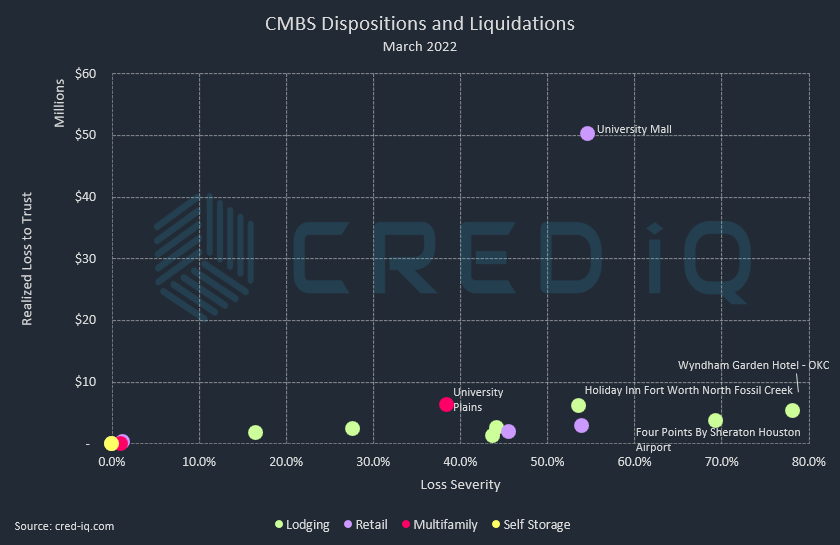

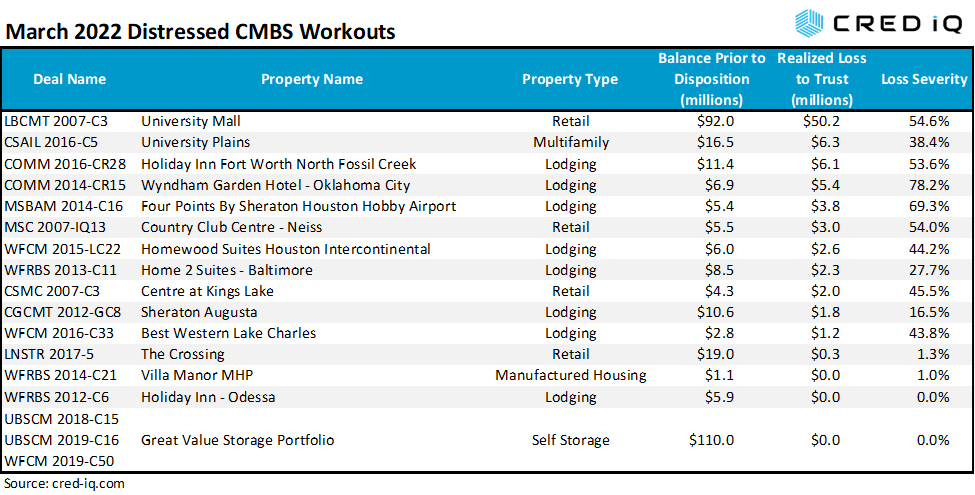

CMBS conduit transactions incurred approximately $84 million in realized losses during March 2022 through the workout of distressed assets. CRED iQ identified 16 workouts classified as dispositions, liquidations, or discounted payoffs. Of those 16 workouts, only two were resolved without a loss. One resolution – Sheraton Denver West — resulted in excess proceeds available to the trust after the REO asset was sold. The sales price for the asset was greater than its total exposure, equal to its unpaid balance, servicer advances, and additional expenses. Loss severities for the month of March ranged from 1% to 78%, based on outstanding balances at disposition. Total realized losses in March represented a decline compared to February’s realized loss totals of approximately $191.3 million.

The largest loss, by total amount, was the liquidation of University Mall, which was an REO regional mall located in Burlington, VT. The property had been with the special servicer since July 2015. The REO liquidation resulted in a $50.2 million loss on an unpaid balance of $92 million, resulting in a loss severity of 54.6%. The loss was allocated to the LBCMT 2007-C3 CMBS conduit transaction, one of the few remaining legacy CMBS deals that are still active.

The largest distressed loan, by outstanding balance, to be resolved was the $110 million Great Value Storage Portfolio loan, which was split pari passu across three CMBS conduit deals. The debt stack for the collateral also included mezzanine loans totaling $166 million. The loan had transferred to special servicing in June 2021 due to bankruptcy of the borrower. It is worth noting that the loan was subject of a demand to repurchase due to a breach of representations and warranties. The portfolio was acquired by a joint venture between CBRE and The William Warren Group/StorQuest for $588 million, well above the total debt amount.

Like the previous month, lodging properties made up the majority of distressed workouts, accounting for eight of the 16 dispositions. The average loss severity for lodging workouts was approximately 42%. The highest loss severity was associated with the liquidation of Wyndham Garden Hotel – Oklahoma City, a 244-key hotel that became REO in July 2020. The asset had an unpaid principal balance of $6.9 million at disposition and its sale resulted in a $5.4 million loss, equal to a 78.2% severity.

Also notable among March workouts was the liquidation of the $16.5 million University Plains, a 540-bed student housing facility catered to enrollees at Iowa State University. The REO asset had been specially serviced since November 2018 and was liquidated with a 38.4% severity.

Excluding defeased loans, there was approximately $3.3 billion in securitized debt that was paid off or worked out in March, which was comparatively lower than $5.2 billion in February. In March, 10% of the loan resolutions were categorized as dispositions, liquidations, or discounted payoffs. An additional 14% of the loans paid off with prepayment penalties.

By property type, lodging had the highest total of outstanding debt paid off in March, led by the retirement of an $828.4 million mortgage secured by a portfolio of WoodSpring Suites hotels and the payoff of a $294.6 million loan secured by a La Quinta Hotel Portfolio.

CRED iQ is a commercial real estate data, analytics, and valuation platform designed to unlock investment, financing, and leasing opportunities. CRED iQ provides real-time property, loan, tenant, ownership, and valuation data for over $2.0 trillion of commercial real estate.

Properties and loan notes securing more than $217 million in outstanding CMBS debt were auctioned during Q1 2022, potentially setting the stage for another wave of losses for investors, with opportunity for a few gains on sale sprinkled in the mix. The volume of CMBS auctions for Q1 2022 represents a decline from Q4 2021 when approximately 50 auctions tied to approximately $550 million in CMBS debt took place. Typically, sales via an auction process can close within 60 to 90 days; however, complications can arise during due diligence periods that can prevent a sale from transacting. The majority of Q4 2021 auctions resulted in the retirement of associated outstanding debt, but 14 auctioned assets backing $137.3 million in CMBS debt remained unresolved as of the March 2022 reporting period.

CRED iQ monitored 30 individual CMBS property and note sales through their respective auction processes during Q1 2022. All except one of those auctions involved distressed sales facilitated by a special servicer. Most auction sales involved REO properties — assets that special servicers have taken over control with the task of maximizing proceeds after title reverts to the CMBS trusts.

Of the REO properties that were auctioned, the average holding period between title acquisition and auction date was approximately 1.5 years. The shortest holding period was about three months, and the longest holding period was just under five years. The quickest auction from REO title date to auction date was the 292-key Hilton Houston Galleria TX. The property transferred to special servicing in July 2020 but had operational issues prior to the pandemic in 2019. Foreclosure of the hotel was completed on February 1, 2022 and the REO asset was marketed for sale less than two months after. The property reportedly sold for $14 million, which is below the asset’s outstanding debt amount. Additionally, net proceeds available to the trust likely would come in lower to account for the repayment of servicer advances, interest on servicer advances, and other liquidation expenses.

By deal vintage, auctions over the past three months were most prevalent among 2015 vintage deals while 2014, 2017, and 2018 vintages had notable volume as well. Comparing to the prior quarter, 2014 and 2016 vintage deals had the most auction activity. Similar to the previous quarter, hotels represented the majority of auctions with 12 attempted sales during Q1 2022. Retail was close behind with 10 auction events. By market, the Philadelphia MSA was most represented in auction activity, including the 200 Precision Drive office property in Horsham, PA and a 126-key Courtyard by Marriott in Wilmington, DE.

Perhaps most useful from CRED iQ’s observations of recent auction activity is the resulting pricing discovery from assets’ final bids. All but two of the auctioned CMBS properties during Q1 2022 were appraised in 2020 or 2021. Excluding the two stale appraisals, we found that 62% of the auctioned assets received final bids that were higher than their recent appraisals. The average premium was approximately 30%, including the highest premium of approximately 78% for a multifamily property in southern New Jersey. When properties traded at a discount to the most recent appraisal, the average difference was approximately -20%. The most severe discount from appraisal to final bid, equal to about -71%, was a vacant freestanding grocery store in Indiana. Altogether, the average difference between final bid prices and prior appraisals was approximately +9%. Lodging properties, on average, exhibited a -6% difference and retail assets had an average +14% difference between final bid price and most recent appraisal.

For access to the underlying data behind this research, please contact us: team@cred-iq.com.

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. Our data platform is powered by over $2.0 trillion of CMBS, CRE CLO, SBLL, and GSE Agency loan and property data.

Our technology transforms multiple data sets into actionable insights for CRE brokers, lenders and investors. Easily build your targeted list of properties and pinpoint value-add, off-market opportunities, expiring leases and maturing loans. Leverage the only platform equipped with the full universe of securitized loan data, interactive DCF valuations, and ownership contact information.

Grow your business faster than ever with CRED iQ. Sign up for CRED iQ today.

This week, CRED iQ reviewed the commercial real estate lending landscape and highlighted five properties that have secured financing in March 2022. The highlighted loan originations feature five different property types — office, retail, industrial, multifamily and self storage. The two largest new originations are secured by properties located in the Los Angeles MSA.

