This week, CRED iQ reviewed the commercial real estate lending landscape and highlighted five properties that secured financing in May and June 2022. In certain cases, financing packages from previous mortgage commitments were catalogued in CRED iQ’s database, which enables users to evaluate prior loan terms and pre-origination financial history. The highlighted loan originations feature five different property types — mixed-use, office, retail, industrial and self-storage. The largest featured commercial mortgage is secured by a mixed-use property located in the San Francisco MSA.

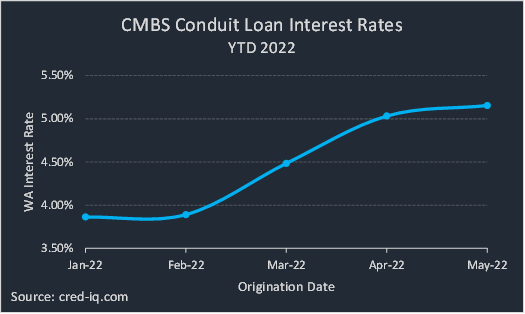

Using the CRED iQ platform’s Comps functionality, which features propriety Comps scoring for the CRE loan universe, we compared lending terms and loan structures to get a sense of the trends in the CRE lending environment. CRED iQ recently examined rising interest rates for CMBS conduit loans in a report published last week, comparing new originations in 2022 across several property types.

CRED iQ additionally provided valuations for each asset to evaluate leverage levels in relation to originators’ LTVs. The CRED iQ valuations factor in base-case (most likely), downside (significant loss of tenants), and dark scenarios (100% vacant). Base-case valuations for select properties are provided below. For access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

The Lion Building

172,328 sf, Mixed Use (Industrial/Office), San Francisco, CA

A $100 million loan was originated by Deutsche Bank on June 8, 2022 to pay off $48 million of existing debt on The Lion Building, a 172,328-sf mixed-use property in San Francisco, CA. Financing from the mortgage was also used to fund $50.7 million in reserves. With more than 50% of the loan balance earmarked for reserves, the loan has a distinctive composition of sources and uses relative to other comparable recent originations. There is a $31 million earnout reserve tied to the smaller of the property’s two tenants, Embark Trucks (31% of NRA). Embark Trucks had not yet taken occupancy at origination and earnout will be completed when the tenant takes occupancy and starts paying rent, which is expected by August 2022. Other major reserve items were for tenant improvements and leasing commissions, free rent, and security deposits for the building’s two tenants.

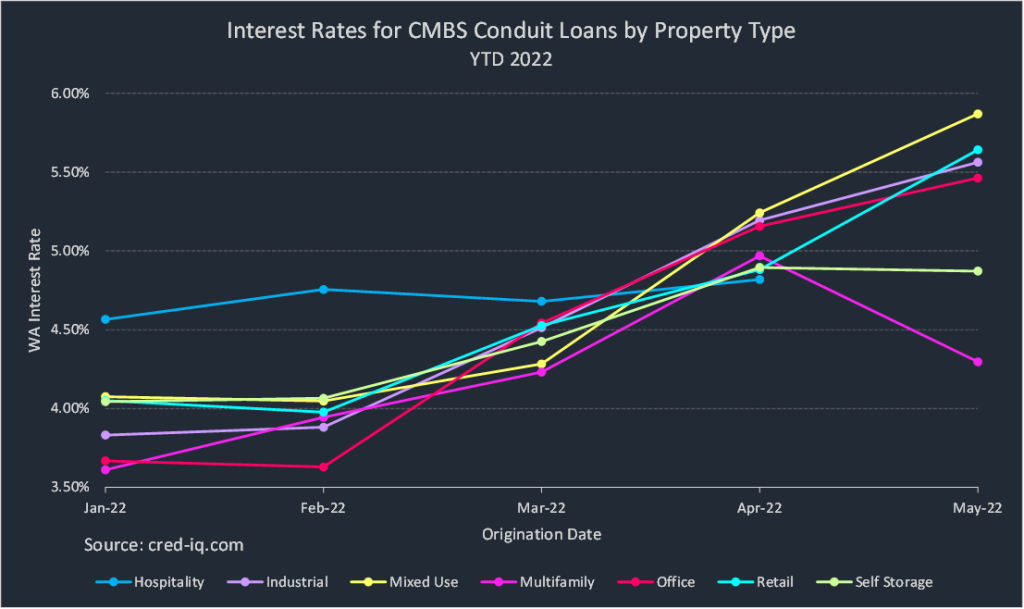

The interest-only loan had a 10-year term and was structured with an interest rate of 5.1975%. The interest rate was below the weighted average interest rate of 5.87% for CMBS conduit loans secured by mixed-use properties that were originated in May 2022. The loan will be locked out from prepayment for two years, and defeasance will be permitted after lockout through the remainder of the loan term until its open period, five months prior to maturity.

Using CRED iQ’s Comps functionality, one of the most comparable originations is a loan secured by a 49,946-sf flex building located at 555 De Haro Street. The loan had a balance of $19 million was originated in October 2017. The comparable loan’s interest rate was 4.31%, which is approximately 89 bps lower than the new origination for The Lion Building.

