10%. The comparable loan is secured by a 36-unit multifamily property located slightly south of the subject, closer to Kips Bay.

The 15-17 Park Avenue mortgage loan is secured by fee interest in a 16-story multifamily property that contains 85 units that lease at market rate and 11 units that are rent stabilized. One unit is reserved for the superintendent and the property features an additional 2,810 sf of commercial space. Average asking rent for Q1 2021 was $3,802 per unit, which represented a 5% decline compared to 2020 and a 21% decline compared to 2019. The rent declines exemplify the downward pressure on rents caused by the pandemic. The property typically operated with about 98% occupancy pre-COVID but occupancy declined to 93%/94% for much of 2020 and 2021. Occupancy was listed as 100% as of July 20, 2021, including all residential and commercial units. The property was appraised for $50.1 million as of July 8, 2021, equal to $516,500/unit, which implied an LTV of 61.90% and a capitalization rate of 4.27% based on the originator’s underwritten NCF. For the full valuation report and loan-level details, click here.

Subject Property

Name

15-17 Park Ave

Address

15-17 Park Avenue New York, NY 10016

Type

Multifamily

Subtype

High Rise

Building Size

97 units

Year Built

1924

Submarket

Murray Hill

County

New York

MSA

New York-Northern New Jersey-Long Island, NY-NJ-PA

Origination Date

08/16/2021

Loan Amount

$31,000,000

Interest Rate

3.34%

Valuation

Appraisal Value

$50,100,000

Appraisal Date

07/08/2021

Appraisal LTV

61.90%

MyQ Concluded Value

$44,590,000

Murrieta Spectrum

172,357 sf, Mixed-Use (Retail/Office), Murrieta, CA 92562

A $23.0 million loan was originated by UBS on August 27, 2021 to refinance existing debt on a 172,357-sf retail property located in Murrieta, CA, just north of Temecula. The loan has a 10-year term and requires amortizing debt service payments based on a 30-year schedule with an interest rate 3.73%. The loan is locked out from prepayment for 1 year, and after lockout will require a yield maintenance charge for prepayment prior to its open period. CRED iQ’s most relevant comp is the $16.2 million Bel Villaggio loan, which was originated in February 2020 and has an interest rate of 3.57%. Bel Villaggio is located in nearby Temecula and has similar size and use as Murrieta Spectrum, although with a much more granular rent roll.

Although property information provided for Murrieta Spectrum lists the property type as mixed-use, the collateral for the loan is primarily designed and operated as a retail center. The largest tenants are Ashley Furniture and Savers Thrift Store, which are both retail tenants and account for a combined 45% of the GLA. The third-largest tenant, STG International, accounts for another 15% of the GLA, but the tenant will not take occupancy until October. Prior to the lease signing with STG International, which will bring occupancy to 95%, the property had operated at approximately 80% occupancy for several years. The property was appraised for $45.25 million as of April 22, 2021, equal to $263/sf, which implied an LTV of 50.90% and a capitalization rate of 5.80% based on the originator’s underwritten NCF. For the full valuation report and loan-level details, click here.

Subject Property

Name

Murrieta Spectrum

Address

25125 Madison Avenue Murrieta, CA 92562

Type

Retail

Subtype

Community Center

Building Size

172,357 sf

Year Built

2005

Submarket

Temecula

County

Riverside

MSA

Riverside-San Bernardino-Ontario, CA

Origination Date

08/27/2021

Loan Amount

$23,000,000

Interest Rate

3.73%

Valuation

Appraisal Value

$45,250,000

Appraisal Date

04/22/2021

Appraisal LTV

50.90%

MyQ Concluded Value

$37,310,000

Nanogate North America (Techniplas)

