")

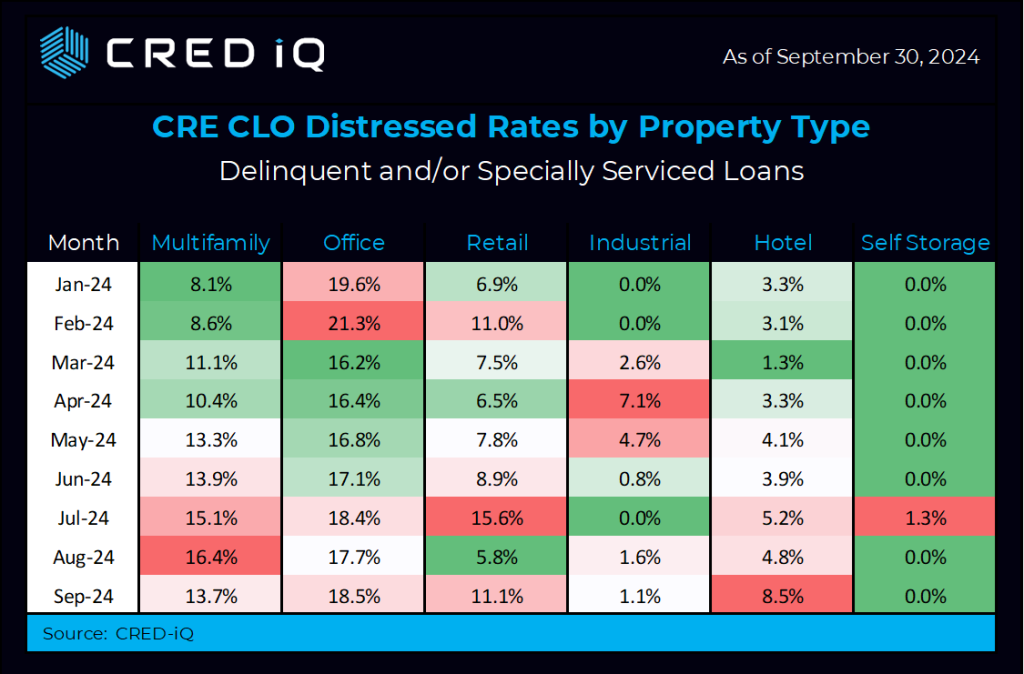

The CRED iQ research team dove into the CRE CLO ecosystem this week. We were interested in how the markets have evolved since our July report. The CRED iQ Distress rate reached 13.07% at the close of Q3, notching a whopping 277 basis point increase from last quarter’s close — setting a new record for the CRE CLO category.

The CRED iQ distress rate includes any loan reported 30 days delinquent, past their maturity, specially serviced, or a combination of these. We also examined the most recent property-level net operating income figures and compared them to underwritten expectations.

Given the rapid surge in interest rates, these floating-rate loans have shown significant declines in debt-service-coverage-ratios (DSCR). Approximately 53.9% of the properties within the distressed CRE CLO sector have reported a lower DSCR (NCF) compared to their underwritten DSCR. These numbers are based on the underwritten “as is” DSCRs and NOI. CRED iQ’s analysis uncovers that 62.3% of all distressed CRE CLOs are operating below a 1.00 DSCR.

Removing the interest rate variable, CRED iQ data uncovered that 41.8% of all CRE CLO distressed loans perform below their underwritten net operating income levels. Net operating income is a key variable in calculating a loan’s DSCR which determines the strength and creditworthiness of a given loan.

From a segment perspective, office leads in destress, logging an 18.5% distress rate, compared to 17.1% at the close of Q2. With that said, the office sector is off it’s 2024 high of 21.3% in February.

Multifamily saw a 13.7% distress rate, or flat to Q2. The segment spent most of the quarter at elevated levels as high as 16.4% in August, before seeing a 270-basis point reduction in the September print.

Retail (11.1%) and Hotel (8.5%) round out the top four. Self-storage scored another 0% distress score and Industrial at 1.1% –operating at these levels across nearly every investment category.

Showing upward trending, hotels saw a 460-basis point increase during Q3, followed by retail which logged a 220 basis point increase.