Using the CRED iQ platform’s Comps functionality, which features propriety Comps scoring for the CRE loan universe, we compared lending terms and loan structures to get a sense of the trends in the CRE lending environment. Additionally, we provided valuations for each asset to evaluate leverage levels in relation to originators’ LTVs. The CRED iQ valuations factor in a base-case (most likely), a downside (significant loss of tenants), and dark scenarios (100% vacant). Base-case valuations for select properties are provided below. For access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

122,411 sf, Medical and Creative Office, Los Angeles, CA

A $68 million loan was originated by Deutsche Bank on March 11, 2022 to refinance existing debt on two office properties in Hollywood, CA. As part of the transaction, approximately $10.8 million of equity was returned to the borrower. The interest-only loan has a 10-year term and was structured with an interest rate of 4.44%. The loan will be locked out from prepayment for about two years, and defeasance will be permitted after lockout through the remainder of the loan term until its open period, seven months prior to maturity.

Using CRED iQ’s Comps functionality, the highest scoring loan comparison was Henson Studio, which is secured by a 79,940-sf creative office owned by the Jim Henson Company. The loan was originated in May 2017 with a balance of $5.1 million, which has since amortized to a balance of $3 million. The comparable loan’s interest rate is 4.76%, which is 32 bps higher than the new origination presumably due to the single-tenant, owner-occupied nature of Henson Studio.

Romaine & Orange Square comprises two buildings. The larger 91,286-sf building is a six-story medical office building that features four levels of parking, including a subterranean garage. Despite the parking component, the buildings primary tenant, healthcare provider Kaiser, requires additional parking to satisfy its business needs. Kaiser occupies 79% of the NRA of the larger office building. Kaiser’s lease expires in September 2028, which is more than three years before loan maturity. The smaller property is a 31,125-sf creative office building that features multiple tenants that require media and post-production space.

The property was appraised at a value of $109 million ($890/sf) as of January 11, 2022. The appraisal resulted in an LTV of 62%, and an implied cap rate of 4.99% based on the originator’s underwritten NCF. The debt yield came in at 8.0%, also based on NCF from the originator’s underwriting. For the full valuation report and loan-level details, click here.

Subject Property

Name

Romaine & Orange Square

Address

7007 Romaine Street Los Angeles, CA 90038

Property Type

Office

Property Subtype

CBD

Property Size

122,411 sf

Year(s) Built

2018 and 1928

Submarket

Hollywood

County

Los Angeles

MSA

Los Angeles-Long Beach-Santa Ana, CA

Origination Date

3/11/2022

Loan Amount

$68,000,000

Interest Rate

4.44%

Debt Yield (UW NCF)

8.00%

Valuation

Appraised Value

$109,000,000 ($890/sf)

Appraisal Date

1/11/2022

Appraisal LTV

62.30%

CRED iQ Base-Case Value

$91,850,000 ($750/sf)

Whizin Market Square

136,746 sf, Retail, Agoura Hills, CA

Benefit Street Partners Realty Trust funded a $40.25 million mortgage on March 14, 2022 to refinance existing floating-rate debt on Whizins Mall Shopping Center, a retail property in Agoura Hills, CA, located approximately 40 miles west of Los Angeles. The loan has a term of 10 years and requires interest-only debt service payments with an interest rate of 4.76%. Prepayment provisions for the loan include yield maintenance until the loan’s open period, which starts four months prior to maturity. One of CRED iQ’s highest scoring comps is an $11 million loan secured by the Agoura Meadows Shopping Center, which is located less than a mile away from Whizin Market Square. The comparable loan was originated in February 2020 and had an interest rate of 3.16%, which is more than 150 bps lower than the new origination.

Whizin Market Square is a six-building retail center with high visibility along Ventura Freeway, although access to the property requires an off-ramp exit to a parallel road. The property’s largest tenant is a DIY Home Center, which operates in a 40,500-sf freestanding building. The tenant accounts for 30% of the property’s NRA and has a lease that expires in December 2026. The remaining tenant roster consists of many small businesses without a noticeable presence of national retailers. A December 26, 2021 appraisal resulted in a value of $64 million ($468/sf), equal to an LTV of 63%. The implied cap rate based on the originator’s underwritten NCF was 5.55% and the debt yield was equal to 8.8% based on the same metric. For the full valuation report and loan-level details, click here.

Bank of Montreal originated a $20.8 million loan on March 11, 2022 to finance the acquisition of a 638,595-sf manufacturing facility in Cincinnati, OH. The interest-only loan has a 10-year term and an interest rate of 4.80%. The loan will be locked out from prepayment for about two years, and defeasance will be permitted after lockout through the remainder of the loan term until its open period, four months prior to maturity. Many of CRED iQ’s property comps for the VVF manufacturing facility are part of larger industrial portfolios and trend towards more traditional warehouse use types. The highest scoring comparable property was 500 Murray Road, a 366-584-sf single tenant warehouse located approximately one mile away from VVF. The loan was originated in 2015 and had a 4.03% interest rate.

The VVF collateral property is a single-tenant manufacturing facility. VVF manufactures personal care products, and the property primarily engages in the production of bar soap. The facility has extensive rail access and capabilities, including one of the largest rail yards in the region. VVF’s lease is structured as NNN and is scheduled to expire in February 2042, which is approximately 10 years after loan maturity. A January 31, 2022 appraisal stated a value of $35.9 million ($56/sf), equal to an LTV of 58%. The implied cap rate based on the originator’s underwritten NCF was 6.30% and the debt yield was equal to 10.9% based on the same metric. For the full valuation report and loan-level details, click here.

Subject Property

Name

VVF

Address

5117 Spring Grove Avenue Cincinnati, OH 45217

Property Type

Industrial

Property Subtype

Manufacturing

Property Size

638,595 sf

Year(s) Built

1888

Submarket

Hamilton County West

County

Hamilton

MSA

Cincinnati-Middletown, OH-KY-IN

Origination Date

3/11/2022

Loan Amount

$20,820,000

Interest Rate

4.80%

Debt Yield (UW NCF)

10.86%

Valuation

Appraised Value

$35,900,000 ($56/sf)

Appraisal Date

1/31/2022

Appraisal LTV

57.99%

CRED iQ Base-Case Value

$35,800,000 ($56/sf)

Oak Ridge Apartments

208 units, Multifamily, Southfield, MI

A $9 million loan was originated by Starwood Mortgage Capital on March 14, 2022 to refinance a $4 million Fannie Mae loan that was secured by Oak Ridge Apartments, a 208-unit multifamily property located in Southfield, MI. The existing debt had an interest rate of 7.22% and was not scheduled to mature until December 2031. The new origination has an interest rate of 4.56%. The 10-year loan amortizes based on a 30-year schedule. The loan will be locked out from prepayment for about two years, and defeasance will be permitted after lockout through the remainder of the loan term until its open period, four months prior to maturity.

One of CRED iQ’s highest scoring comps is a $5.7 million loan originated by Citigroup on November 17, 2021 that is secured by Willow Tree Apartments, a 78-unit multifamily property located less than a mile away from Oak Ridge Apartments. The comparable loan had an interest rate of 3.73% with a similar loan structure.

Oak Ridge Apartments was appraised at a value of $16.4 million ($78,846/unit) as of February 16, 2022. The appraisal resulted in an LTV of 55%, and an implied cap rate of 5.52% based on the originator’s underwritten NCF. The debt yield came in at 10.0%, also based on NCF from the originator’s underwriting. For the full valuation report and loan-level details, click here.

Subject Property

Name

Oak Ridge Apartments

Address

26717 Berg Road Southfield, MI 48034

Property Type

Multifamily

Property Subtype

Garden Style

Property Size

208 units

Year(s) Built

1979

Submarket

Southfield N of 10 Mile

County

Oakland

MSA

Detroit-Warren-Livonia, MI

Origination Date

3/14/2022

Loan Amount

$9,000,000

Interest Rate

4.56%

Debt Yield (UW NCF)

10.05%

Valuation

Appraised Value

$16,400,000 ($78,846/unit)

Appraisal Date

2/16/2022

Appraisal LTV

54.88%

CRED iQ Base-Case Value

$13,820,000 ($66,465/unit)

Buckley Self Storage & RV

82,720 sf, Self Storage and RV Parking, Buckley, WA

A $2.75 million loan was originated by Benefit Street Partners Realty Trust on March 17, 2022 to refinance existing debt on a self storage and RV parking facility located in Buckley, WA, approximately 40 miles southeast of Seattle. The 10-year loan was structured to amortize based on a 30-year schedule and has an interest rate of 5.44%. The loan will be locked out from prepayment for about two years, and defeasance will be permitted after lockout through the remainder of the loan term until its open period, four months prior to maturity. CRED iQ’s highest scoring loan comp is a $6 million loan secured by Enumclaw Plateau Self Storage, which is located about 10 miles away from Buckley Self Storage. The comparable loan was originated in May 2021 and had an interest rate of 3.71%, which is more than 150 bps lower than the new origination.

Buckley Self Storage, which includes 62 recreational vehicle pads, was appraised at a value of $5.3 million ($64/sf) as of February 10, 2022. The appraisal resulted in an LTV of 52%, and an implied cap rate of 6.97% based on the originator’s underwritten NCF. The debt yield came in at 13.4%, also based on NCF from the originator’s underwriting. For the full valuation report and loan-level details, click here.