266,180 sf, Industrial, Mansfield, OH 44903

This $9.5 million loan was originated by UBS on August 20, 2021 to fund the sale-leaseback acquisition of a manufacturing facility located in Mansfield, OH. The property was acquired by MAG Capital Partners LLC and will be solely leased to its previous owner, Nanogate North America, a component manufacturing firm. The tenant was acquired by Techniplas, which is also an engineering and manufacturing company, and the property serves as the company’s only US location. The 10-year loan has an interest rate of 4.20% and requires amortizing debt service payments based on a 30-year schedule. The loan will be locked out from prepayment for 2 years, and after lockout defeasance will be permitted through the remainder of the loan term. Due to the collateral property’s location in a tertiary market, many of the loan’s comps had relatively low scores. However, two notable loans secured by single-tenant industrial properties within 50 miles of the subject included Revere Plastics, which was originated in March 2019 and has an interest rate of 4.41%, and 9040 Smith’s Mill Road, which was originated in March 2020 and has an interest rate of 3.70%.

The Techniplas manufacturing facility comprises 3 buildings set across a 23-acre parcel. The tenant signed a 20-year lease at the property that is scheduled to expire 10 years beyond loan maturity. The property was appraised for $15.25 million, equal to $57/sf, as of June 17, 2021, which implied an LTV of 62.30% and a capitalization rate of 6.33% based on the originator’s underwritten NCF. For the full valuation report and loan-level details, click here.

Subject Property

Name

Nanogate North America

Address

150 East Longview Avenue Mansfield, OH 44903

Type

Industrial

Subtype

Manufacturing

Building Size

266,180 sf

Year Built

1947

Submarket

Mansfield

County

Richland

MSA

Mansfield, OH

Origination Date

08/20/2021

Loan Amount

$9,500,000

Interest Rate

4.20%

Valuation

Appraisal Value

$15,250,000

Appraisal Date

06/17/2021

Appraisal LTV

62.30%

MyQ Concluded Value

$14,750,000

Westgate Shopping Center

47,331 sf, Retail, San Antonio, TX 78216

RPD Catalyst, LLC secured a $7.2 million loan from LMF Commercial (formerly Rialto Mortgage Finance) on August 27, 2021, to refinance existing debt on a 47,331-sf neighborhood center located in San Antonio, TX. The 10-year loan has an interest rate of 4.06% and requires amortizing debt service payments based on a 30-year schedule. One of the highest scoring comps for this loan is University Square Shopping Center, which secures a loan that was originated in May 2019 and carries an interest rate of 4.35%.

Westgate Shopping Center is anchored by Guitar Center, which accounts for 71% of the property’s GLA. The anchor tenant has been severely impacted by the pandemic and recently emerged from bankruptcy in December 2020. Guitar Center’s lease expires in November 2026, which is about halfway through the loan term. The ongoing financial health of Guitar Center as well as a favorable renewal outcome at lease expiration will be the primary credit drivers for this loan. Positive news regarding Guitar Center broke in recent days after a Debtwire report indicated the company filed with the SEC to register for an IPO. The property was 100% occupied at origination and had an appraisal value of $10.4 million, equal to $219/sf, as of July 15, 2021. The appraisal implied an LTV of 69.20% and a capitalization rate of 6.80% based on the originator’s underwritten net cash flow. For the full valuation report and loan-level details, click here.

Subject Property

Name

Westgate Shopping Center

Address

7311 San Pedro Avenue San Antonio, TX 78216

Type

Retail

Subtype

Community Center

Building Size

47,331 sf

Year Built

1965

Submarket

Airport

County

Bexar

MSA

San Antonio, TX

Origination Date

08/07/2021

Loan Amount

$7,200,000

Interest Rate

4.06%

Valuation

Appraisal Value

$10,400,000

Appraisal Date

07/15/2021

Appraisal LTV

69.20%

MyQ Concluded Value

$9,700,000

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. For full access to our loan database and valuation platform, sign up for a free trial below:

This week, CRED iQ calculated real-time valuations for 5 distressed multifamily properties that secure GNMA loans. Ginnie Mae loans secured by distressed properties as well as loans with near-term maturities are sources for intriguing opportunities within the multifamily sector that expand into several property sub-types, including seniors housing and workforce housing. Mortgage originators, distressed investors, and commercial brokers are able to search CRED iQ’s database of approximately 15,000 Ginnie Mae loans totaling $138 billion in outstanding debt for their next opportunity. The properties featured in this week’s WAR Report secure a subset of the largest distressed Ginnie Mae loans by outstanding balance that are at least 90 days delinquent.

