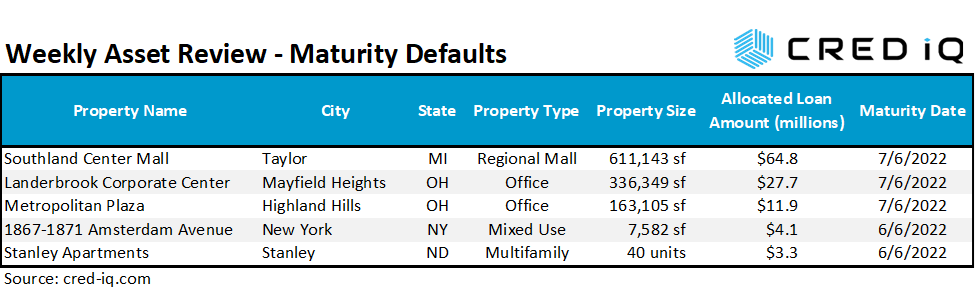

This week, CRED iQ reviewed valuations for several assets that secure non-performing matured loans. Maturity defaults often can be a result of distress but may also be a mismatch in the timing of a refinancing effort or a sale closing. Non-performing matured loans are opportunities for distressed investors to step in and infuse capital in situations where traditional solutions may not be an option. Maturity defaults featured this week include a loan secured by a regional mall in the Detroit, MI MSA and a loan secured by suburban office properties located in the Cleveland, OH MSA.

CRED iQ valuations factor in a base-case (most likely), a downside (significant loss of tenants), and dark scenarios (100% vacant). For full access to the valuation reports as well as full CMBS loan reporting, with detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

Southland Center Mall

611,143 sf, Regional Mall, Taylor, MI [View Details]

This $64.8 million loan failed to pay off at its July 6, 2022 maturity date after the borrower, Brookfield Property Partners, did not secure refinancing. The loan had transferred to special servicing in June 2022, prior to the loan’s maturity default in anticipation of the difficulty with refinancing. The next steps of loan workout involve negotiations between the borrower and Rialto Capital Advisors, as special servicer. A maturity extension is a likely outcome that would help further de-lever the asset and postpone attempting to refinance an unfavorable property type such as regional malls in an unfavorable lending environment.

The loan is secured by 611,143 sf of in-line and anchor space at the 903,520-sf Southland Center Mall in Taylor, MI, which is approximately 15 miles southwest of Detroit. Macy’s and JCPenney serve as traditional anchors, although the Macy’s box is not collateral for the outstanding mortgage. Junior anchors at the mall include Best Buy and Cinemark, neither of which are compelling tenants from a revenue growth and longevity perspective. The mall was 91% occupied as of March 2022. Despite stable occupancy, CRED iQ’s valuation of the asset indicates a value deficiency compared to the outstanding loan amount. For the valuation report and loan-level details, click here.

| Property Name | Southland Center Mall |

| Address | 2300 Eureka Road Taylor, MI 48180 |

| Loan Balance | $64,791,236 |

| Interest Rate | 5.09% |

| Maturity Date | 7/6/2022 |

| Most Recent Appraisal | $114,400,000 ($187/sf) |

| Most Recent Appraisal Date | 4/22/2012 |

| CRED iQ Base-Case Value | Requires Log In |

Cleveland East Office Portfolio

499,454 sf, Suburban Office, Cleveland, OH MSA [View Details]

This $39.5 million loan failed to pay off at maturity on July 6, 2022. The maturity default was expected, evidenced by a preemptive transfer of the loan to special servicing in May 2022. According to servicer commentary, the borrower submitted a proposal for a loan modification; however, the special servicer also commenced foreclosure proceedings to facilitate a workout. The loan, which has an interest rate of 5.217%, is secured by two suburban office properties located in the Cleveland, OH MSA.

| Property Name | Size (sf) | Address | Allocated Loan Amount | Most Recent Appraisal | Most Recent Appraisal Date | CRED iQ Base-Case Value |

| Landerbrook Corporate Center | 336,349 | 5900 – 5920 Landerbrook Drive Mayfield Heights, OH 44124 | $27,653,523 | $42,000,000 ($125/sf) | 2/21/2017 | Requires Log In |

| Metropolitan Plaza | 163,105 | 22901 Millcreek Boulevard Highland Hills, OH 44122 | $11,851,509 | $18,000,000 ($110/sf) | 2/21/2017 | Requires Log In |

Landerbrook Corporate Center

Landerbrook Corporate Center is a three-building office park located in Mayfield Heights, OH, 12 miles east of Cleveland. The property was 89% occupied as of March 2022 but faces near-term lease rollover risk. The property’s largest tenant, Progressive Insurance, plans to vacate at lease expiration. The tenant accounts for 34% of the office park’s NRA and the departure will leave the property approximately 55% occupied. For the full valuation report and loan-level details, click here.

Metropolitan Plaza

Metropolitan Plaza is a six-story office building in Highland Hills, OH, located approximately 10 miles southeast of Cleveland. The property was nearly 100% occupied at loan origination in 2017 but the office building’s primary tenants vacated in recent years. Namely, the property’s former largest tenant, Victoria Fire & Casualty Co., vacated at lease expiration in September 2020. The tenant occupied 86,183 sf of space, accounting for approximately 53% of the building’s NRA. The office was 34% occupied as of March 2022. For the full valuation report and loan-level details, click here.

1867-1871 Amsterdam Avenue

7,582 sf, Mixed Use (Office/Multifamily), New York NY [View Details]

This $4.1 million loan failed to pay off at its maturity date on June 6, 2022. Prior to the maturity default, the loan had transferred to special servicing in March 2021 due to delinquency. Without any successful attempts to cure the loan by the borrower, the next step in workout may be foreclosure; however, an extended workout period may be required given the property’s New York City jurisdiction. The loan is secured by a 7,582-sf mixed-use building located in the Sugar Hill submarket of Manhattan, NY. The property consists of primarily ground-floor retail space with a small multifamily component. The property has been unable to recover from pandemic-induced distress. For the full valuation report and loan-level details, click here.

| Property Name | 1867-1871 Amsterdam Avenue |

| Address | 1867-1871 Amsterdam Avenue New York, NY 10031 |

| Loan Balance | $4,100,000 |

| Interest Rate | 5.65% |

| Maturity Date | 6/6/2022 |

| Most Recent Appraisal | $8,400,000 ($1,328/sf) |

| Most Recent Appraisal Date | 5/8/2017 |

| CRED iQ Base-Case Value | Requires Log In |

Stanley Apartments

40 units, Multifamily, Stanley, ND [View Details]

This $3.7 million loan transferred to special servicing after a maturity default on June 6, 2022. This is the second maturity default for the loan. The loan was originated in July 2014 and had an original maturity date of June 2019. The loan failed to pay off at its June 2019 maturity date and a subsequent loan modification extended the maturity date to June 2022.

The loan is secured by a 39-unit multifamily property in Stanley, ND, which is located within the Bakken Formation. Shortly after loan origination, the property was adversely impacted by volatility in the oil and gas industry. After several years of severe fluctuations in demand, occupancy for the property appears to be stabilized. However, rental rates for the apartments in the region are significantly lower than rates when the loan was originated in 2014. For the full valuation report and loan-level details, click here.

| Property Name | Stanley Apartments |

| Address | 901 5th Street SE Stanley, ND 58784 |

| Loan Balance | $3,277,865 |

| Interest Rate | 5.41% |

| Maturity Date | 6/6/2022 |

| Most Recent Appraisal | $3,200,000 ($80,000/unit) |

| Most Recent Appraisal Date | 8/7/2019 |

| CRED iQ Base-Case Value | Requires Log In |

For full access to our loan database and valuation platform, sign up for a free trial below:

About CRED iQ

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. Our data platform is powered by over $2.0 trillion of CMBS, CRE CLO, SBLL, and GSE Agency loan and property data.