Subject Property

Name

Buckley Self Storage & RV

Address

26306 Washington 410 Buckley, WA 98321

Property Type

Self Storage

Property Subtype

Recreational Vehicle Parking

Property Size

82,720 sf

Year(s) Built

1988

Submarket

Buckley

County

Pierce

MSA

Seattle-Tacoma-Bellevue, WA

Origination Date

3/17/2022

Loan Amount

$2,750,000

Interest Rate

5.44%

Debt Yield (UW NCF)

13.40%

Valuation

Appraised Value

$5,300,000 ($64/sf)

Appraisal Date

2/10/2022

Appraisal LTV

51.90%

CRED iQ Base-Case Value

$5,063,000 ($61/sf)

For full access to our loan database and valuation platform, sign up for a free trial below:

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. Our data platform is powered by over $2.0 trillion of CMBS, CRE CLO, SBLL, Ginnie Mae, FHA/HUD, and Agency loan and property data.

CRED iQ monitors distressed rates (DQ + SS%) and market performance for nearly 400 MSAs across the United States, covering over $900 billion in outstanding CRE debt. Distressed rates include loans that are specially serviced, delinquent, or a combination of both. Distressed rates and month-over-month changes are presented below, by property type, for the 50 largest markets.

Distressed figures include all properties listed 30 days delinquent or worse, as well as specially serviced loans within the securitized universe including Conduit, Agency, SBLL, and CRE CLO.

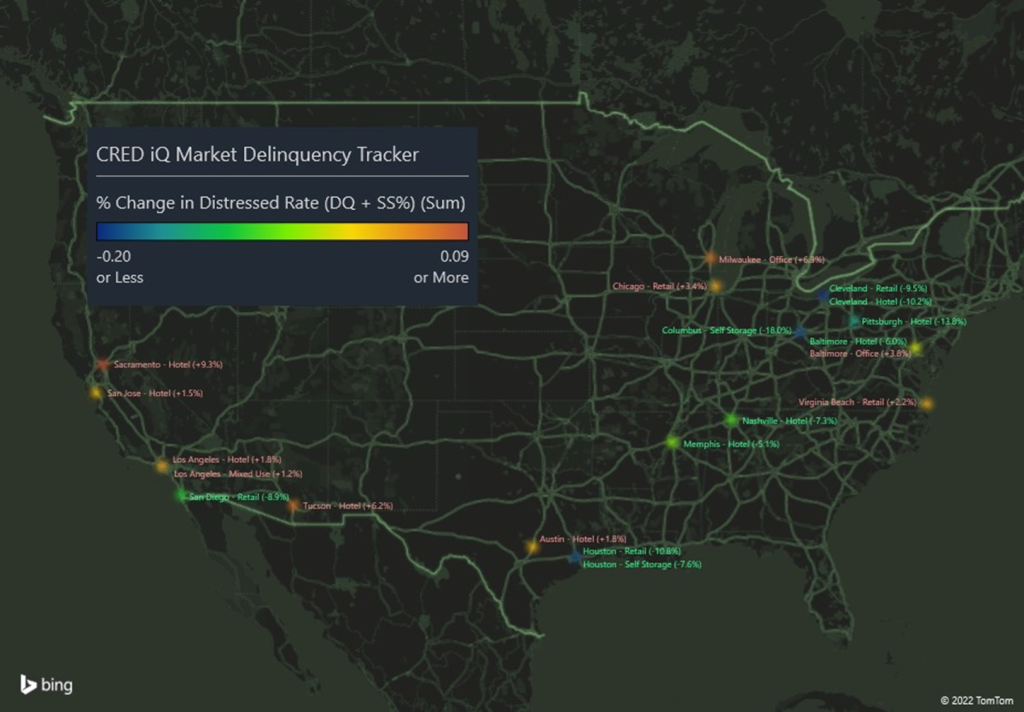

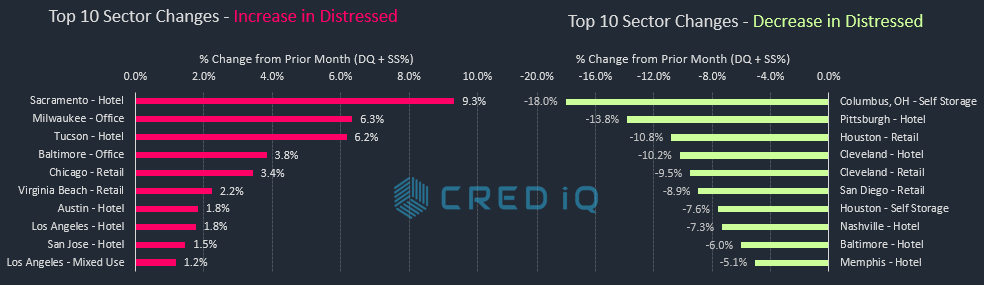

The lodging sector exhibited an overall decline in the rate of distressed mortgages in March 2022 to 13.1%, compared to 13.3% in February. However, a more granular view stratified across all lodging markets reveals that nearly half of the Top 50 MSAs exhibited increases in distress on a stand-alone basis. There were 23 total markets out of the Top 50, equal to 46%, with month-over-month increases in the percentage of distressed loans. Hotels accounted for five of the Top 10 increases in distress by market-sector and included Sacramento, Tucson, Austin, Los Angeles, and San Jose. The Sacramento lodging market had the largest increase in distress this month, which was primarily caused by a 30-day delinquency of a $34 million loan secured by The Citizen Hotel Sacramento. The loan previously entered into a forbearance agreement in October 2020.

The Baltimore office market appeared on the list of Top 10 increases in distress by market-sector for the second month in a row. This month, a $24.8 million loan secured by 300 East Lombard, a 19-story office tower located in the Inner Harbor, transferred to special servicing due to the impending departure of the property’s largest tenant, Ballard Spahr. Ballard Spahr’s lease expires at the end of April 2022 and accounts for 15% of the property’s NRA. The Milwaukee office market was also notable for an increase in distress, which was primarily driven by the special servicing transfer of The Pinnacle at Bishop’s Woods, a three-building suburban office property that secures a $29.1 million loan.

As noted above, improvements in distressed rates this month were most common for lodging markets. Half of the Top 50 MSAs exhibited lower distressed rates for loans secured by lodging collateral compared to the prior month. Five of the largest decreases by market-sector in March were lodging markets, including Pittsburgh and Cleveland. The Cleveland lodging market remains one of the most severely distressed market-sectors with 39.6% of loans that are distressed.

Distressed rates for the self-storage sector had noteworthy improvements this month after the $110 million Great Value Storage Portfolio loan paid off in full, ahead of its scheduled maturity date in December 2023. The loan had previously transferred to special servicing in June 2021 due to the bankruptcy of the borrower, Natin Paul. The majority of the 64 properties in the collateral portfolio were located in the Houston and Columbus, OH MSAs. Both market-sectors were among the list of Top 10 improvements in distress this month.

The Minneapolis MSA has the highest overall distressed rate at 23.0%, which was slightly higher than the prior month. Louisville (17.7%), New Orleans (13.4%), Milwaukee (11.3%), and St. Louis (9.73%) comprise the remaining markets with the highest rates of distress. The Cleveland MSA had the fourth-highest distressed rate as of February 2022 but dropped out of the Top 5 distressed markets this month after delinquency and special servicing cures for multiple retail loans. The Raleigh market (0.34%) had the lowest percentage of distress among the Top 50 MSAs for the third consecutive month. The Sacramento MSA also remained one of the Top 5 markets with the lowest percentage of distressed loans this month, despite the relatively large delinquency of The Citizen Hotel Sacramento loan.