CRED iQ valuations factor in a base-case (Most Likely), a downside (significant loss of tenants), and dark scenarios (100% vacant). For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

Lucas Place Lofts

130 units, Multifamily, Kansas City, MO 64105

GNMA 2015-36178M2A8

This $18.4 million loan, which is 90 days delinquent, is secured by a 130-unit multifamily loft conversion property located in Kansas City’s Garment District. The high-rise apartments were redeveloped from commercial use in 2010 and converted to loft-style units. The loan was issued through HUD’s 221(d)(4) program to facilitate the construction and rehabilitation of multifamily properties for moderate-income families, elderly, and the handicapped. The property also operates under a Chapter 353 Tax Abatement until 2023, which is an incentive for the redevelopment of blighted areas. The tax abatement was facilitated through the Missouri Department of Economic Development. Love Funding originated the loan in October 2012 and maturity is scheduled for March 2054. After the expiration of the tax abatement, property taxes for the property have potential to increase as much as 10 times the current burden. CRED iQ’s Base-Case valuation uses estimates for fully unabated property taxes. For full access to the valuation reports as well as full CMBS and GNMA loan reporting, including borrower contact information, sign up for a free trial here.

Menorah Campus Inc.

328 units, Seniors Housing, Getzville, NY 14068

GNMA 2010-3620ANWH9

This $17.4 million loan is over 120 days delinquent and is secured by a 328-unit residential care facility located about 10 miles northeast of Buffalo, NY, in close proximity to the University at Buffalo campus. The mortgage is a Section 232 loan, which facilitates the construction of assisted living facilities under the FHA’s mortgage insurance program. The loan was originated in 1991 by Berkadia Commercial Mortgage and carries a 40-year term.

The delinquency may be related to a pending sale of the property that has been held up due to pending approval by state regulators. Elderwood Administrative Services agreed to acquire the entire Weinberg Campus, which included the collateral property, in late 2017. However, the closing of the sale transaction has been delayed for several years. Prior to the announcement of the acquisition, the Menorah Campus reportedly suffered from increases in expense growth and fewer reimbursements. The property generated about $5.1 million in revenue but still had an operating loss of over $1.0 million. The sales agreement called for the entire Weinberg Campus, which includes Menorah Campus among other properties, to be acquired for $47.0 million. For full access to the valuation reports as well as full CMBS and GNMA loan reporting, including borrower contact information, sign up for a free trial here.

Oasis at 56th

124 units, Multifamily, Indianapolis, IN 46254

GNMA 2021-3617BWEF8

This $17.0 million loan is 90 days delinquent and is secured by a 124-unit assisted living facility located in suburban Indianapolis. The mortgage loan was originated in November 2017 by Walker & Dunlop and has a 40-year term. Similar to the Menorah Campus, detailed above, the Oasis at 56th property was financed through the FHA’s Section 232 program to aid in the development of assisted living facilities. The property was developed from the ground up for a cost of approximately $27.0 million and opened June 2019. Operations are managed by Gardant Management Solutions. For full access to the valuation reports as well as full CMBS and GNMA loan reporting, including borrower contact information, sign up for a free trial here.

