Following on the heels of well publicized troubles in the office sector, increasing attention has been paid as of late to potential distress within the multifamily sector. Recent headlines have pointed to staggering change rates in distress for a previously obscure financial product, the CRE CLO securitization, which generally consists of floating rate bridge loans leveraging transitional properties. In plain language terms, they encumber riskier properties undergoing some form of a value-add sponsor business plan. Most of the general issues are already well known and have been discussed by market participants ad nausem so need not be repeated.

Issuers generally consist of private debt funds and listed commercial mortgage REITs. In that context, the CLO is effectively a fungible financing option; loans are originated and typically encumbered with repo leverage. Risk retention by the issuer generally falls in the 10-20% range. This is where the similarities end. CRE CLOs can be static or managed transactions; this distinction has notably produced disparate loss mitigation outcomes between two listed commercial mortgage REITs: Ready Capital (“Ready”) and Arbor Realty Trust. A fundamental misunderstanding of distinct structural loss mitigation levers has resulted in an erroneous assessment of near term outcomes and latency of any potential adverse credit events.

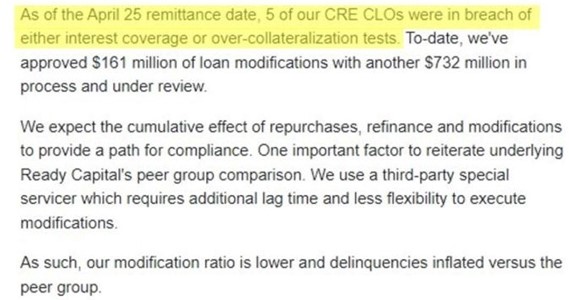

BofA Securitized Products Strategy team indicated in a CRE CLO memo dated May 8, 2024 as follows “Seven deals failed their IC/OC tests in April, which is five more than the two that failed in March. Deals from the RCMT shelf accounted for six of the seven deals that failed its IC or Par Value test.” Ready then indicated the following morning in their May 9 earnings call that as of the April 25 remittance date only five of their CRE CLOs were in breach of interest coverage or overcollateralization tests. I have been unable to reconcile this apparent discrepancy. Regardless, the catalyst for continuing distress in the Ready CLO book seems to be the static nature of their issuances. See below screenshot from Ready’s May 9 earnings call transcript.

In an actively managed CRE CLO, the collateral manager typically has discretion to buy and sell loans so as to minimize losses for pool investors. In effect, even though on a loan level basis the assets within the pool are likely below investment grade, through active management the credit quality of the issuance as a whole can in theory be improved over time. In contrast, Ready has stated on its recent earnings call that it has been hamstrung in loss mitigation efforts by a static CLO structure and that it needs a third party special servicer to affirm any modification requests as compliant with the servicing standard prior to modifications within CLO vehicles. I have had conversations with multiple insiders over the last several months who have indicated to me, in effect, that it is best practice for a collateral manager to avoid modifications within the structure as much as is reasonably practicable.

A CRE CLO SPV is an offshore tax entity not generally subject to US tax on net income. Modifications performed within the structure that are deemed “economically significant” (rate, term, recourse, lien subordination, cross collaterization etc) can be deemed a re-origination and engaging in US Trade or Business (SeeIRS Private Letter Ruling 9701006), which would in turn subject net income to US tax. Ready is in effect apprently hamstrung in modifying loans outside of the SPV and lacks the similar discretion to reinvest seasoned modified loans in CLOs relative to peers.