Riverside – Riverside-San Bernardino-Ontario, CA MSA

$308.9

3.3%

0.0%

Riverside – Hotel

$79.4

25.8%

-1.2%

Riverside – Industrial

$0.0

0.0%

0.0%

Riverside – Multifamily

$08.1

0.2%

0.2%

Riverside – Office

$0.0

0.0%

0.0%

Riverside – Other

$0.0

0.0%

0.0%

Riverside – Retail

$221.4

10.4%

-0.2%

Riverside – Self Storage

$0.0

0.0%

0.0%

Sacramento – Sacramento-Arden-Arcade-Roseville, CA MSA

$59.4

1.0%

0.6%

Sacramento – Hotel

$39.7

10.9%

9.3%

Sacramento – Industrial

$0.0

0.0%

0.0%

Sacramento – Multifamily

$0.0

0.0%

0.0%

Sacramento – Office

$06.1

0.8%

0.0%

Sacramento – Other

$0.0

0.0%

0.0%

Sacramento – Retail

$13.6

1.7%

0.0%

Sacramento – Self Storage

$0.0

0.0%

0.0%

Salt Lake City – Salt Lake City, UT MSA

$46.9

1.3%

0.0%

Salt Lake City – Hotel

$46.9

16.9%

0.6%

Salt Lake City – Industrial

$0.0

0.0%

0.0%

Salt Lake City – Multifamily

$0.0

0.0%

0.0%

Salt Lake City – Office

$0.0

0.0%

0.0%

Salt Lake City – Other

$0.0

0.0%

0.0%

Salt Lake City – Retail

$0.0

0.0%

0.0%

Salt Lake City – Self Storage

$0.0

0.0%

0.0%

San Antonio – San Antonio, TX MSA

$133.8

2.1%

-0.1%

San Antonio – Hotel

$08.4

2.3%

-0.1%

San Antonio – Industrial

$0.0

0.0%

0.0%

San Antonio – Multifamily

$0.0

0.0%

0.0%

San Antonio – Office

$0.0

0.0%

0.0%

San Antonio – Other

$0.0

0.0%

0.0%

San Antonio – Retail

$125.4

14.1%

-0.2%

San Antonio – Self Storage

$0.0

0.0%

-1.0%

San Diego – San Diego-Carlsbad-San Marcos, CA MSA

$113.4

1.0%

-0.9%

San Diego – Hotel

$79.1

4.0%

0.0%

San Diego – Industrial

$0.0

0.0%

0.0%

San Diego – Multifamily

$09.5

0.2%

0.2%

San Diego – Office

$0.0

0.0%

0.0%

San Diego – Other

$20.5

3.0%

0.1%

San Diego – Retail

$04.3

0.3%

-8.9%

San Diego – Self Storage

$0.0

0.0%

0.0%

San Francisco – San Francisco-Oakland-Fremont, CA MSA

$383.1

1.6%

0.3%

San Francisco – Hotel

$171.6

7.3%

0.0%

San Francisco – Industrial

$0.0

0.0%

0.0%

San Francisco – Multifamily

$20.0

0.3%

0.0%

San Francisco – Office

$105.3

1.1%

0.5%

San Francisco – Other

$38.6

2.1%

0.4%

San Francisco – Retail

$47.6

4.0%

-0.1%

San Francisco – Self Storage

$0.0

0.0%

0.0%

San Jose – San Jose-Sunnyvale-Santa Clara, CA MSA

$135.9

0.9%

0.2%

San Jose – Hotel

$121.2

5.8%

1.5%

San Jose – Industrial

$0.0

0.0%

0.0%

San Jose – Multifamily

$0.0

0.0%

0.0%

San Jose – Office

$14.7

0.2%

0.0%

San Jose – Other

$0.0

0.0%

0.0%

San Jose – Retail

$0.0

0.0%

0.0%

San Jose – Self Storage

$0.0

0.0%

0.0%

Seattle – Seattle-Tacoma-Bellevue, WA MSA

$113.3

0.7%

0.0%

Seattle – Hotel

$109.0

8.3%

0.0%

Seattle – Industrial

$0.0

0.0%

0.0%

Seattle – Multifamily

$04.4

0.1%

0.1%

Seattle – Office

$0.0

0.0%

0.0%

Seattle – Other

$0.0

0.0%

0.0%

Seattle – Retail

$0.0

0.0%

0.0%

Seattle – Self Storage

$0.0

0.0%

0.0%

St. Louis – St. Louis, MO-IL MSA

$410.4

9.7%

-0.1%

St. Louis – Hotel

$58.1

20.6%

-0.1%

St. Louis – Industrial

$0.0

0.0%

0.0%

St. Louis – Multifamily

$24.2

1.5%

0.0%

St. Louis – Office

$107.1

19.3%

0.1%

St. Louis – Other

$23.0

4.2%

-0.6%

St. Louis – Retail

$197.9

19.8%

-0.2%

St. Louis – Self Storage

$0.0

0.0%

0.0%

Tampa – Tampa-St. Petersburg-Clearwater, FL

$300.4

3.5%

0.2%

Tampa – Hotel

$29.9

4.3%

1.7%

Tampa – Industrial

$0.0

0.0%

0.0%

Tampa – Multifamily

$02.5

0.0%

0.0%

Tampa – Office

$23.8

4.2%

0.2%

Tampa – Other

$0.0

0.0%

0.0%

Tampa – Retail

$244.2

26.7%

-0.2%

Tampa – Self Storage

$0.0

0.0%

0.0%

Tucson – Tucson, AZ MSA

$181.0

5.9%

0.5%

Tucson – Hotel

$19.4

8.1%

6.2%

Tucson – Industrial

$0.0

0.0%

0.0%

Tucson – Multifamily

$0.0

0.0%

0.0%

Tucson – Office

$0.0

0.0%

0.0%

Tucson – Other

$0.0

0.0%

0.0%

Tucson – Retail

$161.6

20.1%

-0.1%

Tucson – Self Storage

$0.0

0.0%

0.0%

Virginia Beach – Virginia Beach-Norfolk-Newport News, VA-NC MSA

$232.9

5.1%

0.4%

Virginia Beach – Hotel

$09.4

2.1%

-0.5%

Virginia Beach – Industrial

$21.2

6.9%

0.2%

Virginia Beach – Multifamily

$0.0

0.0%

0.0%

Virginia Beach – Office

$0.0

0.0%

0.0%

Virginia Beach – Other

$0.0

0.0%

0.0%

Virginia Beach – Retail

$202.3

23.0%

2.2%

Virginia Beach – Self Storage

$0.0

0.0%

0.0%

Washington, DC – Washington-Arlington-Alexandria, DC-VA-MD-WV MSA

$607.3

2.2%

0.0%

Washington, DC – Hotel

$30.0

3.4%

-1.4%

Washington, DC – Industrial

$11.2

2.0%

0.0%

Washington, DC – Multifamily

$01.2

0.0%

0.0%

Washington, DC – Office

$377.7

5.4%

0.2%

Washington, DC – Other

$44.7

2.8%

0.0%

Washington, DC – Retail

$142.5

5.2%

-0.3%

Washington, DC – Self Storage

$0.0

0.0%

0.0%

Grand Total

$24,536.3

3.7%

-0.2%

About CRED iQ

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. Our data platform is powered by over $2.0 trillion of CMBS, CRE CLO, SBLL, Ginnie Mae, FHA/HUD, and Freddie Mac loan and property data.

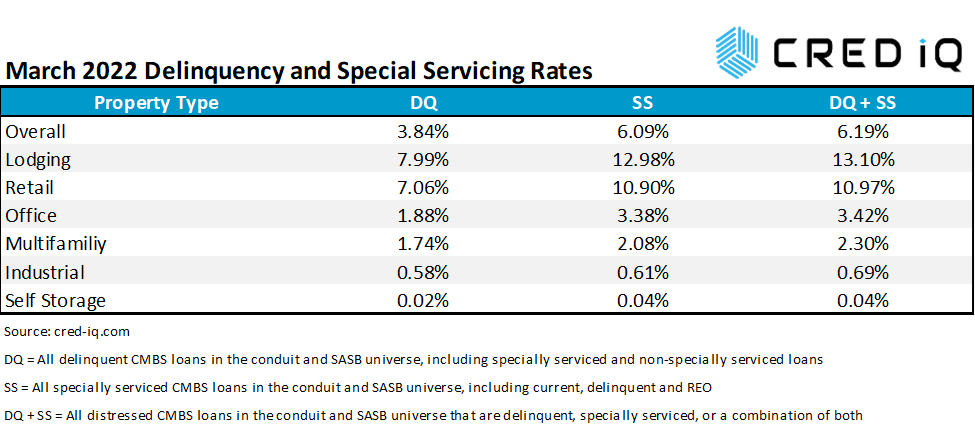

DQ = All delinquent CMBS loans in the conduit and SASB universe, including specially serviced and non-specially serviced loans SS = All specially serviced CMBS loans in the conduit and SASB universe, including current, delinquent and REO DQ + SS = All distressed CMBS loans in the conduit and SASB universe that are delinquent, specially serviced, or a combination of both

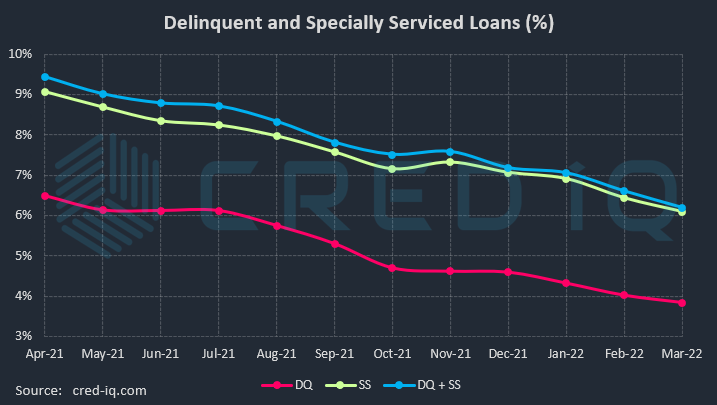

The CRED iQ overall delinquency rate for CMBS declined for the 22nd consecutive month with all major property types — retail, hotel, office, multifamily, and industrial — exhibiting improvements compared to the prior month. The delinquency rate, equal to the percentage of all delinquent specially serviced loans and delinquent non-specially serviced loans, for CRED iQ’s sample universe of $500+ billion in CMBS conduit and single asset single-borrower (SASB) loans was 3.84%, which compares to the prior month’s rate of 4.02%. CRED iQ’s special servicing rate, equal to the percentage of CMBS loans that are with the special servicer (delinquent and non-delinquent), declined month-over month to 6.09% from 6.43%. A combination of workouts, liquidations, cures, and mortgage rehabilitations have enabled the special servicing rate to decline for the fourth consecutive month. Aggregating the two indicators of distress – delinquency rate and special servicing rate – into an overall distressed rate (DQ + SS%) equals 6.19% of CMBS loans that are specially serviced, delinquent, or a combination of both. The overall distressed rate declined compared to the prior month rate of 6.40%. The overall distressed rates typically track slightly higher than special servicing rates as most delinquent loans are also with the special servicer.

DQ = All delinquent CMBS loans in the conduit and SASB universe, including specially serviced and non-specially serviced loans SS = All specially serviced CMBS loans in the conduit and SASB universe, including current, delinquent and REO DQ + SS = All distressed CMBS loans in the conduit and SASB universe that are delinquent, specially serviced, or a combination of both

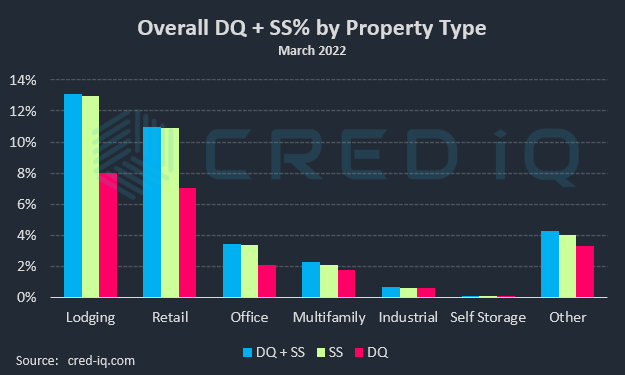

Lodging has shown the most improvement in individual delinquency rates by property type with a 46% decline over the trailing 12 months. The outstanding balance of delinquent lodging loans decreased by more than $450 million compared to the prior month. The lodging delinquency rate was 7.99% this month, which compared to 8.46% a month ago and 14.73% a year ago. An example of a contribution to the decline in the delinquency rate for lodging was the $75.5 million W Chicago – City Center loan, which was paid current and returned to the master servicer in February after a modification.