Chatham Manufacturing Company (Mill 800 Apartments)

166 units, Multifamily, Winston-Salem, NC 27101

This $16.3 million loan, which is over 120 days delinquent, is secured by a 166-unit multifamily conversion located in Winston-Salem, NC. The property was formerly a manufacturing facility that produced a wide range of products from textiles to military equipment. The property, which now operates as Mill 800 Apartments, is the first phase of a mixed-use project that is planned to include additional office and retail space. Similar to Lucas Place Lofts, detailed above, the Mill 800 Apartments loan was issued through HUD’s 221(d)(4) program to aid development of blighted areas. The property was originally acquired in 2012. The 40-year Ginnie Mae loan was originated in 2014 and the apartments completed construction in 2016. For full access to the valuation reports as well as full CMBS and GNMA loan reporting, including borrower contact information, sign up for a free trial here.

Saucon Valley Manor Senior Living

207 units, Seniors Housing, Hellertown, PA 18055

GNMA 2012-36177YHY5

This $16.3 million loan is 90 days delinquent and is secured by a 207-unit senior living facility located about 10 miles east of Allentown, PA. The facility is part of a 5-property regional network of senior living facilities and offers multiple levels of care, including assisted living, independent living, memory care, and personal care. The property is about 147,782 sf and sits on a 2.6-acre parcel. The loan was issued through HUD’s 223(f) program and carries a 35-year term. M&T Realty Capital Corporation originated the mortgage in December 2012 and maturity is scheduled in January 2048. For full access to the valuation reports as well as full CMBS and GNMA loan reporting, including borrower contact information, sign up for a free trial here.

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. For full access to our loan database and valuation platform, sign up for a free trial below:

This week, CRED iQ calculated real-time valuations for 5 retail properties that are owned by Washington Prime Group (WPG), which declared bankruptcy on June 13, 2021. WPG made headlines late last week just before the beginning of Labor Day weekend when the shopping center REIT emerged from bankruptcy. A large part of the bankruptcy proceedings centered around the valuation of WPG’s assets, including its portfolio of over 100 retail properties. Many of WPG’s retail properties are encumbered by first lien mortgages that have been securitized in CMBS, including Dayton Mall and Brunswick Square, which were last featured in the August 3rd WAR Report. This week’s updated valuations aim to provide guidance for WPG properties with the highest amounts of outstanding mortgage debt.

CRED iQ valuations factor in a base-case (Most Likely), a downside (significant loss of tenants), and dark scenarios (100% vacant). For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

Pearlridge Center

903,692 sf, Regional Mall, Oahu, HI 96701

This $225.0 million loan ($130.4 million in senior debt and $94.6 million in subordinate debt) is secured by a combination of fee and leasehold interests in a super-regional mall complex located 9 miles outside of Honolulu, HI. Pearlridge Center is one of WPG’s most valuable properties, consisting of multiple phases. The Uptown portion of the property is anchored by Macy’s, TJ Maxx and Ross Dress for Less. The Downtown portion of the property was formerly anchored by a Sears, which is now vacant, and features a CVS as well as a movie theater. There is also an office portion of the property that consists of an 8-story building. Overall occupancy at the property remained stable at 91% throughout 2020 despite adverse impacts from the pandemic. The loan appeared on the master servicer’s watchlist during 2020 and 2021, citing the potential need for COVID-19 relief; however, the loan remained current in payment. Pearlridge Center was even able to avoid special servicing during WPG’s bankruptcy proceedings. Still, the pandemic has taken a toll on financial performance. NCF for 2020 was $19.7 million, which was a 13% decline from the prior year. The mortgage loan is scheduled to mature in June 2025. For the full valuation report and loan-level details, click here.

Waterford Lakes Town Center

691,265 sf, Power Center, Orlando, FL 32828

This $174.0 loan transferred to special servicing on March 31, 2021, which was before WPG’s bankruptcy filing. The transfer reason was cited as imminent non-monetary default and was likely affiliated with the impending bankruptcy. A forbearance agreement was signed in May 2021 that would grant WPG temporary relief from KeyBank, as special servicer, pursuing any rights and remedies related to the non-monetary default.

