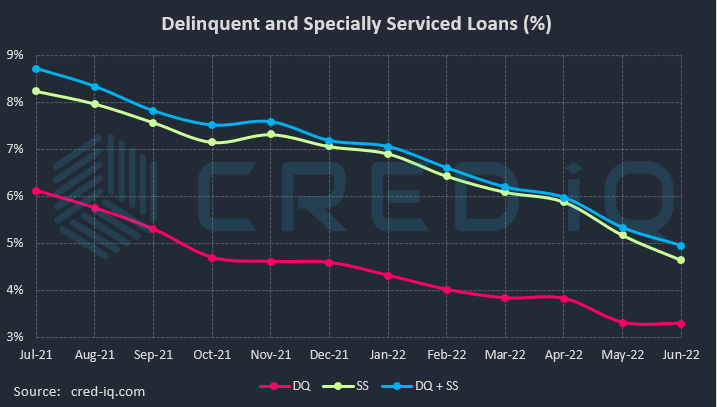

SS = All specially serviced CMBS loans in the conduit and SASB universe, including current, delinquent and REO

DQ + SS = All distressed CMBS loans in the conduit and SASB universe that are delinquent, specially serviced, or a combination of both

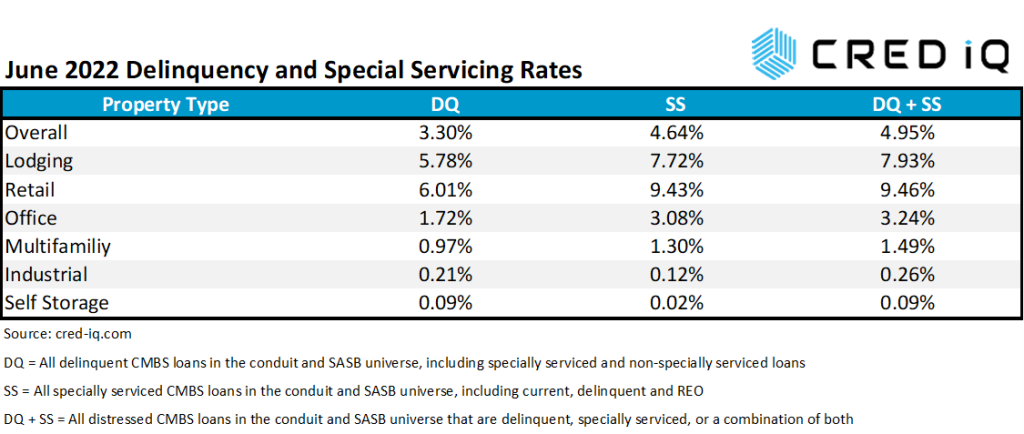

The CRED iQ delinquency rate for CMBS declined modestly during the June 2022 remittance period. Overall delinquency has declined consecutively in each month since June 2020. This month, the delinquency rate, equal to the percentage of all delinquent specially serviced loans and delinquent non-specially serviced loans, for CRED iQ’s sample universe of $500+ billion in CMBS conduit and single asset single-borrower (SASB) loans was 3.30%, which compares to last month’s rate of 3.32%. CRED iQ’s special servicing rate, equal to the percentage of CMBS loans that are with the special servicer (delinquent and non-delinquent), declined month-over month to 4.64% from 5.17%. The CMBS special servicing rate has declined for seven consecutive months. Aggregating the two indicators of distress – delinquency rate and special servicing rate – into an overall distressed rate (DQ + SS%) equals 4.95% of CMBS loans that are specially serviced, delinquent, or a combination of both. The overall distressed rate declined compared to the prior month rate of 5.33%. These distressed rates typically track slightly higher than special servicing rates as most delinquent loans are also with the special servicer.

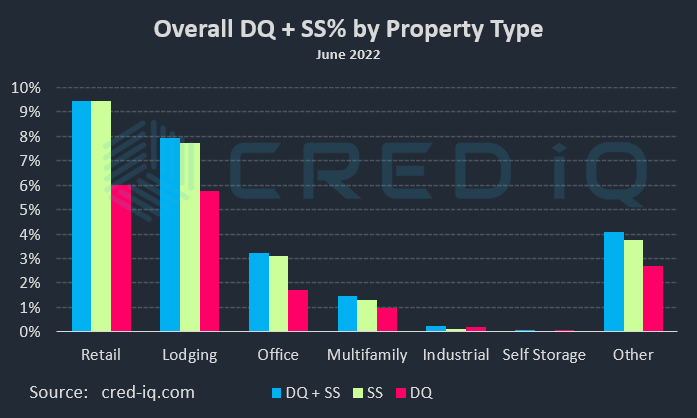

SS = All specially serviced CMBS loans in the conduit and SASB universe, including current, delinquent and REO