The delinquency rate for office moved nominally to 1.88%, compared to 1.89% as of February 2022. A subplot to the nominal month-over-month decline is the industry’s anticipation of a special servicing transfer for the $308 million 1740 Broadway loan. Commercial Observer first broke the news of Blackstone handing back the keys to 1740 Broadway in a March 21, 2022 article. The property’s largest tenant, L Brands, had a lease expire in March 2022 and the company vacated, relocating to 55 Water Street. The transfer to special servicing was not reflected in March 2022 servicer data; however, a delinquency is possible in the near term given the recent developments with the loan. Adjusting for the potential delinquency of 1740 Broadway would push the office delinquency over 2.00%.

Special servicing rates for lodging (12.98%), retail (10.90%), and multifamily (2.08%) declined compared to the prior month. The special servicing rate for office increased to 3.38% this month, compared to 3.31% last month, and the industrial special servicing rate increased nominally. Special servicing transfers of loans secured by office properties have steadily occurred throughout Q1 2022. Notable transfers for the March 2022 reporting period include The Pinnacle at Bishop’s Woods in the Milwaukee, WI MSA and 300 East Lombard in Baltimore, MD.

One of the largest loans to transfer to special servicing this month was the $237.2 million Walden Galleria mortgage, which is secured by a 1.5 million-sf portion of a super-regional mall in Buffalo, NY. The loan is scheduled to mature in May 2022 and the borrower, Pyramid Management Group, has reportedly requested a maturity extension. Despite the special servicing transfer, the loan remained current in payment. The loan previously transferred to special servicing in April 2020 and subsequently returned to the master servicer in December 2020 after a modification.

DQ + SS = All distressed CMBS loans in the conduit and SASB universe that are delinquent, specially serviced, or a combination of both

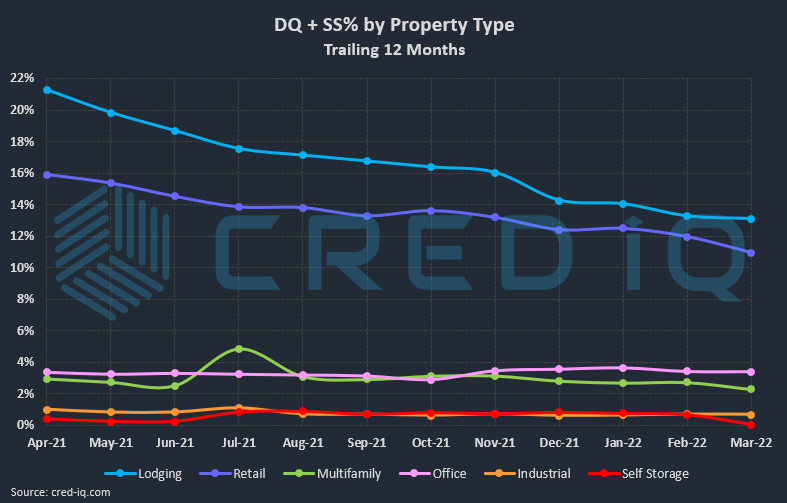

CRED iQ’s overall CMBS distressed rate (DQ + SS%) by property type accounts for loans that qualify for either delinquent or special servicing subsets. This month, distressed rates decreased for all property types. In addition to Walden Galleria, the $80 million Chicago Ridge Mall was also one of the largest loans to transfer to special servicing this month. The Chicago Ridge Mall loan has a near-term maturity date, July 6, 2022, and a timely pay off appears to be unlikely. For additional information about these two loans, click View Details below:

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. Our data platform is powered by over $2.0 trillion of CMBS, CRE CLO, SBLL, and GSE Agency loan and property data.

In this week’s WAR Report, CRED iQ calculated real-time valuations for five distressed properties that have transferred to special servicing in March 2022. Among these is a Chicago-area regional mall that is controlled by Starwood Capital Group. Additionally, there are two office properties featured, including a suburban office campus in the Milwaukee, WI MSA and a CBD office tower in Baltimore, MD. The final two highlighted properties comprise a student housing building in western Pennsylvania and a mixed-use property in San Francisco, CA.

CRED iQ valuations factor in a base-case (most likely), a downside (significant loss of tenants), and dark scenarios (100% vacant). For full access to the valuation reports as well as full CMBS loan reporting, including detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

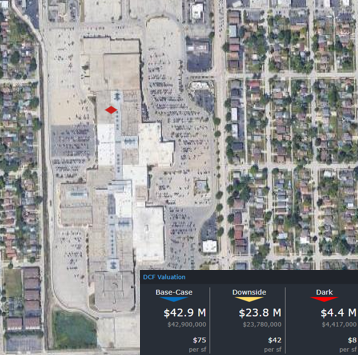

Chicago Ridge Mall

568,915 sf, Regional Mall, Chicago Ridge, IL [View Details]

Yet another regional mall controlled by Starwood Capital Group will need a special servicing workout. The Chicago Ridge Mall, which secures an $80 million mortgage, transferred to Trimont Real Estate Advisors, as special servicer, on March 14, 2022. A reason for the transfer was not initially cited, but the mall’s cash flows were severely impacted by the pandemic and performance has not recovered to pre-pandemic levels. The loan sponsor is a joint venture that is controlled by Starwood Property Group — CRED iQ recently featured a portfolio of Starwood malls in its March 8, 2022 WAR Report. The loan was scheduled to mature in July 2022, but a payoff is unlikely given the value impairment of the collateral. CRED iQ is also watching for a potential title transfer from the borrowing entity to the CMBS trust.

Chicago Ridge Mall is located about 16 miles outside of Chicago, IL and has a total size of 867,955 sf, but only 568,915 sf serve as collateral for the mortgage. There is a vacant 211,858-sf parcel that was formerly occupied by Sears until it closed in 2021. The vacant anchor box is owned by Transformco and there are no immediate plans for redevelopment. Kohl’s also operates as an anchor at the mall and owns its building. Kohl’s, which has been the subject of takeover speculation over the past month, was featured in last week’s WAR Report, which explored CMBS exposure to Kohl’s store locations.

The largest collateral tenants at Chicago Ridge Mall include Dick’s Sporting Goods (9% of NRA), Bed Bath & Beyond (7% of NRA), and AMC Theatres (6% of NRA). Dick’s Sporting Goods opened in 2021 and partially backfilled space that was left vacant by Carson Pirie Scott, a former department store anchor. Aldi provides a grocery component at the mall with a 20,042-sf space, but the tenant has a right to terminate its lease at any time given a 24-month notice. The mall was 80% occupied as of September 2021, which was an improvement compared to 70% occupancy during the prior year. Net cash flow for 2021 was on pace to be over 30% below pre-pandemic levels from year-end 2019. For the full valuation report and property-level details, click here.

248,175 sf, Suburban Office, Brookfield, WI [View Details]

This $29.1 million loan transferred to special servicing on March 1, 2022 due to low occupancy at the collateral property, a three-building suburban office park. The loan’s DSCR has declined for three consecutive years and was most recently reported as 1.09 for the nine-month period ending September 2021. Occupancy across the three collateral office buildings was 67% as of September 2021. The next steps of workout are likely to address the low occupancy across the office portfolio and to mitigate a high concentration of lease rollover in 2022 at the smallest of the three buildings, Pinnacle I.

The Pinnacle at Bishop’s Woods consists of three office properties in Brookfield, WI, approximately 10 miles west of Milwaukee: Pinnacle I (13890 Bishop’s Drive), Pinnacle II (13935 Bishop’s Drive), and Pinnacle III (13845 Bishop’s Drive). The office park first exhibited occupancy declines in 2016 when the former largest tenant, Bader Rutter & Associates (27% of the NRA), vacated Pinnacle III in favor of a CBD location in Milwaukee. A portion of the space was backfilled by a new tenant, Pentair Residential Filtration, and an existing tenant, DeWitt Ross & Stevens SC, expanded its space to offset some of the loss from Bader Rutter. More recently, the office park’s second largest tenant, Travelers Indemnity (formerly 21% of the NRA; now 11%), reduced its footprint at Pinnacle II after signing a five-year renewal in August 2021. Overall, occupancy has declined by nearly 30% since loan origination. For the full valuation report and property-level details, click here.

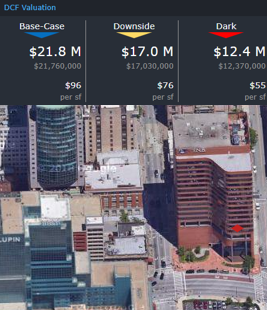

This $24.8 million loan transferred to special servicing on March 14, 2022, likely due to an impending decline in collateral occupancy. The loan is secured by a 19-story office tower located in the Inner Harbor submarket of Baltimore, MD. The Baltimore Business Journal first reported that the building’s largest tenant, law firm Ballard Spahr, planned to vacate 300 East Lombard in favor of a smaller space at 111 S. Calvert Street, a newly renovated building with more tenant amenities that is located a block closer to the harbor. CRED iQ has featured multiple Baltimore CBD office buildings in WAR Reports so far in 2022, including 650 South Exeter Street and 201 North Charles. In each of these cases of distress, tenants have either vacated, downsized, or fled to higher quality locations — exhibiting how dynamic office markets can be in an environment with remote-work and pandemic considerations.

