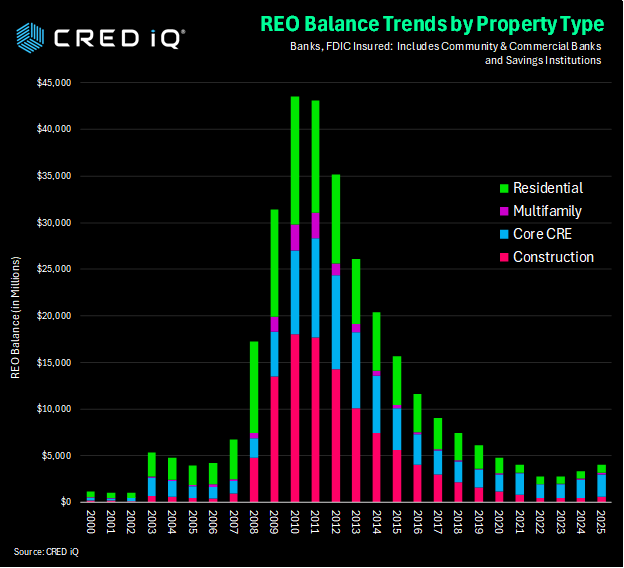

Today’s Q2 2025 REO (real estate owned) balances across property sectors are substantially lower than the peaks witnessed during the great financial crisis of 2008-2012, signaling a more resilient CRE environment and improved asset quality for lenders and investors. As a reminder, REO assets refers to properties (such as office buildings, retail spaces, industrial facilities, or multifamily units) that have been foreclosed upon by a lender—typically a bank or financial institution—and are now directly owned by that lender after an unsuccessful foreclosure auction or when the borrower defaults on their loan.

Q2 2025 vs. GFC REO Levels

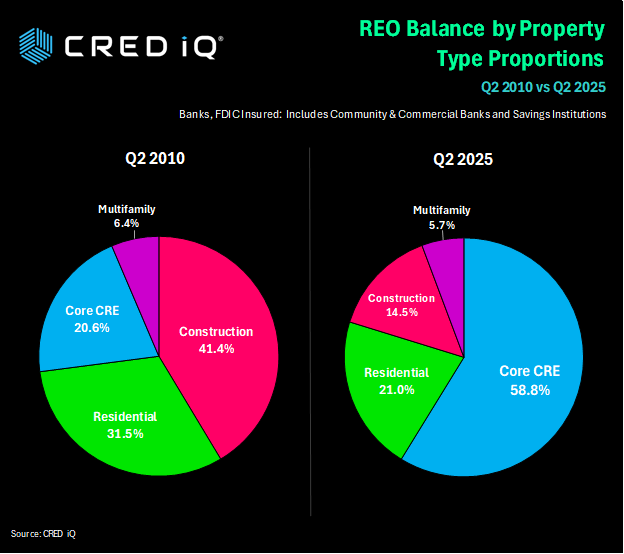

REO balances reached extraordinary heights between 2008 and 2012, with total real estate owned surging up to over $51 billion in Q2 2011. Each major property type saw dramatic increases: nonfarm nonresidential peaked above $17 billion, with multifamily, construction, and residential sectors all seeing multi-billion dollar REO volumes. By comparison, Q2 2025 shows markedly lower balances: total REO is about $4.1 billion, with core CRE (nonfarm nonresidential) at $2.4 billion, construction at $588 million, and multifamily at $231 million.

Sector Breakdown and Trends

Core CRE: After cresting above $17 billion in Q2 2011, this sector now holds only $2.38 billion of REO, showing how far distress has receded.

Construction: The current $588 million in construction REO is a fraction of the GFC peak of over $18 billion, as riskier development loans have been managed more conservatively in recent cycles.

Multifamily and Residential: Multifamily REO hit over $2.7 billion during crisis years but sits at $231 million in 2025. 1-4 Unit Residential peaked above $13 billion in 2010, now just $852 million, reflecting more robust borrower performance and tighter underwriting.