The Lion Building is a four-story mixed-use building located in the Potrero Hill submarket of San Francisco, CA. The property is primarily zoned for industrial use centered around production, design, and repair operations but the building has an allowance for pure office use up to approximately 25% of the NRA. The property is fully leased to two tenants, neither of which had taken full occupancy at loan origination. IDEO is a design and consulting firm that leases 69% of the property, although a portion of the leased space does not commence until 2023. Embark Trucks, a software company for autonomous driving, leases the remaining 31% of the property but is not expected to take physical occupancy until August 2022 at the earliest.

The property was appraised at a value of $170 million ($986/sf) as of March 30, 2022. The appraisal resulted in an LTV of 59% and an implied cap rate of 5.40% based on the originator’s underwritten net cash flow. The debt yield came in at 12.9%, also based on NCF from the originator’s underwriting. For the full valuation report and loan-level details, click here.

| Name | The Lion Building |

| Address | 2525 16th Street San Francisco, CA 94103 |

| Property Type | Mixed Use |

| Property Subtype | Industrial/Office |

| Property Size | 172,328 sf |

| Year Built | 1924 |

| Submarket | Potrero Hill |

| County | San Francisco |

| MSA | San Francisco-Oakland-Fremont, CA |

| Origination Date | 6/8/2022 |

| Loan Amount | $100,000,000 |

| Interest Rate | 5.20% |

| Debt Yield (UW NCF) | 12.9% |

| Valuation | |

| Appraised Value | $170,000,000 ($986/sf) |

| Appraisal Date | 3/30/2022 |

| Appraisal LTV | 59% |

| CRED iQ Base-Case Value | $159,300,000 ($924/sf) |

PentaCentre Office

734,156 sf, Office, Troy, MI

Citi funded a $34.3 million mortgage on June 2, 2022 for the acquisition of the PentaCentre Office complex in Troy, MI. The 10-year loan was structured with amortizing debt service payments based on a 30-year schedule. The interest rate for the mortgage was 5.32%, which compares to the May 2022 weighted average rate of 5.46% for CMBS conduit loans secured by office properties. Prepayment provisions for the loan include a two-year lockout period until defeasance is permitted. The prior financing package for PentaCentre Office, also funded by Citi, was a five-year $41.25 million mortgage that was originated in September 2017. The loan had an interest rate of 4.56%.

One of CRED iQ’s highest scoring loan comps is Troy Place, a $40 million loan that was originated in January 2019. The loan is secured by a 756,845-sf office complex located about two miles away from PentaCentre Office. The comparable loan had an interest rate of 5.09%, which was 23% lower than the new origination.

PentaCentre Office comprises four freestanding office buildings. The portfolio of properties was 62% occupied as of April 2022, which compares to 79% occupancy in 2021 and 77% occupancy in 2020. The property was appraised for $59.5 million ($81/sf) as of March 29, 2022, which resulted in an LTV of 58%. The originator’s underwritten NCF implied a cap rate of 6.68% and a debt yield of 11.6%. For the full valuation report and loan-level details, click here.

| Name | PentaCentre Office |

| Address | 300 – 340 East Big Beaver Road Troy, MI 48083 |

| Property Type | Office |

| Property Subtype | Suburban |

| Property Size | 734,156 sf |

| Year Built | 1986 |

| Submarket | Troy South |

| County | Oakland |

| MSA | Detroit-Warren-Livonia, MI |

| Origination Date | 6/2/2022 |

| Loan Amount | $34,300,000 |

| Interest Rate | 5.32% |

| Debt Yield (UW NCF) | 11.6% |

| Valuation | |

| Appraised Value | $59,500,000 ($81/sf) |

| Appraisal Date | 3/29/2022 |

| Appraisal LTV | 58% |

| CRED iQ Base-Case Value | $55,510,000 ($76/sf) |

Sawmill Plaza

194,694 sf, Retail, Columbus, OH

A $19.5 million loan was originated by LMF Commercial on May 10, 2022 to fund the acquisition of Sawmill Plaza, a 194,694-sf shopping center in Columbus, OH. The property was sold to a private investor group based out of New Jersey from its former California-based owners for $27.4 million, equal to $141/sf. The 10-year loan amortizes over a 30-year period and has an interest rate of 5.63%. The loan’s interest rate is in line with the weighted average interest rate for retail conduit loans originated in May 2022. The loan will be locked out from prepayment for about two years, and defeasance will be permitted after lockout through the remainder of the loan term until its open period, four months prior to maturity. The property was previously encumbered by $16.5 million in floating rate debt with a rate of 1-month LIBOR plus 3.85%.