Waterford Lakes Town Center is one of WPG’s better positioned relative to its whole portfolio with its power center layout and location. The open-air retail center is located in Orlando, FL and is anchored by a Super Target, which does not serve as collateral for the mortgage loan. Updated servicer commentary stated the property was 96% occupied, although we anticipate elevated lease rollover risk prior to loan maturity in May 2029. The 5 largest tenants – Regal Cinemas, Best Buy, JOANN Fabrics, Bed Bath & Beyond, and Ross Dress for Less – all have lease expirations prior to loan maturity. All of these tenants, except for Bed Bath & Beyond, have a 5-year extension option. Four out of the 5-largest tenants have go-dark provisions in their lease agreements, which was a cause for concern during the early stages of the pandemic and remains a peripheral risk through loan maturity. For the full valuation report and loan-level details, click here.

Scottsdale Quarter

541,971 sf, Lifestyle Center, Scottsdale, AZ 85254

This $165.0 million loan ($95.0 million in senior debt and $70.0 million in subordinate debt) transferred to special servicing on March 22, 2021. Similar to Waterford Lakes Town Center, the transfer was affiliated with WPG’s eventual bankruptcy filing in June 2021. KeyBank, as special servicer, indicated that it would not enforce an event of default related to WPG’s bankruptcy. As part of that agreement, cash management provisions were put in place, but such provisions may be lifted now that WPG has exited bankruptcy.

The loan is secured by a mixed-use lifestyle center located in Scottsdale, AZ comprising of 66% retail and 33% office space. Primary retail tenants include Apple and Restoration Hardware. Primary office tenants include Starwood Hotels, Spaces – a coworking Regus affiliate, and Maracay Homes. WPG recently announced a positive leasing development for the retail portion of the property, stating that a lease has been signed with Landmark Theatres, which will backfill the vacant movie theater space that was formerly occupied by iPic Theaters. Notable retail tenants that have vacated since loan origination include H&M and Nike, which accounted for an aggregate 8% of the property’s GLA. CRED iQ estimates occupancy of 87% following the new lease with Landmark Theaters. For the full valuation report and loan-level details, click here.

Cottonwood Mall

410,832 sf, Regional Mall, Albuquerque, NM 87114

This $91.8 million loan transferred to special servicing on June 17, 2021 due to WPG’s bankruptcy. Unlike the previous 3 properties discussed, Cottonwood Mall is a weaker asset within WPG’s portfolio and the REIT classified the mall as a non-core asset. Updated commentary for the loan indicated WPG requested for a deed-in-lieu of foreclosure agreement with Midland Loan Services, the special servicer. Following receivership and a transfer of title, the mall would then need to be liquidated. The mortgage loan was over 90 days delinquent.

The loan is secured by 410,832 sf of in-line space at the Cottonwood Mall, which has five non-collateral anchor pads. Dillard’s (170,610 sf) and JCPenney (124,656 sf) are the two largest anchors in operation. There is also a 164,978-sf anchor pad that was formerly occupied by Macy’s but the space was backfilled by Hobby Lobby and 2 furniture stores. There is a 106,000-sf anchor pad that was formerly occupied by Sears and remains vacant. Conn’s HomePlus is the 5th non-collateral anchor with an 84,048-sf parcel. Notable collateral tenants include Regal Cinemas, Old Navy, and Ulta. For the full valuation report and loan-level details, click here.

Westminster Mall

771,844 sf, Regional Mall, Westminster, CA 92683

This $74.1 million loan is secured by 771,844 sf of a regional mall located in Orange County, CA. Westminster Mall features 4 anchor pads – Macy’s, a vacant former Sears, Target, and JCPenney. Macy’s and the vacant Sears space do not serve as collateral for the loan while Target and JCPenney own their improvements and operate pursuant to a ground lease with WPG. The mall was reported to be 88% occupied; however NCF declined sharply in 2020. The Westminster Mall generated NCF of $4.7 million during 2020, which was a 51% decline compared to origination. Despite cash flow issues, the property has a desirable location in Orange County with redevelopment potential and underlying land value.