Ballard Spahr’s lease at 300 East Lombard is scheduled to expire on April 30, 2022. The tenant accounted for 15% of the property’s NRA. CRED iQ estimates occupancy will decline to approximately 65% following the tenant’s departure. For the full valuation report and property-level details, click here.

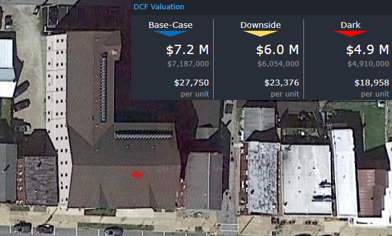

259 units, Student Housing, Indiana, PA [View Details]

This $10.5 million loan transferred to special servicing on March 11, 2022, which is two months ahead of the May 11, 2022 scheduled maturity date. The loan had a below breakeven DSCR during 2020 and through the nine-month period ended September 2021. The loan is secured by a 259-unit student housing property that caters to students enrolled at Indiana University of Pennsylvania (IUP). Enrollment at IUP has been falling for several years. Fall 2021 enrollment was 9,308 students, which represented a 7.5% decline compared to the prior year. Lower enrollment is a catalyst for lower demand and weakness in rental rates at off-campus student housing facilities. CRED iQ’s highest scoring comp for the property is IUP Pratt Studios, which transferred to special servicing in July 2021 and became REO in October 2021. For the full valuation report and property-level details for Philadelphia Square, click here.

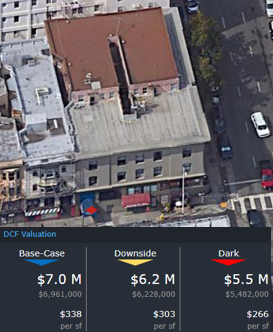

20,586 sf, Mixed-Use (Retail/Multifamily), San Francisco, CA [View Details]

This $8 million loan transferred to special servicing on March 2, 2022 due to imminent monetary default. The loan is secured by a mixed-use property located in the Nob Hill submarket of San Francisco. The three-story building consists of ground floor retail and 65 residential hotel rooms that are operated as single-room occupancy units. The single-room occupancy units are master leased by Balmoral Residences, LLC for approximately $850 per unit per month. The master lease is scheduled to expire in February 2026. Multifamily and lodging property types have faced headwinds in the San Francisco MSA since the onset of the pandemic. Early in the pandemic, there was evidence of higher multifamily vacancies. Additionally, the lodging sector has been slow to recover. With a master lease in place, it is difficult to discern the performance of Balmoral Residences; however, the residential hotel company likely faces similar struggles to other distressed multifamily and lodging properties in San Francisco. For the full valuation report and property-level details, click here.

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. Our data platform is powered by over $2.0 trillion of CMBS, CRE CLO, SBLL, Ginnie Mae, FHA/HUD, and Freddie Mac loan and property data.

Kohl’s plans to open smaller stores and transition away from department store format

The highest concentration of Kohl’s lease expirations occurs in 2024 impacting $815 million in CMBS debt

CMBS exposure to Kohl’s totals approximately $5 billion

Speculation surrounding Kohl’s and its future as a public company has been active during Q1 2022. In early-March 2022, Kohl’s provided updates on strategic initiatives for the company, which included a transition away from traditional department store operations. The retailer plans to open 100 new stores over the next four years with a smaller format than the 80,000 to 100,000-sf footprint of a Kohl’s legacy store layout. Kohl’s has reportedly faced pressure from activist investors to sell the company. Interested parties included hedge fund Starboard Value and private equity firm Sycamore Partners. Most recently, Hudson’s Bay — the former owner of failed department store Lord & Taylor — was reported to be considering a takeover bid for Kohl’s. The strategic objectives of Kohl’s management and external pressures from activist investors may lead to subsequent impacts in the commercial real estate sector.

In a takeover, many of Kohl’s owned real estate locations may be sold in a sale-leaseback transaction. Store closures or reduced footprints, in line with current management objectives, may also be possibilities for future operations. In all scenarios, retail landlords will need to adapt to the evolution of the retailer’s operational and real estate strategies.

Kohl’s operated approximately 1,165 stores as of January 2022 and owned 35% of the real estate for those locations. Kohl’s leased space for approximately 44% of its store locations. For 20% of the store locations, Kohl’s owned its building improvements and ground-leased the underlying land. Leased locations typically operate pursuant to a 20 to 25-year lease agreement with several five-year extension options.

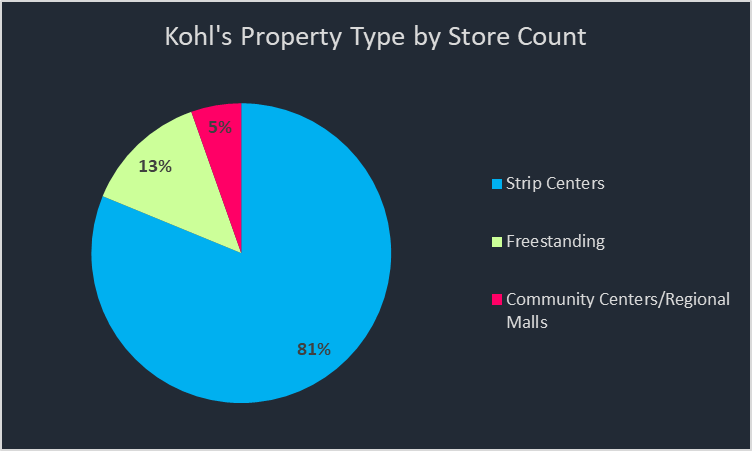

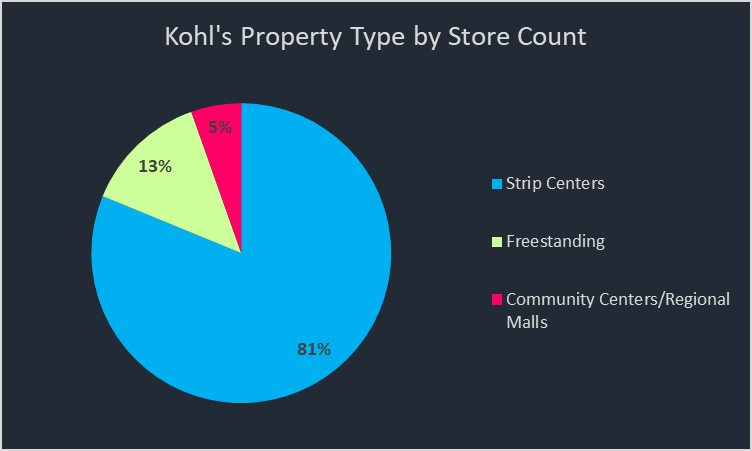

Kohl’s has been historically more versatile than counterparts JCPenney and Macy’s with the location of its stores less reliant on regional malls. Only 5% of all stores are part of a community center or regional mall. Most locations, approximately 81%, anchor smaller strip centers. Kohl’s also operates freestanding locations, which make up 13% of the total store count.