Sawmill Plaza is located approximately 13 miles north of the Columbus, OH CBD and is anchored by Hobby Lobby. The anchor tenant accounts for 30% of the property’s NRA pursuant to a lease that expires in February 2024. Planet Fitness is the second-largest tenant, accounting for 15% of NRA, with a lease that expires in September 2028. The property was 96% occupied as of March 2022. The collateral was appraised for $28 million ($144/sf) on March 18, 2022, resulting in an LTV of 70%. The implied cap rate based on the originator’s underwritten NCF was 7.00% and the debt yield was equal to 10.1% based on the same metrics. For the full valuation report and loan-level details, click here.

| Name | Sawmill Plaza |

| Address | 2643 Sawmill Place Boulevard Columbus, OH 43235 |

| Property Type | Retail |

| Property Subtype | Anchored |

| Property Size | 194,691 sf |

| Year Built | 1987 |

| Submarket | Worthington |

| County | Delaware |

| MSA | Columbus, OH |

| Origination Date | 5/10/2022 |

| Loan Amount | $19,500,000 |

| Interest Rate | 5.63% |

| Debt Yield (UW NCF) | 10.1% |

| Valuation | |

| Appraised Value | $28,000,000 ($144/sf) |

| Appraisal Date | 3/18/2022 |

| Appraisal LTV | 70% |

| CRED iQ Base-Case Value | $25,240,000 ($130/sf) |

Valcour Industrial

490,000 sf, Industrial, St. Louis, MO

Bank of Montreal originated a $9.2 million loan on May 19, 2022 to refinance existing debt on a 490,000-sf industrial property in St. Louis, MO. After a five-year interest-only period, the 10-year loan will amortize based on a 30-year schedule. The interest rate for the loan is 5.55%, which was in line with the weighted average interest rate for conduit industrial loans originated in May 2022. The property’s previous mortgage had a similar structure but had an interest rate of 4.70%, which was 85 bps lower than the new origination.

The Valcour Industrial property is 100% occupied between two tenants. The larger tenant, Schroeder & Tremayne, has a lease expiration in December 2025. The smaller tenant, Miss Elaine, has a lease expiration in December 2024. The property was appraised for $13.1 million ($27/sf) as of January 25, 2022, which resulted in an LTV of 70% and an implied cap rate of 7.58% based on the originator’s underwritten net cash flow. The debt yield based on underwritten net cash flow came in at 10.8% For the full valuation report and loan-level details, click here.

| Name | Valcour Industrial |

| Address | 8500 Valcour Industrial St. Louis, MO 63123 |

| Property Type | Industrial |

| Property Subtype | Warehouse |

| Property Size | 490,000 sf |

| Year Built | 1961 |

| Submarket | South County |

| County | St. Louis |

| MSA | St. Louis, MO-IL |

| Origination Date | 5/19/2022 |

| Loan Amount | $19,500,000 |

| Interest Rate | 5.55% |

| Debt Yield (UW NCF) | 10.8% |

| Valuation | |

| Appraised Value | $13,100,000 ($27/sf) |

| Appraisal Date | 1/25/2022 |

| Appraisal LTV | 70% |

| CRED iQ Base-Case Value | $13,080,000 ($27/sf) |

Mini U Storage – Woodbridge

58,075 sf, Self-Storage, Woodbridge, VA

KeyBank originated a $5.6 million loan on June 7, 2022 to refinance existing debt on a self-storage property in Woodbridge, VA, located approximately 30 miles south of Washington, DC. The 10-year interest-only loan has an interest rate of 5.66%, which is significantly higher than the average for self-storage conduit loans originated year-to-date in 2022. The weighted average interest rate for self-storage loans in CMBS conduit securitizations was approximately 4.9% in April and May 2022. One of CRED iQ’s highest scoring comps was Dumfries Self Storage, which secured a $2.5 million loan. The loan was originated in October 2015 and had an interest rate of 4.43%.

Mini U Storage contains units ranging from 5’ x 5’ to 20’ x 25’. The property was appraised at a value of $10.65 million ($183/sf) as of May 4, 2022. The appraisal resulted in an LTV of 53%, and an implied cap rate of 4.88% based on the originator’s underwritten NCF. The debt yield came in at 9.2%, also based on NCF from the originator’s underwriting. For the full valuation report and loan-level details, click here.

| Name | Mini U Storage – Woodbridge |

| Address | 13901 Smoketown Road Woodbridge, VA 22192 |

| Property Type | Self Storage |

| Property Subtype | Self Storage |

| Property Size | 58,075 sf |

| Year Built | 1999 |

| Submarket | Manassas/Woodbridge |

| County | Prince William |

| MSA | Washington-Arlington-Alexandria, DC-VA-MD-WV |

| Origination Date | 6/7/2022 |

| Loan Amount | $5,625,000 |

| Interest Rate | 5.66% |

| Debt Yield (UW NCF) | 9.2% |

| Valuation | |

| Appraised Value | $10,650,000 ($183/sf) |

| Appraisal Date | 5/4/2022 |

| Appraisal LTV | 53% |

| CRED iQ Base-Case Value | $55,510,000 ($76/sf) |

For full access to our loan database and valuation platform, sign up for a free trial below:

About CRED iQ

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. Our data platform is powered by over $2.0 trillion of CMBS, CRE CLO, SBLL, Ginnie Mae, FHA/HUD, and Agency loan and property data.