DQ + SS = All distressed CMBS loans in the conduit and SASB universe that are delinquent, specially serviced, or a combination of both

By property type, the delinquency rate increased in June for the office and industrial sectors. The delinquency rate for loans secured by office properties was 1.72% as of June 2022, which was an increase compared to 1.60% in the previous month. However, office delinquency is still down by approximately 47 bps from a year ago. A major contributor to the increase in office delinquency was the $231 million 260 and 261 Madison loan, which failed to pay off at maturity on June 11, 2022. According to a March 2022 Commercial Observer article, The Sapir Organization as loan sponsor was marketing the 923,277-sf office property for sale, although updated servicer commentary indicates a refinance is also being considered.

Delinquency rates declined in June 2022 for the retail, lodging and self-storage sectors. Retail continued to have the highest delinquency rate (6.01%) by property type for the third consecutive month after eclipsing the lodging sector in April 2022. Similar to the prior month, there were new high-profile retail delinquencies this month, including an $85.2 million loan secured by the Crossroads Center regional mall in Saint Cloud, MN. The loan became 30 days delinquent in June 2022 but has been in special servicing since October 2020.

Special servicing rates declined across all major property types this month. The lodging sector, which had a special servicing rate of 7.72%, exhibited the greatest month-over-month improvement among all property types. One of the more notable drivers behind the decline in the special servicing rate for lodging loans was the $325 million Hyatt Regency New Orleans. The loan transferred to special servicing in July 2020 due to pandemic-related disruptions to operations but returned to the master servicer on May 17, 2022 after a March 2022 loan modification.

The retail sector had the highest special servicing rate (9.43%), weighted by relatively large mortgages secured by regional malls. In one of this month’s latest developments, the $210 million Eastview Mall and Commons loan transferred to special servicing on June 1, 2022. The borrower cited ongoing issues related to the pandemic; however, the loan also has an impending September 2022 maturity date in an unfavorable refinancing environment.

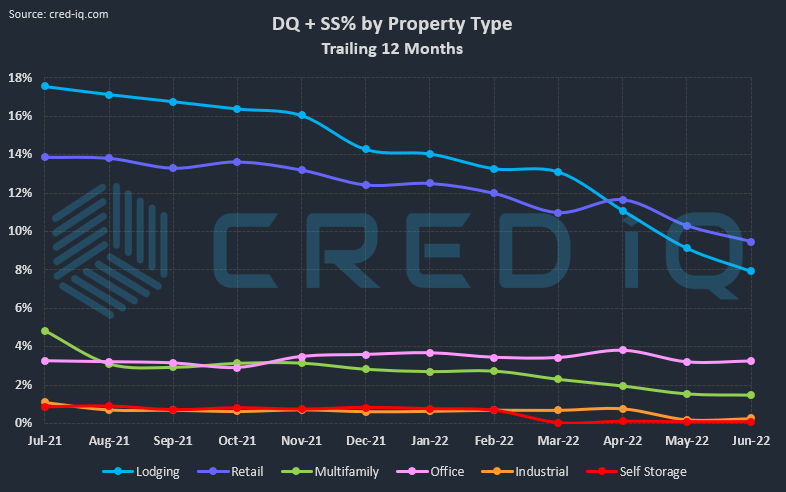

CRED iQ’s CMBS distressed rate (DQ + SS%) by property type accounts for loans that qualify for either delinquent or special servicing subsets. This month, overall distressed rates for all property types declined, except for office and industrial. Two of the largest loans added to the distressed category this month were 260 and 261 Madison Avenue, which failed to pay off at maturity, and Eastview Mall and Commons, which transferred to special servicing. For additional information about these two loans, click View Details below:

| [View Details] | [View Details] | |

| Loan | 260 and 261 Madison Avenue | Eastview Mall and Commons |

| Balance | $231,000,000 | $210,000,000 |

| Special Servicer Transfer Date | – | 6/1/2022 |

About CRED iQ

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. Our data platform is powered by over $2.0 trillion of CMBS, CRE CLO, SBLL, and GSE Agency loan and property data.