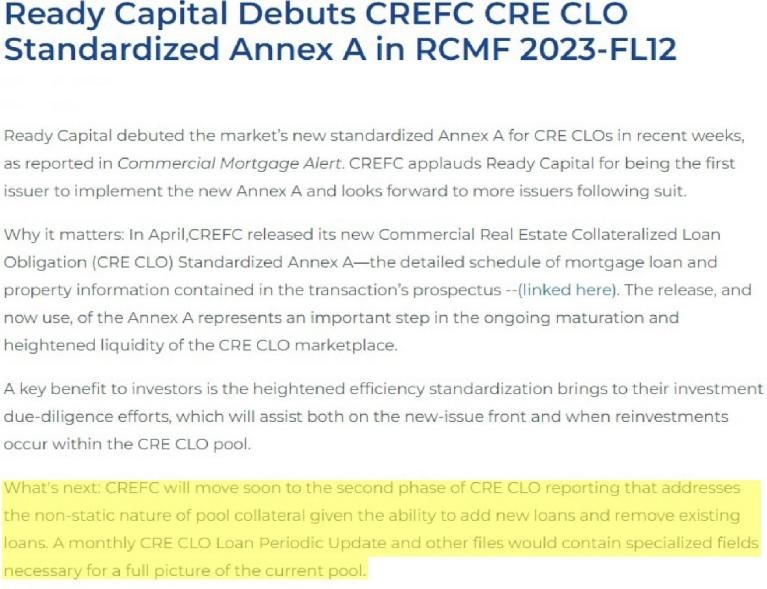

Ready rolled out its 12th CRE CLO, RCMF 2023–FL12, last June to some fanfare as it was the first issuance implementing the new CREFC Annex A data standard.

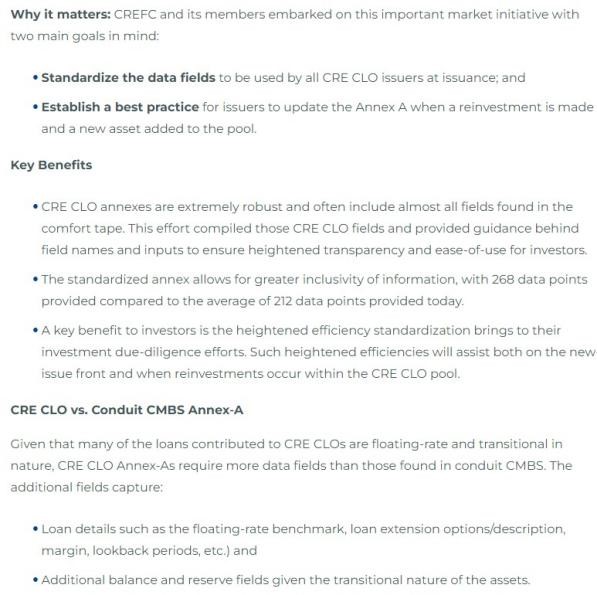

Notably, the second phase highlighted above has lagged in implementation across the board since CREFC press releases last spring. The new standard is particularly important at this moment in time for actively managed CLO issuances as the underlying loans are exchanged and/or modified and seasoned loans are reinvested. Having identified this need, the team at Cred IQ is currently working through generating a proprietary cohort of CRE CLO annexes which seek to normalize outstanding issuances to the new Annex A standard inclusive of relevant data fields.

Back to Ready’s twelfth issuance (noted above) which is the first to adhere to the new CREFC standard, inexplicably and consistent with Ready’s prior issuances, it is once again a statically managed CLO. There is a particular tinge of irony in this as Waterfall Asset Management is the external advisor to the publicly traded Ready Capital entity; Waterfall was a substantial player in the residential NPL market from 2009 onwards and their team has extensive loss mitigation and workout experience.

The extent of Arbor Realty Trust’s modifications is well known; the purpose of this article is not to debate the validity or terms of those modifications, as their existence is undeniable. Credit enhancement or lack thereof of Arbor CLO vehicles from reinvestments is likewise the subject of another article in which I intend to incorporate the new CRED iQ normalized reporting standard to discuss identifying potential preferred equity opportunities in the ARCREN actively managed shelf. That said, there an inherent latency to credit events for an actively managed CRE CLO relative to a static CRE CLO. To gripe and claim an active collateral manager is “extending and pretending” is simply demonstrative of lack of understanding of the structural levers in my view; it is not a bug but rather a feature.

Where now? The distressed debt opportunity from static CRE CLOs

Ready and affiliates have been particularly active over the years as loan sellers. Tellingly, Ready has specifically stated that it has $655 million in loans now marked as held for sale, of which approximately 40% are from its M&A bucket, namely acquisitions of Broadmark Realty Capital and Mosaic Real Estate Credit. Arbor, in comparison, has not proven to be a frequent loan seller. As alluded to, a potential Arbor opportunity set in the next several quarters may very well be pref equity of the soft variety behind an agency senior with recognition rights.