The loan has not yet transferred to special servicer despite a below breakeven DSCR during 2020. A favorable tax appeal ruling could have potential to alleviate potential debt service coverage issues; however, the decline in NCF remains a major concern. The loan has been on the servicer’s watchlist since December 2019. For the full valuation report and loan-level details, click here.

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. For full access to our loan database and valuation platform, sign up for a free trial below:

The overall delinquency rate declined for the 14th consecutive month since its peak in June 2020 and broke below 6% this month. Although the past year has shown a consistent trend in lower delinquencies, the recovery of distressed assets still has some distance before reaching pre-pandemic levels of sub-3%. Lodging and retail are still the leaders by property type with the highest individual delinquency rates; although, several hotel markets have posted delinquency declines this month including Kansas City, Los Angeles, Raleigh, and Pittsburgh. New Orleans was among the lodging markets that had the highest month-over-month increase in delinquency.

CRED iQ monitors market performance for nearly 400 MSAs across the United States. Below is a summary of the default rates for the 50 largest metros segmented by property type. For these 50 MSAs, the highest delinquency rate was in Minneapolis, followed by Louisville and New Orleans. The New Orleans market saw the largest month-over-month increase in delinquency, which allowed the MSA to surpass Cleveland amongst the regions with the highest delinquency rates. Allentown and Sacramento reported the lowest delinquency rate among the Top 50 MSAs. The most significant month over-month decline in delinquency was in the San Francisco market, which was attributed to the $1.5 billion Parkmerced loan paying current after a 30-day delinquency in July.

By property type, the hotel and retail sectors remain the largest contributors to the delinquency percentages for the majority of these statistical areas. Loans backed by self-storage, multifamily, and industrial facilities posted the lowest delinquency rates for most of these markets.

This week, CRED iQ calculated real-time valuations for 5 regional malls that have had title transfers in the past year and are now REO. The updated valuations serve as a follow-up to our August 18 blog – CRED iQ in the News – Regional Mall Distress. The featured assets are the 5 largest malls, by outstanding debt, that have become REO since the onset of the pandemic. One of the featured properties, Oakdale Mall, reportedly has secured a buyer with major redevelopment plants. Check out the commentary below for more detail! CRED iQ valuations factor in a base-case (Most Likely), a downside (significant loss of tenants), and dark scenarios (100% vacant). For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

Town Center at Cobb

559,940 sf, Regional Mall, Kennesaw, GA 30144

This property, which has outstanding debt of $172.5 million, has been with the special servicer since June 2020. Title to the property transferred to KeyBank, as special servicer, from Simon Property Group in January 2021 via foreclosure. KeyBank appears to still be in the process of assessing the timeline for liquidation, although March 2022 was provided as an estimated resolution date.

The Town Center at Cobb, located approximately 25 miles northwest of Atlanta, features 5 anchor pads that include 2 separate Macy’s boxes, a vacant former Sears box, a JCPenney, and a Belk. The REO portion of the property only includes the ground and improvements for the 128,819-sf Belk parcel as the other 4 pads did not secure the mortgage debt. Additionally, Belk has a near-term lease expiration in August 2022. An updated appraisal of $130.4 million ($233/sf) was reported last August and was equal to a 60% decline in value since the mortgage loan was originated. CRED-iQ’s Base-Case Valuation calculates a lower figure given uncertainty regarding Belk’s lease renewal and continued occupancy declines. For the full valuation report and loan-level details, click here.

Florence Mall

384,111 sf, Regional Mall, Florence, KY 41042

This property, which has outstanding debt of $89.4 million, has been with the special servicer since July 2020. Florence Mall, located in the suburbs of Cincinnati, OH, was formerly owned by Brookfield Property Partners but the firm agreed to a deed-in-lieu of foreclosure agreement with KeyBank in January 2021. The REO portion of the property solely consists of in-line space and a 68,324-sf movie theater outparcel. A vacant former Sears box, 2 separate Macy’s boxes, and a JCPenney make up the non-collateral anchor mix.