Office Example

A four-story, 137,731-square-foot office building at 120 Mountain View Blvd in Basking Ridge, NJ, entered foreclosure after a failed balloon payment upon loan maturity in June 2024, resulting in REO status. Originally valued at $27.2 million in 2014, the property’s value plummeted to $7.7 million by mid-2025 as its occupancy dropped from 100% in 2022 to just 45.64% in March 2025, contributing to a low DSCR of 0.46 as of May 2025. With amenities like a cafeteria and garage, the asset’s financial distress led to the appointment of a receiver and foreclosure proceedings as the lender moved to resolve the non-performing matured loan transferred from the JPMBB 2014-C22 conduit

Macro Implications for Investors and Lenders

REO levels are now in line with—or lower than—pre-GFC averages, confirming that lenders are carrying far fewer distressed real estate assets on their books than before. This shrinkage reflects not only the economic growth following the crisis, but also dramatic improvements in risk management, property valuation, and loan workout strategies that have reduced the systemic build-up of troubled assets.

Opportunity and Risk Outlook

While lower REO supply suggests fewer forced-sale buying opportunities for opportunistic investors, it also signals healthier loan books for lenders and higher confidence in collateral values. Should economic headwinds intensify, early detection and workout mechanisms in today’s market will likely prevent a repeat of GFC-level asset distress, offering greater stability for commercial real estate stakeholders.

Overall, today’s REO environment tells a story of cautious optimism, where lessons from the GFC have reduced risks and left both lenders and investors better positioned to weather future shocks.

About CRED iQ

CRED iQ is a market data provider that offers a robust suite of data and software solutions tailored for commercial real estate and finance professionals.

With over $2.3 trillion of CRE loans, CRED iQ delivers instant access to a comprehensive range of financial data and analytics for millions of properties in every market. CRED iQ’s data and analytical capabilities are instrumental in helping investors, lenders and brokers make informed and strategic decisions critical to their business.

THE DATA, INFORMATION AND/OR RELATED MATERAL (“DELIVERABLES”) IS BEING OFFERED AS-IS/WHERE-AS CONDITION. CRED-IQ MAKES NO REPRESENTATION OR WARRANTY AS TO QUALITY OR ACCURACY OF SUCH DELIVERABLES BEING PURCHASED, WHETHER EXPRESS OR IMPLIED, EITHER IN FACT OR BY OPERATION OF LAW, STATUTE, OR OTHERWISE, AND CRED-IQ SPECIFICALLY DISCLAIMS ANY AND ALL IMPLIED OR STATUTORY WARRANTIES INCLUDING WARRANTIES OF MERCHANTABILITY AND OF FITNESS FOR A PARTICULAR PURPOSE, TECHNICAL PERFORMANCE, AND NON-INFRINGEMENT. WITHOUT LIMITING THE FOREGOING, YOU AS CUSTOMER ACKNOWLEDGE THAT YOU HAVE NOT AND ARE NOT RELYING UPON ANY IMPLIED WARRANTY OF MERCHANTABILITY OR OF FITNESS FOR A PARTICULAR PURPOSE OR OTHERWISE, OR UPON ANY REPRESENTATION OR WARRANTY WHATSOEVER AS TO THE DELIVERABLES IN ANY REGARDS WHATSOEVER, AND ACKNOWLEDGE THAT CRED-IQ MAKES NO, AND HEREBY DISCLAIMS ANY, REPRESENTATION, WARRANTY OR GUARANTEE THAT THE PURCHASE, USE OR COMMERCIALIZATION OF ANY DELIVERABLES WILL BE USEFUL TO YOU OR FREE FROM INTERFERENCE. BY ACCEPTANCE OF THE DELIVERABLES, YOU HEREBY RELEASE CRED-IQ AND ITS AFFILIATES AND AGENTS FROM ALL CLAIMS, DAMAGES AND LIABILITY ARISING HEREUNDER.