As to the situation at hand, of Ready’s $655 million of loans marked for sale approximately 70% are in some stage of delinquency. There is a certain value in tracking potential distress in advance of an anticipated loan sale; secondary market NPL sales typically occur relatively quickly and lack the prolonged due diligence periods characteristic of typical CRE investment sales. In addition, understanding the inherent changes that occur to a distressed asset over time assists with accurate loan level NPL underwriting and bid commentary to loan sellers. This is even more important when targeting a specific distressed loan acquisition which has not yet been offered on the secondary market. Additionally, nonperforming loan backleverage has also become increasingly interesting. Loan to acquisition cost varies widely but is typically in the 60% range +/- 10%. Terms range from SOFR +400 for a relatively low leverage note on note product to prime +200 with a 10.5% rate floor for note buyers seeking 75% leverage. Origination fees are typically one to two points for a two year term with extension option. NPL backleverage provides high yield at a relatively low LTV ratio against the underlying collateral with upside in the optionality to take over the workout process in the event of default.

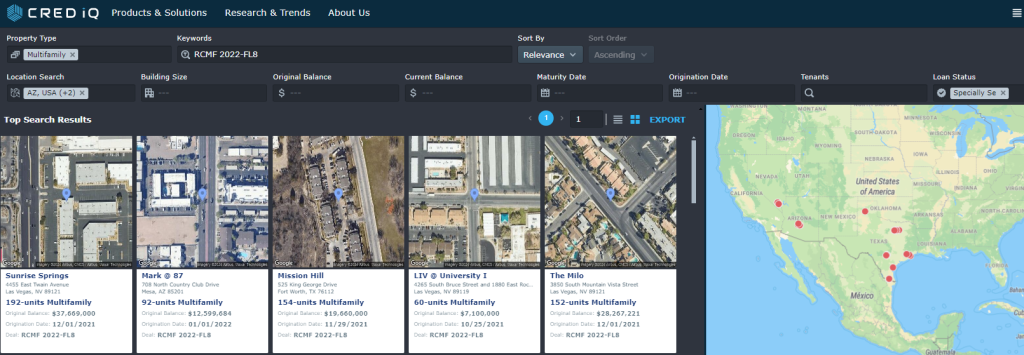

For purposes of a sample use case of CRED iQ data to source such opportunities, let’s take a look at an issuance from the Ready shelf, 2022-FL8. In a surveillance update dated September 21, 2023, DBRS notes: Five loans, representing 14.6% of the current trust balance, encumber properties for which Tides Equities is the sponsor.

CRED iQ has provided me a draft of their soon to be released normalized Annex A cohort specific to the RCMT FL8 issuance which I have cropped in pertinent part:

The five loans issued to Tides Equities within this pool encumber the following properties: 4620 W McDowell Rd, Phoenix AZ (“Tides on McDowell”), 2645 E Cactus Rd, Phoenix AZ (“Tides on East Cactus”), 4455 E Twain Ave, Las Vegas, NV (“Tides on Twain”), 3850 S Mountain Vista St, Las Vegas, NV (“Tides on Indios”), and 525 King George Dr, Fort Worth, TX (“Tides on Meadowbrook”). Utilizing the data from the Cred IQ normalized RCMT 2022-FL8 annex, we can then find loan level distress for Tides Equities properties using the platform’s property analytics interface. Tides properties in are multifamily in AZ, TX and NV so I limited my search accordingly.

Based upon the limitations of static CLO loss mitigation as described in the Ready Capital earnings call, I then filtered results to those loans specially serviced or 60 days+ delinquent. Please note that some of these properties have changed hands several times in recent years and the apartment complex name from the prior sponsor may still be reflected in results. However, based upon the property addresses, I can determine that Tides on Twain, Tides on Meadowbrook and Tides on Indios are either specially serviced or more than 60 days delinquent.