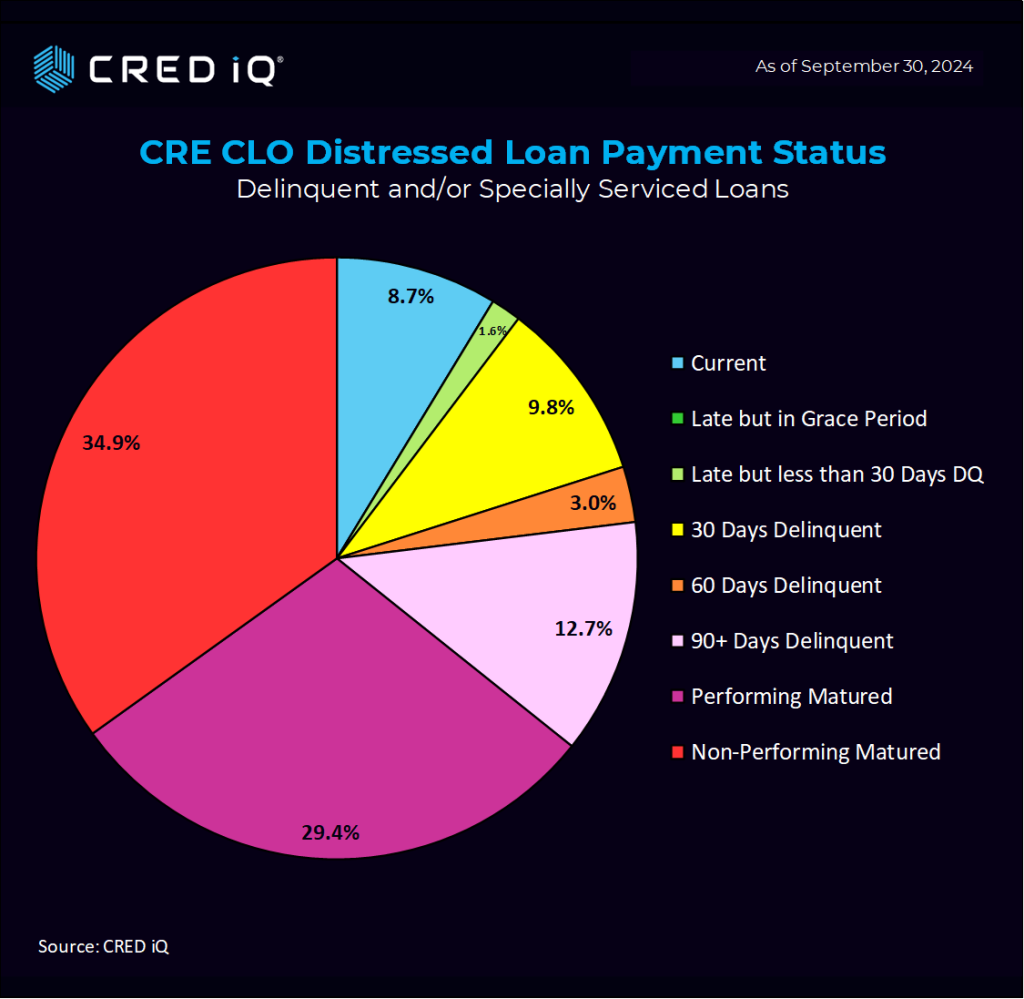

Looking across payment status, 29.4% of loans are performing matured, with another 34.9% non-performing matured, meaning 64.3% of the CRE CLO loans in our study are past their maturity dates.

Analysis Scope & Methodology

CRED iQ consolidated all of the loan-level performance data for every outstanding CRE CLO loan to measure the underlying risks associated with these transitional assets. Our team examined $72.4 billion in active CRE CLO loans. Many of these loans were originated in 2021 at times where cap rates were low, valuations high, low interest rates, and are starting to run into maturity issues given the spike in rates.

Some of the largest issuers of CRE CLO debt over the past five years include MF1, Arbor, LoanCore, Benefit Street Partners, Bridge Investment Group, FS Rialto, and TPG.The vast majority of the $79.1 billion in CRE CLO loans are structured with floating rates with 3-year loan terms equipped with loan extension options if certain financial hurdles are met.

About CRED iQ

CRED iQ is a market data provider that offers a robust suite of data and software solutions tailored for commercial real estate and finance professionals.

With over $2.3 trillion of CRE loans, CRED iQ delivers instant access to a comprehensive range of financial data and analytics for millions of properties in every market. CRED iQ’s data and analytical capabilities are instrumental in helping investors, lenders and brokers make informed and strategic decisions critical to their business.