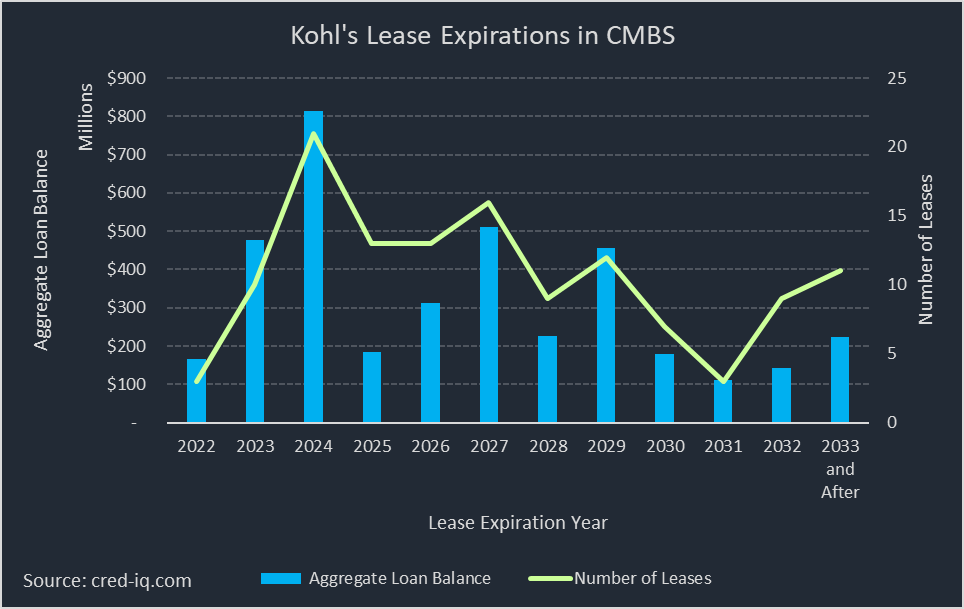

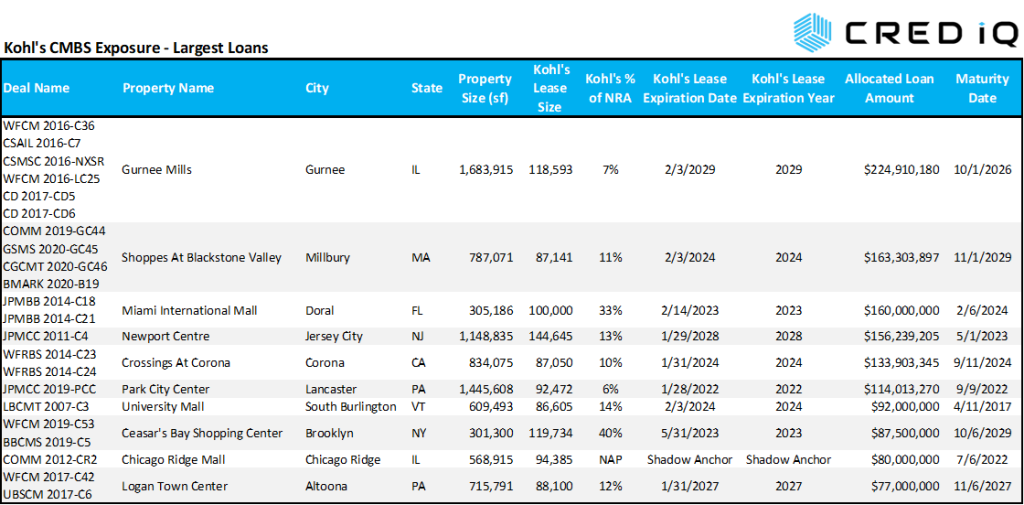

CRED iQ leveraged its platform to identify properties leased to Kohl’s and properties that are shadow-anchored by a Kohl’s store. CRED iQ identified 230 properties with exposure to Kohl’s with actionable data including lease size, lease expiration date, property information, and borrower contact information. Most leases for this group of properties have expirations within the next 10 years. There were nine leases identified with expirations in 2022, including three active CMBS loans with $167.3 million in outstanding debt. The highest concentration of lease rollover is in 2024 with 23 leases scheduled to expire. Twenty-one of these properties secure active CMBS debt totaling $815 million. Classifying properties by lease expiration date, CRED iQ was further able to isolate properties with a Kohl’s lease expiration as shown Figure 1.

Figure 1

CRED iQ identified active CMBS exposure to Kohl’s as a tenant, which totaled approximately $5 billion in outstanding mortgage debt secured by 172 properties with Kohl’s as a leased tenant or shadow anchor. There were 13 properties with Kohl’s exposure, totaling $539.9 million, that were in special servicing and in need of workout. Eight of those properties were REO and had outstanding debt of $310.5 million. University Mall in Burlington, VT is the largest REO property by outstanding debt amount with $92 million in unpaid principal balance. Kohl’s leases 86,605 sf, equal to 14% of the property’s NRA, pursuant to lease that expires in February 2024. As of February 2022, University Mall was under contract to be sold.

The implications of near-term lease expirations coupled with initiatives by Kohl’s to reduce store layout sizes could have negative impacts on CMBS collateral if the tenant opts to downsize or move to a more favorable and strategic location.

Furthermore, sale-leaseback transactions have the possibility of converting complimentary retail space into competitive space for smaller shadow-anchored retail centers. Monitoring the various scenarios may be a complicated endeavor, but still not as complicated as figuring out how to use Kohl’s Cash (it’s probably expired).

For a copy of a comprehensive list of properties with exposure to Kohl’s — including CMBS exposure, please reach out to Shane Beeson (shane@cred-iq.com) or click the link below.

a comprehensive list of 230 property records with Kohl’s exposure, including lease size and lease expiration date

all CMBS exposure to Kohl’s, including shadow anchored properties and

a complete list of all Kohl’s locations in the US (1,164 locations)

This week’s WAR Report focuses specifically on a few notable properties with Kohl’s exposure, including distressed regional malls. The third property is a freestanding single-tenant property in Tallahassee, FL that is leased to Kohl’s but went dark when the tenant vacated. CRED iQ provided updated real-time valuations for each of the properties.

CRED iQ valuations factor in a base-case (most likely), a downside (significant loss of tenants or 50% reduction in rent), and dark scenarios (100% vacant). For full access to the valuation reports as well as full CMBS loan reporting, with detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

Kitsap Mall

715,255 sf, Regional Mall, Silverdale, WA [View Details]

Kohl’s operates a 76,145-sf store at Kitsap Mall, a REO regional mall in Silverdale, WA with $74 million in outstanding debt. Kohl’s owns its improvements, located on the north side of the mall adjacent to JCPenney. The entire mall, including Kohl’s, measures approximately 715,255 sf in size. Only about 533,480 sf of the space is the portion that was foreclosed on in December 2021. The REO portion of the mall was formerly owned by Starwood Retail Partners. CRED iQ previously featured Starwood-affiliated malls in its March 8, 2022 WAR Report, which also mentioned Kitsap Mall as a comp for the Capital Mall located in Olympia, WA.

CW Capital is the appointed special servicer for the Kitsap Mall and has indicated plans to stabilize in-line occupancy and improve operations. The mall will need to be sold out of the CMBS trust at some point in the future. Kohl’s could potentially exit this location through a sale-leaseback; although the central location to Silverdale’s retail corridor may be the best option for the retailer if it wants to remain in the market. The nearest Kohl’s is located approximately 30 miles south in Gig Harbor, WA. For the full valuation report and property-level details, click here.

457,199 sf, Regional Mall, Indiana, PA [View Details]

Kohl’s leases 40,516 sf at Indiana Mall, located approximately 50 miles east of Pittsburgh, PA. Similar to Kitsap Mall, the Indiana Mall is REO. LNR Securities foreclosed on the property in May 2021 and subsequently sold the asset via auction in March 2022. If the auction’s final bid is accepted, a sale of the property could close within 60 days.

Kohl’s operates pursuant to a lease that expires in January 2031. The retailer’s store layout at Indiana Mall is the smallest in CRED iQ’s database and likely aligns with the company’s initiatives for smaller store formats. However, the mall was only 49% occupied as of January 2022. Sales performance for Kohl’s is unavailable for this location, but there appears to be little benefit to the store’s attachment to a struggling mall in need of major redevelopment. For the full valuation report and property-level details, click here.

Kohl’s leases 100,000 sf in this freestanding retail building at 6785 Thomasville Road in Tallahassee, FL. Kohl’s vacated the property in 2016, but has been honoring the lease, which expires in January 2029. Kohl’s appears to be paying approximately $6.10 per sf in rent under a NNN lease. Servicer commentary for the loan indicates that Kohl’s is in the process of sub-leasing the space and has engaged Colliers to facilitate a deal. The listing can be found here. Kohl’s operates a more favorable location in Tallahassee at 2010 Apalachee Parkway, nearby the Governor’s Square Mall. Despite Kohl’s commitment to its lease obligation at the Thomasville Road location, the mortgage secured by the property has a maturity date in June 2025. The presence of a dark building could cause complications in refinancing the debt. For the full valuation report and property-level details, click here.

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. Our data platform is powered by over $2.0 trillion of CMBS, CRE CLO, SBLL, Ginnie Mae, FHA/HUD, and Freddie Mac loan and property data.

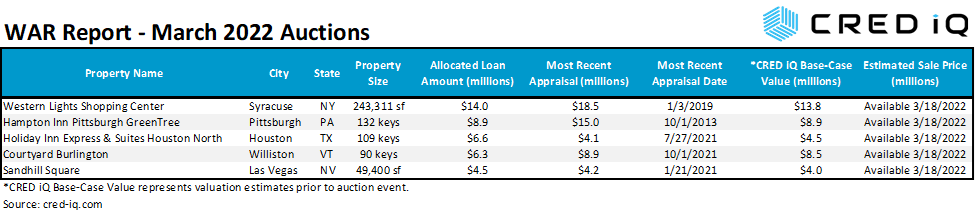

For this edition of the WAR Report, CRED iQ reviewed real-time valuations for five assets that are being marketed for sale this week. Each of these assets is distressed and requires workout by special servicers that have opted for auction sales. While one property is already REO, several properties may be subject to foreclosure if sales do not materialize. This week’s featured properties include three hotels with a history of pre-pandemic distress and two retail properties. All of the assets, four properties and one note, are being sold through an online auction platform with final bids due this week. Valuation guidance for each of the assets is provided prior to the closing of any sales. Contact our team — team@cred-iq.com — for post-auction results and valuation guidance.

CRED iQ valuations factor in a base-case (most likely), a downside (significant loss of tenants), and dark scenarios (100% vacant). For full access to the valuation reports as well as full CMBS loan reporting, with detailed financials, updated tenant information, and borrower contact information, sign up for a free trial here.

Western Lights Shopping Center

243,311 sf, Retail Community Center, Syracuse, NY [View Details]

This retail center, which secures a $14 million mortgage, has been in special servicing since October 2020. The property has a history of distress and was also in special servicing from December 2018 through June 2020. KeyBank, as special servicer, does not appear to have attempted to take title of the asset yet but the property has been marketed for sale. An auction sale of the property is scheduled for this week.

Western Lights Shopping Center is located about three miles outside the CBD of Syracuse, NY and has a traditional community center layout. The property is grocery-anchored by Price Chopper, accounting for 28% of the property’s NRA, pursuant to a lease that expires in July 2025. Price Chopper competes with a Wegman’s grocery store located across the street. The property is 71% occupied and has not shown any improvement in attracting new tenants since 2018. For the full valuation report and property-level details, click here.

132 keys, Limited-Service Hotel, Pittsburgh, PA [View Details]

This limited-service hotel, which secures an $8.9 million loan, has been in special servicing since February 2021. Prior to the loan’s transfer to special servicing, a forbearance agreement was signed in August 2020 to provide COVID-related relief. However, cash flow issues existed at the property in 2019, which was evidenced by a below breakeven DSCR for the mortgage. During the forbearance agreement’s repayment period, the loan transferred to special servicing and had delinquent debt service payments. The borrower and special servicer agreed to market the property for sale in order to pay off the loan. The property will be auctioned online this week.