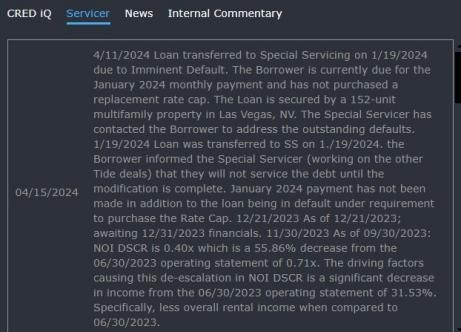

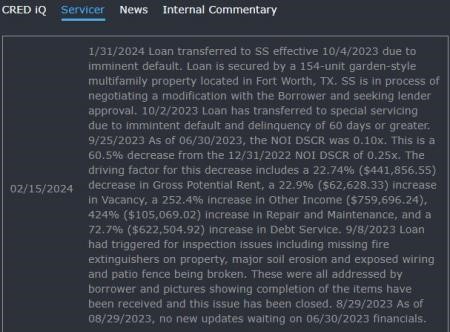

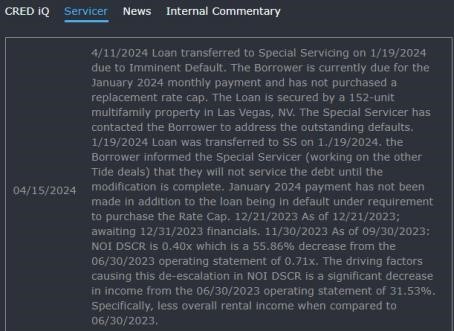

Below are the special servicer’s most recent notes from the CRED iQ platform for Tides on Twain, Tides on Meadowbrook, and Tides on Indios, respectively:

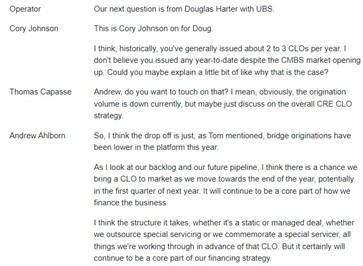

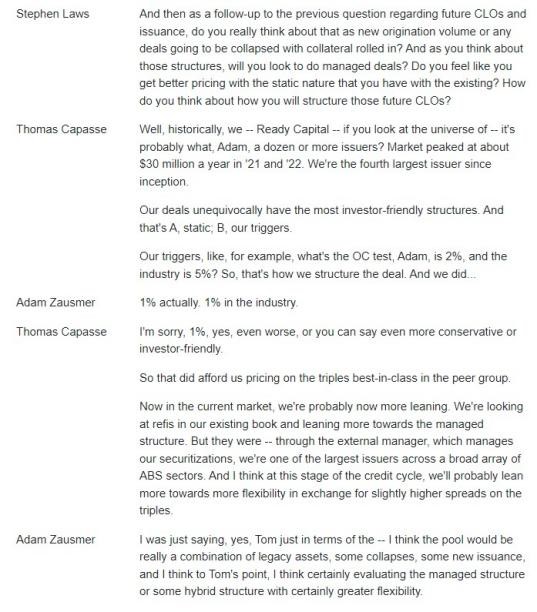

These particular Tides properties are encumbered by just some of the many troubled multifamily bridge loans that have recently entered the loss mitigation process. To gain further insight NPL sales and note on note backleverage out of Ready’s static CLO structures, below are several relevant exchanges from Ready’s earnings call:

Ready has expressed interest in bringing a new CLO to market by the end of 2024, tellingly of the actively managed variety. This is particularly relevant; assuming the market still has an appetite for new issue CRE CLOs it reflects a present opportunity for sourcing distress out current static CLO structures using CRED iQ analytics.

About the Author

Jordan Cailliarec

Jordan Cailliarec is a career distressed debt and special situations investor. After attending law school, he spent six years in the nonperforming loan space in the aftermath of the GFC including a stint managing the judicial state portfolio for a PE backed residential distressed debt platform. Subsequently, he has managed an UHNWI’s opportunistic real estate investments with a focus on lower middle market credit related positions and creative restructurings. In addition, he acquired and managed the disposition of a residential whole NPL portfolio sourced from a housing nonprofit in 2021. Disclosure: Jordan holds a long position in Arbor Realty Trust common stock. You can follow him on LinkedIn or reach him by email.