Updated servicer commentary stated the property was 82% occupied. The last full-year financials for the property indicated a DSCR of 2.16 for 2019, which is a prime example of the acceleration of credit deterioration brought on by the pandemic in the form of tenant departures, rent collection issues, and reduced foot traffic. JLL has been put in place to manage the property until the mall can be put to market for a liquidation sale. For the full valuation report and loan-level details, click here.

Southland Mall

660,736 sf, Regional Mall, Cutler Bay, FL 33189

This property, which has outstanding debt of $65.2 million, has been with the special servicer since April 2020. KeyBank, as special servicer, pursued foreclosure on the mall and acquired title to the property in March 2021. Southland Mall is located about 20 miles south of Miami and features 4 anchor parcels: a vacant former Sears, Macy’s, JCPenney, and Regal Cinemas. Sears and Macy’s are owned by separate entities and are not part of the REO collateral. However, the REO title vesting includes a 148,841-sf freestanding retail strip located to the north of the mall that is leased to a 28,450-sf Ross Dress for Less and was leased to a former K-Mart, which is now partly occupied by a church.

Prior to the mall’s foreclosure, it was encumbered by floating-rate mortgage debt as well as $41.0 million in mezzanine debt, which equated to a 91% LTV based on cumulative debt at origination. Prospective buyers will likely be concerned with lease rollover risk at the property as leases for the three-largest tenants, accounting for 28% of the GLA, are scheduled to expire in 2022. For the full valuation report and loan-level details, click here.

Newgate Mall

497,962 sf, Regional Mall, Ogden, UT 84405

This property, which has outstanding debt of $58.0 million, has been with the special servicer since March 2020. Rialto foreclosed on the property and acquired title from Time Equities Inc. in March 2021. The mall is now managed by The Woodmont Company and the sale of the asset is targeted for early-2022. The Newgate Mall, located 35 miles north of Salt Lake City, has 3 anchor pads consisting of a 149,624-sf vacant former Sears, Dillard’s, and a Burlington Coat Factory. Dillard’s and Burlington are owned by separate entities and are not part of the REO offering. The Burlington space has turned over several times in recent history, with the box previously occupied by GlowGolf and Mervyn’s prior to that. The REO portion of the property also includes a 61,970-sf junior anchor Cinemark movie theater and a DownEast Home & Clothing, which backfilled a former Sports Authority. For the full valuation report and loan-level details, click here.

Oakdale Mall

708,695 sf, Regional Mall, Johnson City, NY 13790

This property, which has outstanding debt of $47.5 million, has been with the special servicer since June 2018. Rialto acquired title to the property from Interstate Properties through a deed-in-lieu of foreclosure agreement in September 2020. The mall had been severely distressed pre-COVID when the mortgage loan had a below breakeven DSCR in 2018 and 2019. Positive developments for the mall came to fruition in recent weeks in the form of a 25-year payment-in-lieu-of-taxes (PILOT) program that would reduce real estate tax expense for the property from approximately $3.5 million to $449,000 for the next 5 years before scaling back up to $1.1 million in year 25. The PILOT agreement is in conjunction with a potential sale to Spark JC LLC, a local developer that acquired the vacant Sears portion of the mall in 2019. SPARK JC LLC plans to convert the former Sears box into a hospital and social services center.

The development firm also reportedly negotiated a $6.5 million settlement with Rialto for a tax lawsuit and is finalizing the acquisition of the property for approximately $8.5 million ($12/sf). In total, the redevelopment project is estimated to cost $116.0 million with plans convert the Oakdale Mall into a diversified mixed-use project named Oakdale Commons. For additional details, full valuation report, and loan-level details, click here.

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. For full access to our loan database and valuation platform, sign up for a free trial below: