Analysis of CRED iQ loan-level data reveals maturity extensions now account for the largest share of CMBS modification balance, with office collateral representing nearly two-thirds of all extension activity.

Modification Landscape: Maturity Extensions Take Center Stage

CRED iQ’s proprietary loan analytics platform tracks modification activity across the CMBS universe, capturing more than 7,800 individual loan modification events since 2019. Within that dataset, maturity date extensions have emerged as the dominant workout structure by outstanding loan balance. Of the 1,249 loans that received maturity extensions, the aggregate unpaid principal balance totals approximately $115.0 billion — reflecting the depth of refinancing stress concentrated in the legacy office sector and, increasingly, other property types navigating a prolonged high-rate environment.

Forbearance agreements account for the second-largest cohort by loan count at 1,445 loans ($38.7 billion), followed by combination modifications at 890 loans ($63.0 billion). Principal write-offs remain a relatively rare outcome, with only four recorded events totaling $155 million, underscoring that lenders and servicers continue to lean on time-based extensions over loss crystallization.

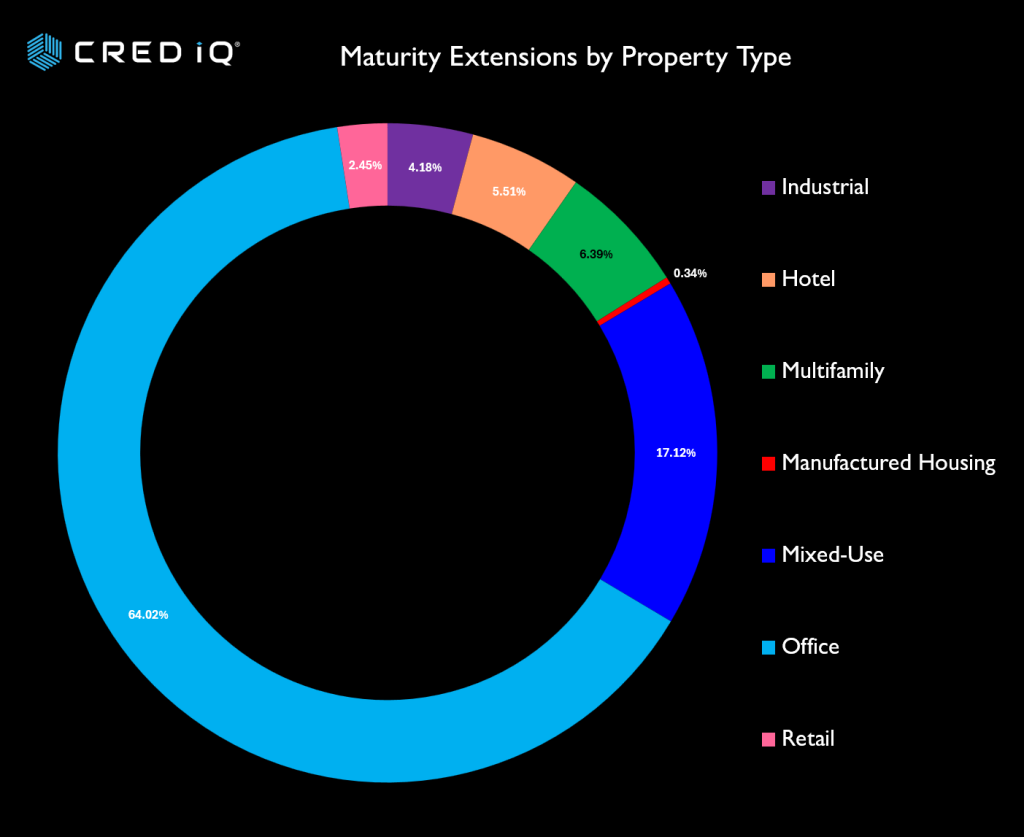

Property Type Allocation: Office Dominates Extension Activity

Among the 1,249 maturity extensions tracked by CRED iQ, office collateral accounts for 452 loans and $66.7 billion of the $104.3 billion in property-type-identified extension balance — representing 64.0% of total extension volume. Mixed-use properties rank second at 17.1% ($17.9 billion), followed by multifamily at 6.4% ($6.7 billion) and hotel at 5.5% ($5.7 billion). Industrial and retail trail at 4.2% and 2.4%, respectively.

The outsized office concentration reflects the structural headwinds facing the sector: post-pandemic occupancy erosion, elevated capital expenditure requirements, and an inability to refinance at maturity as values have declined sharply from origination-era appraisals. Extensions are being used as a bridge mechanism while borrowers and servicers negotiate long-term resolutions.

| Property Type | Loans | Balance | % of Balance |

| Office | 452 | $66.7B | 64.0% |

| Mixed-Use | 139 | $17.9B | 17.1% |

| Multifamily | 175 | $6.7B | 6.4% |

| Hotel | 87 | $5.7B | 5.5% |

| Industrial | 64 | $4.4B | 4.2% |

| Retail | 38 | $2.6B | 2.4% |

| Manufactured Housing | 14 | $354M | 0.3% |

Source: CRED iQ

Loan-Level Spotlight: Federal Center Plaza, Washington DC

A representative example of the maturity extension dynamic is Federal Center Plaza, a 725,317-square-foot office complex at 400 & 500 C Street SW in Washington, DC. The $130 million interest-only loan was securitized in COMM 2013-CCRE6 and originally matured on February 6, 2025. Unable to pay off at maturity, the loan was transferred to special servicing on November 15, 2024, and received a formal maturity date extension executed on February 4, 2026.

The property’s financial profile illustrates the broader challenges confronting DC office: physical occupancy has declined from 74% in 2023–2024 to 68% as of the trailing nine-month period ending September 2025. More critically, CRED iQ’s most recent appraised value stands at $168 million — a 45.6% reduction from the $309 million valuation at loan contribution in 2013. Despite the value impairment, the loan continues to carry a DSCR of 2.23x on a most-recent NOI basis, supported by the General Services Administration’s anchor lease covering 465,839 square feet. However, that GSA lease expires in August 2027, creating a concentrated rollover risk that will likely define the asset’s resolution trajectory. The loan’s expected resolution date is April 30, 2026.

| Loan Detail: Federal Center Plaza | |

| Deal / Loan ID | COMM 2013-CCRE6 / Loan 1 |

| Property | Federal Center Plaza, Washington DC |

| Property Type | Office (725,317 SF) |

| Current Balance | $130,000,000 |

| Original Maturity | February 6, 2025 |

| Modification Executed | February 4, 2026 |

| Modification Type | Maturity Date Extension |

| Appraised Value (2013) | $309,000,000 |

| Appraised Value (Jan 2026) | $168,000,000 (−45.6%) |

| Physical Occupancy | 68% (TTM Sept 2025) |

| DSCR (NOI) | 2.23x (most recent) |

| Largest Tenant | GSA — 465,839 SF (Lease Exp. Aug 2027) |

| Special Servicer Transfer | November 15, 2024 |

| Expected Resolution | April 30, 2026 |

Source: CRED iQ

About CRED iQ

CRED iQ is a leading commercial real estate (CRE) data and analytics platform designed to bring transparency, structure, and actionable intelligence to complex CRE debt markets. The platform aggregates and normalizes loan- and property-level data across CMBS, CRE CLO, Agency, and private debt, enabling investors, lenders, servicers, and advisors to analyze risk, performance, and opportunities within a single, unified environment.

CRED iQ specializes in advanced analytics for loan surveillance, distress tracking, special servicing activity, and workout strategies, with a particular focus on identifying early warning signals and resolution outcomes across the CRE lifecycle. By combining institutional-grade data infrastructure with AI-driven insights, CRED iQ helps market participants move beyond static reporting toward dynamic, forward-looking decision-making.

Users leverage CRED iQ to monitor delinquency trends, track foreclosures and REO pipelines, evaluate modification and extension activity, and assess portfolio exposure at the property, sponsor, and market level. The platform is built for speed, scalability, and precision—reducing manual research while increasing confidence in investment, underwriting, and asset management decisions.

Trusted by leading institutional investors, lenders, and advisory firms, CRED iQ delivers the data foundation required to navigate today’s evolving CRE market. For professionals seeking a comprehensive commercial real estate analytics platform with deep coverage of distressed debt, special servicing, and AI-powered insights, CRED iQ provides a differentiated, execution-ready solution.