The hotel is located in the Green Tree suburb of Pittsburgh, PA and operates under the Hampton Inn flag pursuant to a franchise agreement that expires on November 30, 2023. Prospective buyers will likely consider costs of a property improvement plan (PIP) required by change of ownership as well as the potential renewal of the franchise agreement. The near-term expiration could also present the opportunity to reposition the hotel under a different brand. The hotel’s closest competitor is a 460-key DoubleTree by Hilton, which benefits from an adjacent sports complex as a primary demand generator. The property averaged 46% occupancy for most of 2021. For the full valuation report and property-level details, click here.

This non-performing loan has an outstanding balance of $6.3 million and is secured by a 109-key limited-service hotel that has been in special servicing since July 2020. Although the loan’s transfer to the special servicer was characterized as COVID-related, the property struggled with cash flow in 2018 and 2019, which yielded below-breakeven DSCRs for the loan. LNR Securities, as special servicer, filed for foreclosure but will attempt to sell the loan prior to scheduling a foreclosure sale. The note sale will be conducted through an online auction this week.

The hotel is located approximately 20 miles north of the Houston, TX CBD and operates as a Holiday Inn Express & Suites pursuant to a franchise agreement with IHG Hotels that expires in October 2024. The property is located fairly close to George Bush Intercontinental Airport (IAH) and has had corporate contracts with airlines in the past, including Spirit Airlines. The hotel faces intense competition given its location along Interstate 45 with more than 10 lodging options within two miles. Additionally, there are three other Holiday Inn Express & Suites locations within 10 miles of the collateral property. For the full valuation report and property-level details, click here.

This hotel, which has outstanding debt of $6.3 million, has been in special servicing since September 2020. The title transferred to Argentic Services Company LP, acting as special servicer, in December 2021. The property was put up for sale via online auction this week. A change of ownership will likely require a PIP to be implemented by any prospective new owner. The last reported PIP for the property cost approximately $928,000.

The property is located approximately seven miles outside of downtown Burlington, VT and operates as a Courtyard by Marriott pursuant to a franchise agreement that expires March 24, 2032. The hotel’s cash flows were severely disrupted by the pandemic; however, operational struggles can be traced back to 2019. Food and beverage operations in 2019 generated a net loss and impaired total net cash flow for the hotel. More efficient operations under new management are a potential value-add opportunity for prospective investors. For the full valuation report and property-level details, click here.

This retail strip center, which has outstanding debt of $4.5 million, has been in special servicing for nearly nine years. The property has been REO since August 2018. However, there is a possibility that the retail center could be sold this week through an online auction. The property has a long history of high vacancy and low net cash flow compared to comparable retail centers. Furthermore, servicer commentary for the property makes note of groundwater contamination issues that still need to be resolved.

The property is located about five miles east of the Las Vegas Strip and has a traditional strip center layout across two buildings. Many of leasable spaces are uniformly sized and the largest occupied suite is approximately 3,850 sf. The property was 72% occupied as of January 2022. For the full valuation report and property-level details, click here.

CRED iQ is a commercial real estate data, analytics, and valuation platform providing actionable intelligence to CRE and capital markets investors. Subscribers to CRED iQ use the platform to identify valuable leads for leasing, lending, refinancing, distressed debt, and acquisition opportunities. Our data platform is powered by over $2.0 trillion of CMBS, CRE CLO, SBLL, Ginnie Mae, FHA/HUD, and Agency loan and property data.

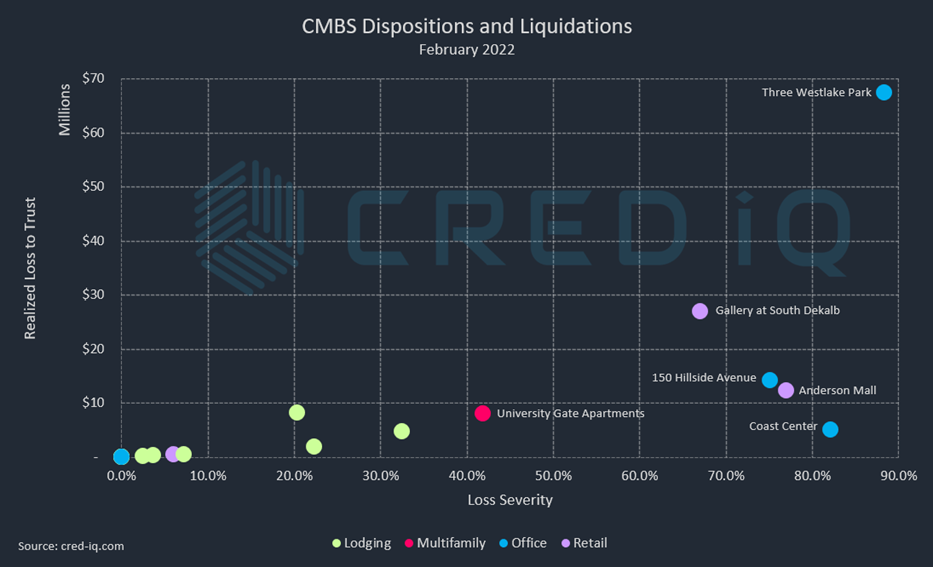

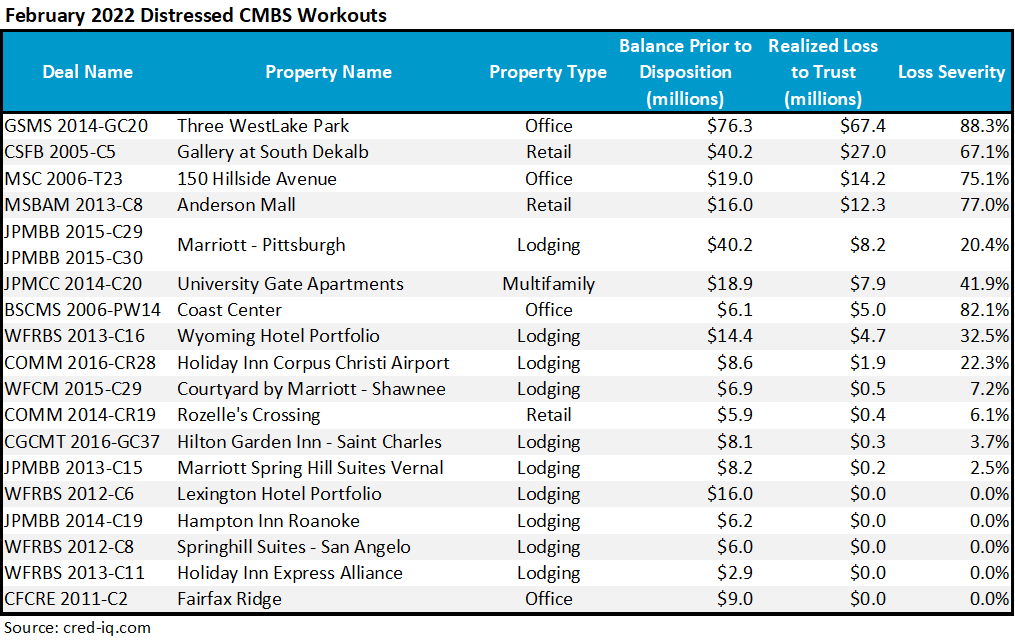

In February 2022, CMBS conduit transactions incurred approximately $150 million in realized losses through the workout of distressed assets. CRED iQ identified 18 workouts that the servicer classified as dispositions, liquidations, or discounted payoffs. Of those 18 assets, there were five dispositions that had either a nominal loss or no loss at all. The remaining workouts resulted in loss severities ranging from 2.5% to 88.3%, based on outstanding balances by disposition. Total realized losses in February were an increase compared to January’s realized loss totals of approximately $108.5 million.

The largest loss, by total amount and by loss severity, was the liquidation of Three Westlake Park, which was an REO, 19-story office building located in the Energy Corridor of Houston, TX. The property was vacant at the time of sale and future plans for the property centered around a conversion to multifamily use. The REO liquidation resulted in a $67.4 million loss on an outstanding balance of $76.3 million, equal to an 88.3% loss severity. The loss was allocated to the GSMS 2014-GC20 CMBS conduit transaction, which has been under a Control Termination Event since May 2021 that allows the trust’s operating advisor to consult on a non-binding basis with special servicing major decisions.

More than half of the dispositions in February comprised lodging collateral. Loss severities for the lodging assets were comparatively lower than the period’s retail and office dispositions. Lodging loss severities from the period’s distressed workouts ranged from 0% to 32.5%. The largest lodging disposition was the note sale of a mortgage secured by Marriott – Pittsburgh. The $40.2 million loan was sold with an $8.2 million loss, equal to a 20.4% severity.

Notable among the retail liquidations were two regional malls — Gallery at South Dekalb and Anderson Mall. Both assets had loss severities in excess of 60%, exhibiting the extreme binary nature of distressed workouts for impaired lower-tier regional malls. Prior to their respective liquidations, both malls were foreclosed and became REO in 2021.

The largest individual loss from last month was $62.7 million, equal to a 73.6% loss severity, and stemmed from The Crossroads, which is also a regional mall.

Excluding defeased loans, there was approximately $5.2 billion in securitized debt that was paid off or worked out in February which compares to $3.9 billion in January. In February, 6% of the loan resolutions were categorized as dispositions, liquidations, or discounted payoffs. An additional 6% of the loans paid off with prepayment penalties.

By property type, industrial dominated the volume of outstanding debt paid off in February with Blackstone’s retirement of a $2.8 billion mortgage. This loan was secured by 272 industrial properties formerly owned by Colony Capital.

CRED iQ is a commercial real estate data, analytics, and valuation platform designed to unlock investment, financing, and leasing opportunities. CRED iQ provides real-time property, loan, tenant, ownership, and valuation data for over $2.0 trillion of commercial real estate.